Who Really Pays for Carbon Border Taxes? What Market Expectations Reveal

To global equity markets, the EU’s Carbon Border Adjustment Mechanism (CBAM) looks like another burden for European firms.

The CBAM is the world’s first cross-border carbon tax. Beginning in 2026, it mandates EU firms importing carbon-intensive goods such as steel, cement, fertilizer and aluminum to pay for the emissions embedded in those imports. The mechanism complements the EU’s existing tough carbon pricing regime for domestic goods and is intended to reduce “carbon leakage”—the relocation of production or sourcing to lower-regulation countries. The policy is explicitly designed to protect European companies from unfair competition by imposing a carbon price on imports. In principle, The CBAM should level the playing field in the EU and create decarbonization pressure for foreign producers operating in jurisdictions with weaker climate regulation.

While the policy objective is clear, its economic incidence is not. Which firms will bear the economic burden of the CBAM depends not only on statutory design, but also on market dynamics, including firms’ exposure to the regulation and their ability to adapt or pass costs along the value chain. Understanding where these costs ultimately fall is critical, particularly amid increasing pushback against EU regulation and concerns that well-intended policies may impose disproportionate burdens on European firms.

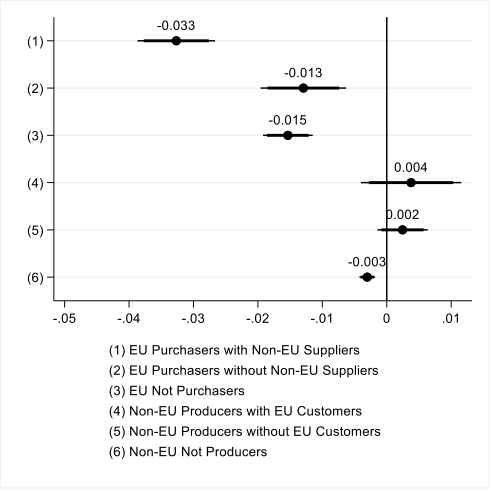

To understand how markets assess expected incidence related to the CBAM, we examine stock price reactions during short windows around three key CBAM announcements between 2021 and 2023[1]. Because stock prices incorporate forward-looking expectations, these reactions provide an early indication of how investors believe the policy will affect firms. The results show that European firms that are most exposed to the CBAM (i.e., those purchasing carbon-intensive inputs “EU Purchasers”) experienced significantly negative stock price reactions following key CBAM announcements. In contrast, non-EU producers of those same goods show little to no comparable decline. On average, the gap in equity market returns between these groups is 2.5 to 3 percentage points.

This pattern runs counter to the idea that foreign producers will absorb the cost of the policy. Instead, investors appear to expect that European firms will face higher effective costs. The underlying mechanism is intuitive. For EU firms with exposure to the CBAM to avoid bearing additional costs, they would need adapt to reduce their exposure or pass the costs on—either upstream to suppliers or downstream to customers. When that is difficult, the costs remain with the firm.

Consistent with this interpretation, the negative market reaction is not uniform across firms. It is most pronounced among European companies with global supply chains that depend on carbon-intensive inputs. These firms are directly exposed to the new carbon charges and often have limited short-term flexibility to adjust sourcing. However, we find evidence consistent with negative spillover effects across EU Purchasers not reliant on imports and even across EU firms operating in industries not directly impacted by the regulation (“EU Not Purchasers”).

At the same time, EU firms with lower profit margins or more concentrated supplier networks experienced larger declines, suggesting that limited bargaining power constrains their ability to shift costs elsewhere. In contrast, EU firms sourcing from countries that already impose meaningful carbon prices, or those connected to more sustainability-oriented suppliers, experienced less negative reactions, consistent with lower incremental exposure to CBAM-related costs.

Importantly, the market response reflects more than just the direct cost of purchasing carbon certificates. Investors appear to anticipate a broader set of implications, including compliance and reporting costs, supply chain restructuring, and the gradual phase-out of free emissions allowances under the EU system. There is also evidence that markets expect increased uncertainty, as reflected in higher stock return volatility for exposed firms. Taken together, these effects point to both lower expected cash flows and a higher cost of capital—two channels through which firm value can decline.

For executives, the findings highlight that CBAM is not just a regulatory compliance issue, but a strategic and financial one as well. Our findings suggest exposure to carbon pricing extends across supply chains and beyond the emissions covered by the regulation. Firms that rely on high-emission imports in their value chain could face meaningful transition risk. This means supply chain decisions are increasingly strategic from a carbon perspective. Choices about sourcing, supplier relationships, and production location now or in the future are likely to include financial consequences related to carbon pricing. While the EU was the first to implement a carbon border tax, it is not expected to be the last, with similar regulation under consideration by a variety of nations including Canada and the United Kingdom.

More broadly, the findings highlight a tension at the heart of cross-border climate policy. While the CBAM is designed to protect domestic industry and enforce the principle that polluters should pay, the reality is more complex. In a globally interconnected economy, the incidence of carbon pricing depends on contractual relationships, competitive dynamics, and adjustment frictions. As a result, the costs of policies intended to prevent carbon leakage may largely be absorbed domestically.

The CBAM is still in its early stages, and its full effects will depend on how firms respond over time. Companies may renegotiate supplier contracts, reconfigure supply chains, invest in lower-carbon inputs and processes, or pass costs through to customers. These adjustments will ultimately determine how the burden is distributed. However, the message from financial markets is already clear: investors expect the CBAM to be costly for European firms, particularly those most integrated into global supply networks for carbon intensive inputs.

[1] Alonso, M, Jacob, M., Ormazabal, G., and Raney, R. 2026. Cross-border carbon taxes and shareholder wealth. Working paper available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4832122