How Should We Talk About Cash Taxes?

Think tanks, reporters, academics, economists, voters, lobbyists, and policy advocates all regularly weigh in on taxes, advocating for or against certain policies, but taxes are not simple. There is no one true number that encompasses all the nuances of taxation. Starting this year, new financial reporting will give us more detailed information than we have ever had on corporate taxation. With the new information and new data, it is worth exploring what the numbers can tell us, and importantly, what they don’t. In this article, I use recent reporting by the Financial Accountability and Corporate Transparency (FACT) Coalition to highlight how headline numbers might not tell the whole story.

In 2023 the Financial Accounting Standards Board issued Accounting Standards Update (ASU) 2023-09, a new accounting standard for income taxes that required firms to disclose information on the amount of cash taxes paid by jurisdiction. In comment letters to the FASB, some organizations, such as MSF Investment, were supportive of the new standards. They said the disclosures would help investors and provided specific examples where tax surprises harmed stock prices.[1] Politicians also weighed in on the standard, some supporting and some opposing it.[2] The Chamber of Commerce, among others, argued vociferously against the proposal, contending that activists will use the information to name, shame, or vilify companies.[3] With firms filing their first financial statements under the new reporting rules, it is too early to tell how investors and markets will react, but organizations have been quick to call out companies for their low tax rates using the new information. The FACT Coalition recently wrote an article comparing oil and gas companies’ foreign and U.S. tax payments.[4] The Institute on Taxation and Economic Policy also recently published an article on the tax payments of U.S. corporations.[5] Both articles use the new disclosures to argue that U.S. corporations don’t pay enough tax.

Using new reporting required under ASU 2023-19, the FACT Coalition begins their article with a table detailing the geographic breakdown of cash taxes paid by the major U.S. oil and gas companies. They say that the amount of tax paid to the federal government is a small fraction of the total tax paid, but this comparison is not as useful as one might think. First, one of the limitations of cash taxes paid is that it does not adjust for the level of income earned (in total or by country). For example, Chevron reports that nearly 70 percent of its income is earned outside the United States.[6] For ExxonMobil and ConocoPhillips, the number is 73.3 percent and 51.1 percent, respectively.[7] This is why, when comparing two companies (or comparing the taxes among jurisdictions), it is important to adjust for differing levels of income. As any introductory tax textbook will tell you, taxes paid are a function of tax rates and the tax base. In line with this principle, academics generally prefer an effective tax rate measure. ETRs take a tax amount and divide it by a pretax income amount to get a percentage rate that the company pays. Details of some of these calculations for Chevron are displayed in Table 1. As shown, there can be a large variation in the ETR depending on the measure, which gives groups wide latitude to choose measures that may fit a preferred narrative or viewpoint. Policy makers should be aware of not only the details of the ETR chosen (for example, cash ETR or generally accepted accounting principles ETR) but also the reasons why it was chosen.

Examples of ETRs for Chevron

| Tax Amount (in millions) | Income Measure (in millions) | ETR | |||

| Cash taxes paid | $7,304 | Pretax income | $19,743 | Cash ETR | 37% |

| Federal tax paid | $143 | Domestic pretax income | $5,979 | Federal cash ETR | 2.4% |

| Federal GAAP tax expense | $1,329 | Domestic pretax income | $5,979 | Federal GAAP ETR | 22.2% |

| Foreign tax paid | $6,937 | Foreign pretax income | $13,764 | Foreign cash ETR | 50.4% |

| GAAP tax expense | $7,258 | Pretax income | $19,743 | GAAP ETR | 36.8% |

| Source: All numbers taken from Chevron’s Form 10-K for the year ending December 31, 2025. | |||||

ETRs can be useful when comparing domestic firms in the same country, but there are further complications for multinational firms, especially in the oil and gas space. One example is that tax rates can vary dramatically between countries. In Saudi Arabia, the standard corporate tax rate is 20 percent, but that is increased to 50-85 percent for certain oil and gas companies.[8] In the United Arab Emirates, where almost half of ExxonMobil’s foreign cash taxes were paid, there is a maximum rate of 55 percent on oil and gas, but only a 9 percent rate on other corporate income.[9] In comparison, the U.S. corporate tax rate is only 21 percent. From a policy perspective, because the United States cannot mandate foreign tax rates, achieving parity between foreign and domestic taxes would entail potentially quadrupling the corporate tax rate for oil and gas income.

