New Financial Statement Disclosures Give Us a Better Tax Map. We Need to Use it Carefully.

For reporting periods beginning on or after December 15, 2024, the Financial Accounting Standards Board (FASB) is requiring public companies to provide enhanced tax disclosures in their 10-K. These disclosures respond to demand from investors, creditors, and lenders for greater transparency about how global operations, tax planning and tax risk affect cash flows and effective tax rate (ETR). The more granular disclosures could prove useful to an even wider audience including policymakers, journalists, and the general public.

The new disclosures tell us more about what drives a company’s ETR and where it makes tax payments. They do not, however, tell us enough to fully determine whether tax payments are aligned with the location of real economic activity. In that sense, they offer a more detailed, but still incomplete map of a corporation’s tax landscape.

Newly Required Disclosures

Accounting Standards Update (ASU) 2023-09 aims to significantly enhance and standardize the information public companies provide in the income tax footnote to their financial statements. Although it falls short of public country-by-country reporting, it is intended to offer new landmarks to help users better understand a company’s global tax planning, tax risks, and tax obligations.

Two changes are particularly important.

ETR Reconciliation: Prior to ASU 2023-09, required ETR disclosures were largely unstandardized. Companies disclosed “significant” reconciling items but retained wide latitude over descriptions and the aggregation of related items. Investors claimed these disclosures provided insufficient detail to assess tax risks and the sustainability of a company’s ETR and made it difficult for users to compare ETR drivers across companies.

ASU 2023-09 requires disclosure of eight specific categories, including foreign tax effects, tax credits, and the effect of cross-border tax laws to help users understand why a company’s ETR differs from the statutory rate and whether those differences are likely to persist.

Cash Taxes Paid: ASU 2023-09 also requires companies to disclose the amount of income taxes paid, net of refunds, by federal, state, and foreign jurisdictions. Any individual jurisdiction where income taxes paid is at least 5% of total income taxes paid must also be separately disclosed.

Useful Information, for Specific Purposes

The FASB’s stated objective for these enhanced disclosures was improved decision usefulness for investors. The usefulness comes in part from enhanced visibility. That visibility is important because the risks associated with tax planning can vary by country and by tax strategy, with some tax strategies being more politically or economically fragile than others.

