Profit Without Tax? A Flawed List’s Admission to Corporate AMT’s Failings

Published in Tax Notes on May 29, 2026.

The Institute on Taxation and Economic Policy recently refreshed its report on profitable U.S. corporations that paid zero federal income tax.[1] The report attributes this trend to two Trump administration tax reforms: The Tax Cuts and Jobs Act in 2017 and the One Big Beautiful Bill Act in 2025. There is good news, however, if you are concerned about companies reporting accounting profits while paying no income tax in any given year (more on this below). In the years between those two tax reforms, the Biden administration and a Democrat-controlled Congress took aim at precisely this issue with the corporate alternative minimum tax, passed as part of the Inflation Reduction Act. Specifically, corporate AMT imposes a minimum tax of 15 percent on financial accounting profits (or book income) for large corporations whose liabilities under the regular corporate tax system fall below that threshold.

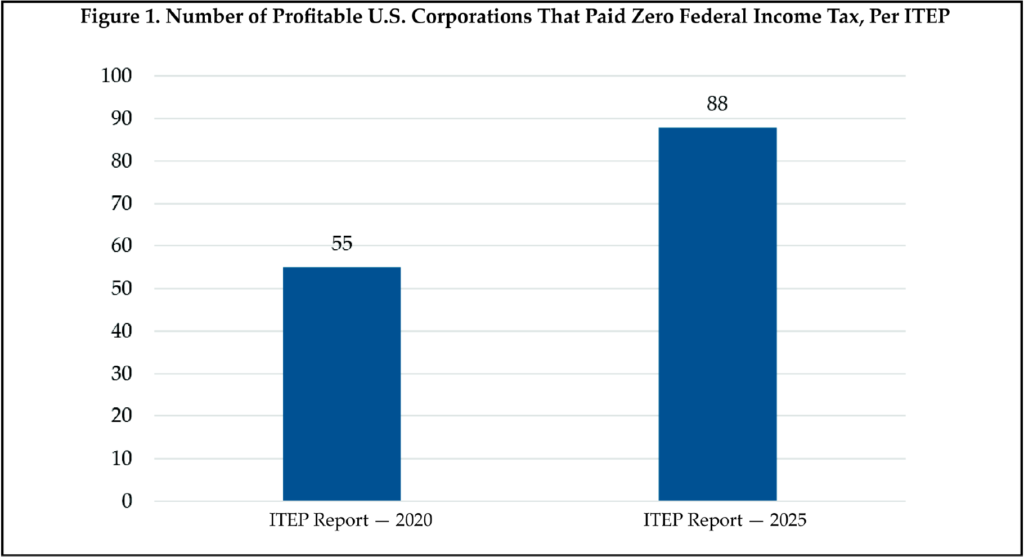

So the days of big, profitable corporations paying zero corporate income tax are over, right? As it turns out, the list went from 55 in 2020 to 88 in 2025 (see Figure 1).[2]

How could this happen? It is tempting to point the finger at the TCJA and OBBBA, which lowered corporate tax rates and increased other corporate deductions, such as accelerated depreciation. But if you care about companies being profitable and paying no tax in the same year (again, a big “if,” which I discuss below), we need to ask why corporate AMT — the law specifically designed to prevent this from happening — has apparently failed.

In the sections below, I briefly outline corporate AMT’s shortcomings, discuss key flaws in the ITEP’s list, and show what we can learn from a deeper dive into a few companies on the ITEP list.

I. Why Corporate AMT Has Failed

Corporate AMT’s shortcomings stem from three interrelated issues: conceptual flaws, vague statutory design, and extraordinary complexity.

First, corporate AMT is conceptually flawed. At its core, the tax attempts to bridge two systems that are built for fundamentally different purposes. Financial accounting standards, set by the Financial Accounting Standards Board, are designed to provide decision-useful information to investors and other capital providers. The tax system, in contrast, is intended to raise revenue and, at times, to shape societal behaviors or redistribute resources. These differing objectives naturally produce different measures of income. By anchoring a minimum tax to financial statement income, corporate AMT implicitly treats book income as a meaningful proxy for taxable capacity, even though it was never designed for that purpose.

