Should States Conform to Federal Tax Law?

The U.S. Congress frequently changes the federal tax code, and those changes have direct consequences for state income taxes. The vast majority of states essentially tell taxpayers: “Start with the taxable income you calculated for the federal government, make a few of our specific adjustments, and pay taxes to us based on that final number.” The practice of linking the state’s tax code to the federal Internal Revenue Code (IRC) is called conformity. But just how closely should states conform to federal tax law?

I’ll spare you the technical summary of “rolling” versus “static” conformity, and I won’t dissect the state-level implications of each federal tax change in the One Big Beautiful Bill Act.[1]

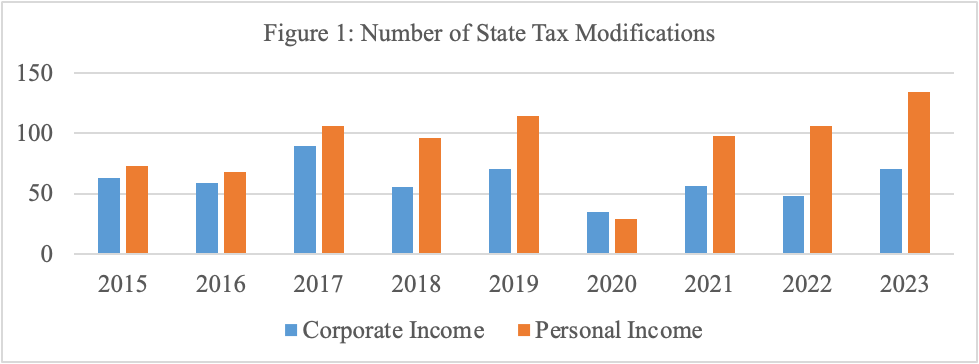

Instead, let’s start with the broader state tax landscape. State individual income tax rates range from 0% to 13.3%, and corporate rates range from 0% to 11.5%. Between 2015 and 2023, states enacted over 1,300 collective modifications to their corporate and personal income tax codes, altering rates, bases, and credits (see Figure 1). Some states have even implemented or proposed entirely new taxes on digital advertising, social media, or wealth. While many states recently cut their income taxes, other states are realizing they need to raise taxes to balance their budgets. Thus, state tax rates are diverging[2] and bases are adapting to a constantly changing economic environment.

As a researcher who studies state tax policy and administration, I find this rapidly evolving landscape incredibly intriguing. My tenth-grade A.P. Government teacher (yes, I took an A.P. class or two in high school, so you know I’m credible) used to say, “The most gripping reality show on television is government and politics.” One captivating subplot is the long-standing debate over conformity, pitting administrative simplicity against local fiscal autonomy.

The arguments for and against conformity

The primary appeal of conformity is simplicity and administrative efficiency. If every state decoupled entirely from the IRC, taxpayers and their accountants would drown in separate accounting ledgers (even accountants get exhausted by these), depreciation schedules, and definitions of gross income. Anyone who has trudged their way through multistate tax compliance will eagerly vent to you about the headache and confusion it causes (pro tip: they don’t need you to solve their problems, they just need you to listen). Furthermore, conformity allows state revenue departments to leverage the enforcement capabilities of the Internal Revenue Service (IRS), effectively adopting federal regulatory guidance and case law.

However, tax policy is about much more than administrative ease. Broadly speaking, tax policy is a tool to raise revenue, fund public goods and services, redistribute income, and influence behavior. Some people say that taxation is the Swiss Army Knife of policymaking (and by “some people,” I mean me). Just as the IRC (taxable income) has different objectives from Generally Accepted Accounting Principles (financial statement income), state tax codes can have different objectives from the federal code. The federal government focuses on broad macroeconomic goals, while states must prioritize their own localized values and constraints.

One of the key objectives of any state tax system is revenue generation. Unlike the federal government, which can easily engage in deficit spending or issue debt, state governments are generally bound by constitutional or statutory balanced-budget requirements. This constraint forces states to prioritize revenue sufficiency and fiscal stability to a higher degree than the federal government. States cannot run deficits, yet need to fund local public goods such as education, infrastructure, safety, and pickleball courts (a sport that is almost as hotly debated as conformity). When the federal government reduces the tax base to stimulate economic activity or spending (e.g., via bonus depreciation or tip income exemptions), a conforming state mechanically suffers an immediate revenue loss. Consequently, a state tax cut via a federal base change requires an offsetting expenditure reduction or tax hike.

Why state tax codes diverge

No two states share the exact same environment, and their policy objectives may differ from one another. Demographics, industries, and socioeconomic profiles vary widely; there is no universal tax structure that yields identical results across states or across time. For example, a state whose economy runs on agriculture and energy extraction may require a different approach to taxation than one built on financial services or tech. Furthermore, as the economy became more globalized, digitized, and service-based, traditional tax bases began to erode. Legislatures have had to move quickly to determine exactly what and who should be taxed.