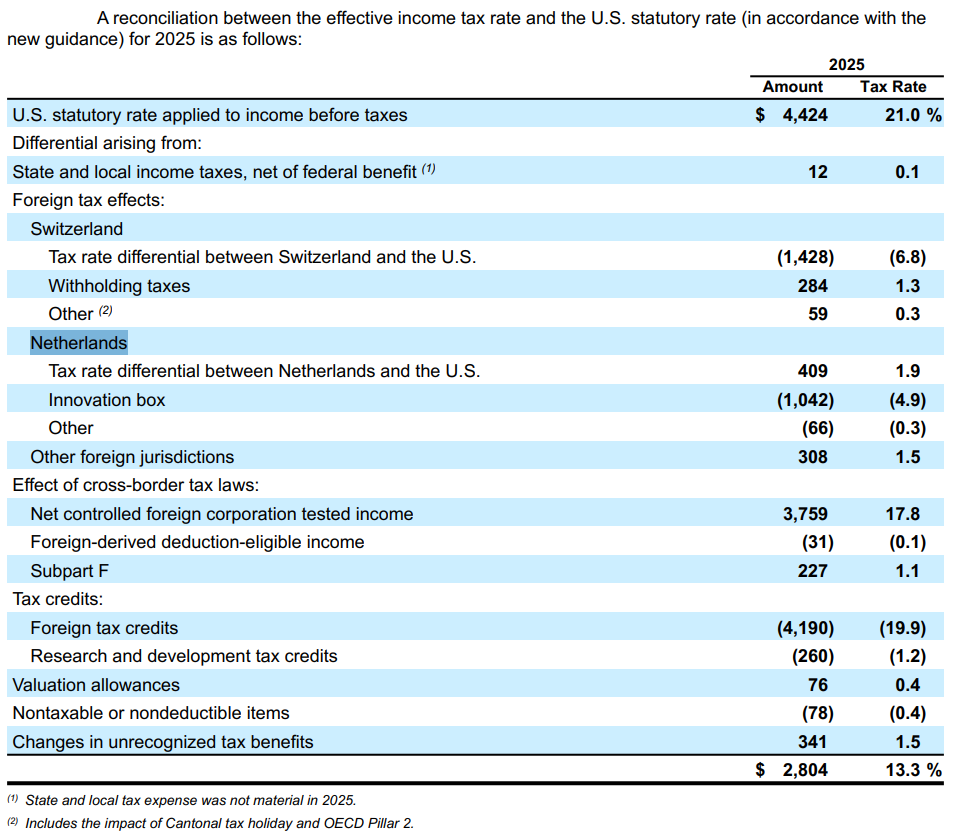

Merck illustrates this point. In 2024, Merck disclosed a $1.30 billion tax benefit arising from “foreign earnings”, offering little context about the underlying strategy or its long-term risk. In its enhanced 2025 disclosure, Merck reveals a $1.04 billion tax benefit attributable to an innovation box regime in the Netherlands. This detail helps users identify the underlying source of a material tax benefit and better evaluate whether the benefit is stable or fragile.

FIGURE 1: MERCK’s ETR RECONCILIATION FOR 2025

Limitations of the New Disclosures

But even a better map can leave blank spaces. The new disclosures do not show the full geographic footprint of a company’s profit or of its profit drivers – employees, tangible and intangible assets. Without those coordinates, strong conclusions are hard to draw. Tax payments to a low-tax jurisdiction may reflect aggressive income shifting, but they could also reflect real operational decisions, timing differences, prior-year audit settlements or other legitimate business factors.

Returning to Merck, the company reports about 56% of its 2025 sales in the U.S. but only about 26% of its income tax payments are to the U.S. government. This pattern could reflect aggressive tax planning, or it could reflect the timing of legitimate tax planning strategies combined with the realities of cost allocation for a global pharmaceutical company. In reality, it likely reflects a mix of these factors. Without a complete picture of the location of the company’s operations, it is challenging to assess whether tax payments are aligned with real activity or distorted by tax minimization considerations.

What Should We Do with this Information?

These disclosures are valuable, but their value depends on how carefully they are used. A single data point can support multiple conclusions depending on what additional context a reader brings or assumes.

A recent article by the FACT Coalition illustrates both the promise and the peril of these new disclosures. FACT tallied more than $11 billion in aggregate tax savings attributable to “haven jurisdictions” across 40 large U.S. companies, with pharmaceutical and biotech firms accounting for the majority. The analysis also identifies that roughly 70% of those savings were concentrated in Switzerland, Ireland, Puerto Rico, and the Netherlands. Both findings were made possible, in large part, by ASU 2023-09.

But the report moves quickly from observation to conclusion, characterizing the pattern as evidence that U.S. corporations “stash profits in tax havens.” That framing may be accurate for some companies and some transactions. For others, it ignores important complexity. Consider again the Merck example: FACT highlights Merck as one of the companies reducing its tax bill by more than $1 billion through tax havens. What the new disclosures actually show, however, is that a significant portion of those benefits is attributable to an innovation box regime in the Netherlands that the EU’s own Code of Conduct Group has characterized as “non-harmful.” That is a meaningful distinction, and one that the disclosures themselves make visible. The lesson is not that Merck’s tax planning is beyond scrutiny. The lesson is that the disclosures require deeper engagement to fully contextualize them.

This nuance suggests different norms for different audiences. Investors and analysts should use enhanced ETR reconciliations to ask better questions. Journalists and advocacy groups should remember that a number without context provides only a starting point, not a definitive answer. Policymakers should distinguish between patterns that reveal genuine abuse that warrants a response, and those that reflect legitimate incentive structures their own governments have enacted.

Companies, for their part, have a corresponding obligation. The new disclosures create an opportunity to help users understand the business and economic substance behind material reconciling items. Transparency is not just a reporting exercise; it is the beginning of a conversation.

Conclusion

ASU 2023-09 gives us a better tax map, but not a complete one. It marks more of the terrain: the categories that move ETRs, the jurisdictions where cash taxes are paid, and the places where low-tax outcomes may deserve greater scrutiny. But it does not show the precise route a company took to arrive where it did, nor does it reveal the full geography of the company’s economic activity. The new disclosures can point users toward the right questions, but they cannot answer all of them. Treating them as though they can risks limiting their usefulness.