Accounting for bad math in tax policy: How being off by 10x gives us bad tax policy

When policymakers do not understand the size of a problem, or as it turns out, are led to believe by flawed academic research that it’s 10x bigger than it is, they cannot effectively fix it. So, it is especially important that proposed tax increases on multinational enterprises (MNEs) (and corresponding estimates of revenue raised) are based on sound interpretations of where MNEs’ profits are generated and the tax paid on those profits. As I show with my coauthor in Blouin and Robinson (2025), academic research in the U.S. got it wrong – very wrong – and it should serve as a warning bell that the tax community must scrutinize work more closely.

Influential tax policy work published prior to the passage of the U.S. Tax Cuts and Jobs Act of 2017 purports to show that U.S. MNEs earned between 50% and 60% of their foreign profits in tax havens and claims the U.S. government surrenders $100 billion annually in “lost” revenue to profit shifting (Clausing, 2016; Zucman 2014). But after I counted U.S. MNEs’ foreign profits only once in the country where the operations are located, the $100 billion estimate drops to just $10 billion. The alleged more than 35% of US tax revenue lost to profit shifting drops to just 4%. This flawed estimate, on which policymakers relied, is undermined by some bad math regarding the location of MNE income and taxes paid.

The need to measure these constructs is not letting up anytime soon. For example, consider the OECD’s two-pillar solution to address the tax challenges arising from the digitalization and globalization of the economy. These proposals provide new taxing rights for market jurisdictions (Pillar One) and put a floor on tax competition through the creation of a global 15% minimum effective corporate tax rate (Pillar Two). The OECD’s latest estimate of annual global tax revenue gains of between USD 13-36 billion from Pillar One and around USD 220 billion for Pillar Two rely on properly measuring the location of MNE income and taxes paid.

The higher these numbers the more policymakers will make statements such as “This new economic impact analysis again underlines the importance of a swift, efficient and widespread implementation of these reforms to ensure these significant potential revenue gains can be realized.”[1] To be clear, I am not critiquing these new estimates; to do so would require careful replication and scrutiny of the calculations, something I certainly hope will happen in the tax research community. Here, I wish to alert tax policymakers to the important implications for current and future work, such as this, of my discovery (along with Blouin) of measurement error in previous U.S. work.

The measurement errors we discovered stem from a misunderstanding of the accounting standards that apply to businesses that operate with multiple corporate entities across borders – MNEs. Let’s explain the confusion in a simple example. First, there is the issue of double counting. Imagine a person fortunate enough to own a profitable business incorporated in Texas that earns $1,000 of income annually while they live in New Mexico. If they report $2,000 of income because the business earned $1,000 and they earned $1,000 as the owner, that’s counting the same income twice. For years, this is how many public finance economists erroneously misinterpreted the data on the amount and location of foreign profits of U.S. companies.

Just as importantly, another major problem we raised is misattribution of income. If the illustrative Texas business owner living in New Mexico owns equity in the business, they might feel $1,000 wealthier if the business profits increase the value of their stake. But on the personal tax return in New Mexico, there is nothing to report related to the business – those activities are all reportable in Texas, where the company operates. So how should the business’s income be reported? Accountants would report $0 to New Mexico and $1,000 to Texas. However, some economists would incorrectly assign $1,000 to New Mexico and $0 to Texas, meaning that misattribution also confuses whether the business is paying sufficient tax. If $1,000 of income is misattributed to New Mexico but no tax is assessed because those earnings were in Texas, the business appears to pay $0 in taxes. Things can get even more confusing if the Texas business distributes a portion of its earnings to the New Mexico business owner. If policymakers create tax policy based on work misinterpreting data, prescriptions will focus on the incorrect assumption that companies aren’t paying their fair share.