Second, the conceptual issues manifest in vague and uneven statutory drafting. Lawmakers were aware that a pure tax on book income would produce undesirable results, particularly where differences between book and taxable income reflect deliberate policy choices. Accelerated tax depreciation, for example, reflects a long-standing policy choice to incentivize investment. Applying a minimum tax to book income would effectively claw back this and other deliberate incentives. To address this issue, Congress levied the tax not on pure book income but on adjusted financial statement income, which modified book income to account for certain tax preferences, including depreciation.

But this solution undermined the original premise of the tax. What began as a straightforward tax on book income inevitably evolved into a hybrid measure with dozens of adjustments, many of which reintroduced the tax deductions that drive the wedge between book and tax income.

Compounding this problem, the Internal Revenue Code sections for corporate AMT delegated significant authority to Treasury, deferring to the secretary 28 times. The heavy reliance on administrative guidance means that many of the law’s most consequential details were never fully specified in statute, leaving substantial room for interpretation in implementation. It is fair to argue that the erosion in corporate AMT that allows profitable corporations to avoid paying tax is in part caused by regulations and executive actions under the Trump administration.[3] But this flexibility was built into the statute from the outset and is the inevitable result of attempting to levy a tax on a conceptually flawed base.

Third, corporate AMT is extraordinarily complex. Early proponents lacked the tax and financial accounting expertise to foresee issues such as entity-scope and consolidation rules, fair value and accounting method rules, and foreign income adjustments, among many others. The result is a regime that is difficult to comply with and administer. The proposed regulations alone exceed 600 pages, and new guidance continues to evolve. Executives report high compliance costs with little change to tax revenue raised or their firms’ incentives for tax planning.[4] Unintended interactions with new laws, such as the OBBBA, become virtually impossible to predict or avoid. A tax this complicated is more of an additional compliance layer than a minimum backstop.

II. ITEP’s List: Should We Care About Companies Reporting Accounting Profits and Not Paying Tax in a Given Year?

No, we shouldn’t.

Lists like the ITEP’s can be compelling. There is an intuitive appeal to identifying large, profitable corporations that appear to pay no federal income tax, and there is little doubt that the ITEP’s latest number will be cited in future presidential addresses. But the list is deeply flawed.

A primary issue is that the ITEP’s analysis relies on a point-in-time snapshot in an inherently volatile environment. Corporate earnings and tax liabilities fluctuate significantly from year to year, driven by business cycles, investment timing, and the increasingly dynamic nature of tax rules. Hence, evaluating firms based on a single year yields a misleading picture.

To illustrate, I examined filing data from the last five years for the 88 corporations on the ITEP list and identified how many would still be profitable and pay no tax (using the ITEP’s definitions) over that period. Instead of 88 corporations, I find just 16 (see Figure 2). The steep drop suggests that most cases are driven by transitory factors, such as the timing of large investments or losses carried forward from prior years, rather than persistent tax avoidance.

Another way to demonstrate this point is to look at the persistence of companies across the ITEP’s own lists. Only nine corporations, or roughly 10 percent, appear on the ITEP reports for both 2025 and 2020. The fact that the vast majority of companies on the 2025 list were not on the 2020 list suggests that the tax system is generally working as intended. Rather than reflecting certain firms’ sustained ability to avoid tax altogether, the turnover indicates that zero-tax outcomes are typically short-lived.

III. Are All Comparisons of Book and Tax Income Fraught?

No, not all comparisons are fraught.

None of this is to suggest that differences between book and tax income are completely irrelevant. Corporate income tax returns require firms to reconcile book and tax income, indicating that the IRS finds this information useful for enforcement. And research has long shown that large differences are associated with greater audit adjustments, suggesting that, on average, substantial gaps between the income reported to investors and the income reported to the IRS may reflect aggressive positions that are not sustainable upon audit.[5]

But context matters, and a closer look can reveal more than a simple list. Let’s consider a few examples.

A. Tesla

In 2025 Tesla reported $4.8 billion in pretax U.S. profit and zero dollars of current federal income tax expense.[6] If book and tax income were equal, we would expect to see about $1 billion in current federal income tax expense (21 percent of $4.8 billion). The tax rate reconciliation helps shed light on the gap (at least the permanent book-tax differences). There we see that the single largest item bringing down Tesla’s effective tax rate is $354 million in nontaxable manufacturing credits. These were passed as part of the Biden administration’s IRA. Right behind the IRA credits is $352 million of research and development tax credits, which have long had bipartisan congressional support. Another major factor is accelerated depreciation, which the OBBBA enhanced by making bonus depreciation permanent under section 168(k) and adding qualified production property under section 168(n). Accelerated tax depreciation and amortization reduced Tesla’s current income tax by $488 million relative to book income in 2025 (the difference between its 2024 and 2025 deferred tax liability for this item), although this includes both U.S. and foreign effects.