Simultaneously, state lawmakers must navigate the economic effects of their tax policies, and compete for mobile capital and labor. Academic literature suggests multistate corporations respond to state taxes by reallocating activity across states or adjusting hiring practices.[3],[4] Individuals, particularly higher-income earners, may move in response to higher taxes to keep more of their wealth.[5],[6] Consequently, state legislatures must balance a host of competing objectives.

What’s a state to do?

If all of this seems like a challenging task for state policymakers, that’s because it is. Any piece of tax legislation requires a rigorous revenue estimate and economic impact analysis. To enhance the accuracy of these estimates, it’s necessary to weigh the net revenue effect against the expected economic and administrative effects. This process must move beyond static scoring to include:

- Dynamic Modeling: Estimating behavioral responses such as interstate mobility, investment, and hiring shifts.

- Administrative Analysis: Evaluating administrative costs and frictions for taxpayers and the tax authority.

- Incidence and Distributional Analysis: Identifying who gains and who loses by estimating the effects across different income cohorts, subpopulations, and business entities.

This process is not easy, but precision improves with better questions. For instance, if a state conforms to federal capital expensing, does the policy create high-paying local jobs or subsidize capital investment out of state? When do capital and labor function as substitutes versus complements? Will an R&D tax break spur new jobs and innovation or simply reward companies for routine expenses? To what extent do informational or administrative frictions prevent taxpayers from responding to tax incentives? Who ultimately bears the economic burden of a corporate tax hike?

At times, existing research can help shed light on these types of questions.[7]At other times, entirely new analyses are warranted.

The case for investment and academic partnerships

In the midst of our polarized political and information environment, evidence-based policymaking is critically important to improve overall welfare. The reality, however, is that state governments are notoriously resource-constrained, making it difficult to develop highly sophisticated dynamic models or analyses.

One novel solution to the budget and bandwidth constraints of state governments is to leverage university researchers, who can bring deep, specialized knowledge in causal inference, belief elicitation, prediction, and forecasting. More importantly, they work for free (technically, they work to publish peer-reviewed research that advances our collective understanding of tax policy, but luckily that’s free to the state).

States are increasingly partnering with academic researchers to enhance both policy design and administrative execution. Although these collaborations face real frictions (time, data security, personnel turnover, etc.), there are many success stories across the country.[8] By collaborating with academics, resource-constrained agencies can leverage novel datasets, design and implement pilot programs, conduct A/B testing, and determine not only if a policy works, but which administrative features make the policy most effective and efficient.

Concluding thoughts

Although the administrative appeal of conforming to federal tax policy is undeniable, state policymakers must consider local conditions, competing objectives, and strict budget constraints. As “laboratories of democracy,” states have an opportunity and responsibility to thoughtfully design, implement, and evaluate new tax policies. When states invest in the resources to rigorously estimate the tradeoffs of these policies, they increase the likelihood that their tax codes build stronger, more resilient local economies. And when states are transparent about what they learn, other states can benefit. The result might be a less dramatic “subplot” – but if it improves outcomes, I like to think my A.P. Government teacher would approve.

[1] For summaries, see Walczak, J. 2025. “State Tax Implications of the One Big Beautiful Bill Act.” Tax Foundation. Available at https://taxfoundation.org/research/all/state/big-beautiful-bill-state-tax-impact/; and Morgan, J. 2026. “How states are responding to new federal tax law changes.” Available at: https://www.ey.com/en_us/insights/tax/state-responses-to-2025-federal-tax-changes-and-impacts.

[2] Walczak, J. 2026. “The State Income Tax Divergence.” Tax Foundation. Available at: https://taxfoundation.org/blog/state-income-tax-trends/.

[3] Giroud, X. and J. Rauh. 2019. “State taxation and the reallocation of business activity: evidence from establishment-level data.” Journal of Political Economy 127 (3): 1262-1316.

[4] Welsch, A. 2023. “The Effect of Market-Based Sourcing on Labor Outcomes.” Journal of Public Economics 225 (2023): 104966.

[5] Moretti, E. and D. J. Wilson. 2017. “The Effect of State Taxes on the Geographical Location of Top Earners: Evidence from Star Scientists.” American Economic Review 107 (7): 1858–1903.

[6] Rauh, J. and R. Shyu. 2024. “Behavioral Responses to State Income Taxation of High Earners: Evidence from California.” American Economic Journal: Economic Policy 16 (1): 34–86.

[7] E.g., the following paper examines the tax incidence of the state corporate income tax: Suárez Serrato, J. and O. Zidar. 2016. “Who benefits from state corporate tax cuts? A local labor markets approach with heterogeneous firms.” American Economic Review 106 (9): 2582-2624.

[8] Recent examples of academics partnering with state agencies to examine tax policy include the following: Belnap, Welsch and Williams (2023) examine remote sales tax compliance in Texas; Rauh and Shyu (2024) examine interstate mobility after a California personal income tax increase; Lester, Millar, and Rauh (working paper) examine state tax subsidy outcomes in Alabama; Belnap, Gramlich, Welsch, and Williams (working paper) examine program participation of a state-level Earned Income Tax Credit in Washington state; Lester and Welsch (working paper) examine taxpayer awareness and perceptions of a major state income tax cut in Hawaii.