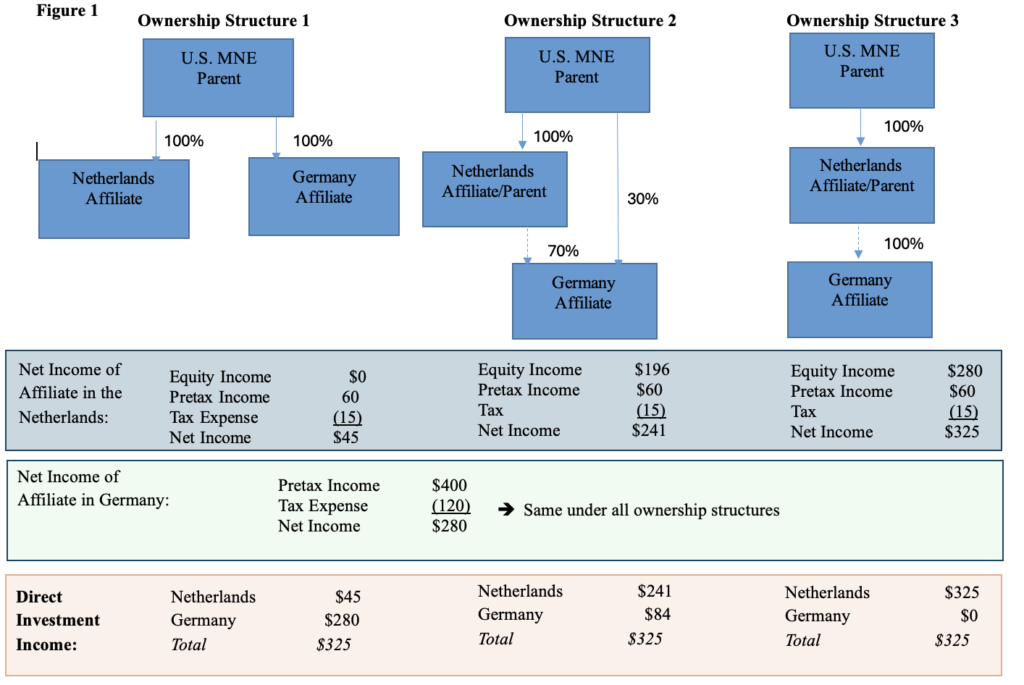

The same lens is essential to understanding MNEs’ foreign profits. Instead of New Mexico and Texas, suppose a global U.S. business has a subsidiary in Netherlands and another in the Germany, owned by the Dutch company. The misattribution problem would lead some economists to believe that the German subsidiary with $1,000 of income (the Texas equivalent) is located in the Netherlands (the New Mexico equivalent). Even though tax was paid on these earnings in Germany, if the Netherlands is misattributed as where the profits are earned, there will appear to be no tax assessed on the profits and some economists will conclude that this income is “low-taxed.” See Figure 1 for an illustration of the accounting methods that underly these measurement issues (see Blouin and Robinson, 2025 for more details).

These (mis)calculations could seriously undermine revenue estimates of a global minimum tax. If tax receipt projections rely on the misassigned income, a minimum tax would not raise substantial revenue from the Netherlands – because no substantial income was earned. A global minimum tax could fall dramatically short of expectations. Policymakers should not rely on proposed international tax revenue estimates as essential pay-fors, particularly if these changes have the second order effect of harming the competitiveness of MNEs.

We are beginning to see researchers explicitly recognize double counting in new data sources such as country-by-country reports (CbCR), (Hugger et al., 2023, 2024) but we must be cognizant that the methodologies used to correct for double counting are not (yet) widely accepted and must be scrutinized. Also important are data imputations, or the filling in of missing data from another data source when the preferred data source is insufficient. We see imputations frequently done using foreign direct investment (FDI) statistics (Tørsløv et al., 2022), but Blouin and Robinson (2025) warn that FDI statistics in many cases suffer from massive misattribution problems. The use of FDI data to shed light on any aspect of profit shifting should be carefully scrutinized.

It is imperative policymakers actively look for flaws in the studies they rely on for their decisions about international tax policies with seismic effects for MNEs. It’s not rocket science. It’s just accounting. Don’t assume that simple math is done correctly. Ask questions. Demand competence.

References

Blouin, J., and L. Robinson. 2025. “Accounting for the profits of multinational enterprises: Double counting and misattribution of foreign affiliate income.” Journal of Public Economics, 252, 105512.

Clausing, Kimberly. 2016. The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond. National Tax Journal (Vol. 68, No. 4), pp. 905-934.

Hugger, F., A. González Cabral and P. O’Reilly (2023), “Effective tax rates of MNEs: New evidence on global low-taxed profit”, OECD Taxation Working Papers, No. 67, OECD Publishing, Paris, https://doi.org/10.1787/4a494083-en.

Hugger, F. et al. (2024), “The Global Minimum Tax and the taxation of MNE profit”, OECD Taxation Working Papers, No. 68, OECD Publishing, Paris, https://doi.org/10.1787/9a815d6b-en.

Tørsløv, Thomas, Ludvig Wier, and Gabriel Zucman. 2022. The Missing Profits of Nations, Review of Economic Studies, 90(3), pp. 1499-1534.

Zucman, Gabriel. 2014. Taxing across Borders: Tracking Personal Wealth and Corporate Profits, Journal of Economic Perspectives (Vol. 28, No. 4), pp. 121–148

[1] https://www.oecd.org/en/about/news/press-releases/2023/01/revenue-impact-of-international-tax-reform-better-than-expected.html