B. Vistra Energy

Vistra Energy reported $1.1 billion in pretax book income and negative $3 million in current federal income tax expense.[7] In the company’s tax rate reconciliation, the two largest permanent items relate to stock-based compensation ($145 million) and production tax credits ($46 million). Congress has long supported low book expenses and high tax deductions for stock-based compensation, even pressuring the FASB not to introduce accounting standards that would reflect these expenses on the books.[8] Moreover, the IRA introduced the production tax credits that Vistra claimed. Vistra also benefited significantly from accelerated tax depreciation, which was expanded in the OBBBA as discussed above.

C. Yum Brands

For 2025, Yum reported $1.1 billion in U.S. pretax book income and negative $5 million in current federal income tax expense.[9] Like Tesla and Vistra, Yum benefited significantly from accelerated depreciation in the OBBBA, stating in its Form 10-K specifically that “as a result of the accelerated tax deductions, our cash tax payments for 2025 were significantly reduced.”[10]

In the same filing, Yum disclosed migrating intellectual property to Malta. This kind of transfer reflects classic base erosion and profit-shifting strategies, where profits are moved to low-tax jurisdictions to reduce overall tax liability. Unlike accelerated depreciation or tax credits, which are explicitly designed by Congress to encourage investment and specific economic activities, these cross-border structuring decisions raise more substantive policy concerns.

Overall, these examples highlight both the limitations of a simple but superficial list and the importance of digging deeper. Not all instances of low or zero tax liability are created equal. A closer look can reveal concerning trends, such as companies migrating intellectual property offshore. However, in most cases, the drivers are benign and reflect activities such as investment, R&D, and sustainable energy that are intended and encouraged by Congress. Moreover, these incentives have been enacted by both Democrats and Republicans, and efforts to attribute concomitant outcomes to a single political party are not supported by the underlying policy record.

IV. Conclusion

The ITEP’s latest report asserts an eye-catching trend: a growing number of profitable corporations that report no current federal income tax expense. In this article, I use the ITEP’s list to illustrate three points. First, this pattern underscores that corporate AMT is failing at its stated objective of ensuring that large, profitable firms pay a minimum level of tax. Second, the focus on single-year outcomes substantially overstates the magnitude and persistence of the issue, as most zero-tax outcomes are temporary and driven by timing effects rather than sustained tax avoidance. Finally, many of the firms that appear on these lists are not exploiting loopholes so much as responding to incentives deliberately embedded in the tax code.

[1]Matthew Gardner and Spandan Marasini, “At Least 88 Profitable U.S. Corporations Paid Zero Federal Income Tax in 2025,” Institute on Taxation and Economic Policy (Apr. 14, 2026).

[2]Gardner and Steve Wamhoff, “55 Corporations Paid $0 in Federal Taxes on 2020 Profits,” ITEP (Apr. 2, 2021).

[3]See, e.g., Committee for a Responsible Federal Budget, “Resolution to Overturn CAMT Guidance Would Reduce Deficits” (Feb. 10, 2026).

[4]Andrew Belnap and Jeff Hoopes, “How Complex Is the New Corporate Alternative Minimum Tax?” Bloomberg Tax Management Memorandum, Feb. 18, 2026; Belnap and Hoopes, “The New CAMT Does Not Meaningfully Alter Corporate Tax Outcomes,” Bloomberg Tax Management Memorandum, Mar. 19, 2026.

[5]See, e.g., Lillian F. Mills, “Book-Tax Differences and Internal Revenue Service Adjustments,” 36 J. Acct. Rsch. 2 (1998).

[6]Tesla Inc., Annual Report (Form 10-K) (Jan. 29, 2026).

[7]Vistra Corp., Annual Report (Form 10-K) (Feb. 27, 2026).

[8]Nicholas G. Apostolou and D. Larry Crumbley, “Accounting for Stock Options: Update on the Continuing Conflict,” CPA J. (2005).

[9]Yum Brands Inc., Annual Report (Form 10-K) (Feb. 20, 2026).

[10]Id.