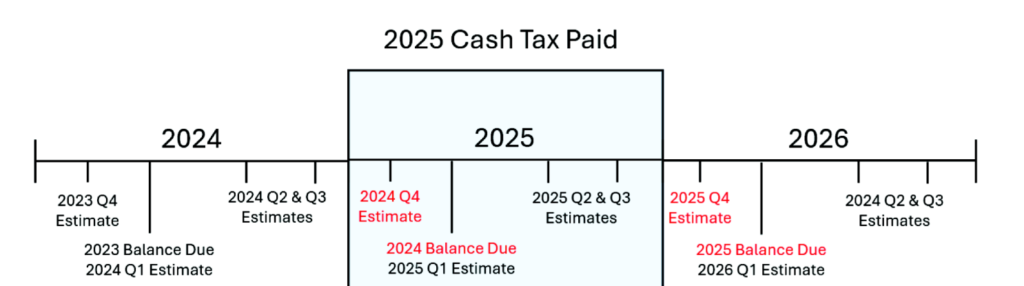

Another complication when using cash taxes is timing. Cash taxes paid relates to actual cash payments that the company makes to revenue agencies during the year. However, this does not necessarily relate directly to the company’s tax return for the same year. As shown in Figure 1, cash taxes paid may include estimated tax payments, balance due payments, or refunds received from the 2024 tax year, in addition to estimated payments for the 2025 tax year. Because tax returns are filed after the year end, some payments that relate to 2025 will not be included in the 2025 cash taxes paid amount if they were paid in 2026.[10] This can create variation across years if there is volatility in earnings or tax law changes between years (for example, the One Big Beautiful Bill Act in 2025 (P.L. 119-21)). Timing is an issue not only for cash taxes paid but also for other measures of tax. Both the FACT coalition and ITEP use current GAAP to calculate each country’s tax expense — a single-year measure. Academics have long known that a single-year ETR can be very volatile and that an ETR measure over time is a much better signal of how much tax a firm is paying.[11] Using a measure of taxes over three, five, or even 10 years can provide a more accurate picture of whether a firm is paying too much or too little in tax.

Figure 1. Cash Payments in Relation to Cash Taxes Paid

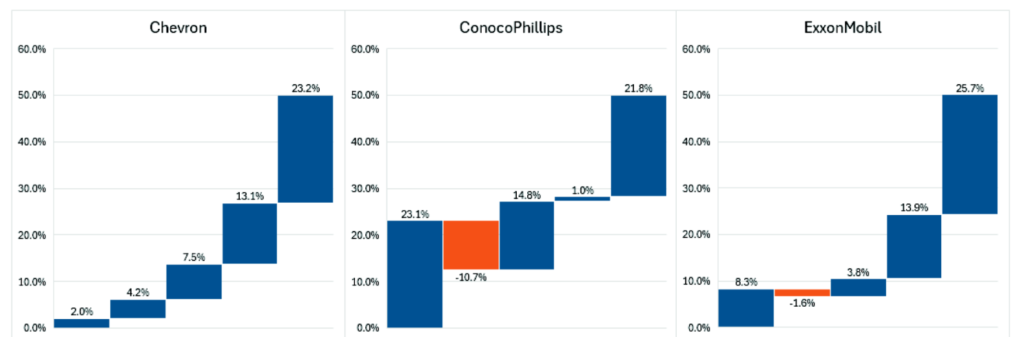

Using financial statements, we can begin to adjust for these factors. Beginning with the ratio of federal domestic cash taxes paid to total cash taxes paid, we see significant variation between the oil companies highlighted in the FACT report. Chevron’s tax ratio is only 2 percent, while ConocoPhillips’s is 23.1 percent. First, we need to adjust for the timing differences mentioned above by calculating a long-run tax rate. To accomplish this, I assume that over the long run each company will have an average federal cash ETR approximately equal to its average current federal tax expense as a percentage of pretax domestic income.[12] As one would expect, this begins to balance out the three companies. Over the most recent five-year period, the average domestic current ETR is 7.7 percent (Chevron), 8.2 percent (ConocoPhillips), and 6.8 percent (ExxonMobil). Second, as mentioned above, the foreign tax rate of oil companies is much higher than the U.S. statutory rate. ExxonMobil has a foreign cash ETR of 34 percent, while the other two companies both have foreign cash ETRs over 50 percent. To normalize the comparison, I adjust the foreign tax amount assuming a 21 percent ETR on foreign income. This accounts for the effect of different tax rates between domestic and foreign income. Third, to make an accurate comparison about the relative tax burdens, we need to adjust the comparison so that there is an equal amount of domestic and foreign income.[13] Because Chevron and ExxonMobil have significantly more foreign income than domestic income, the ratio of federal tax to total tax is quite biased. ConocoPhillips, on the other hand, reports nearly 50 percent of its income as domestic, leading to a much smaller adjustment at this step. The final adjustment represents the unexplained tax benefits that the oil and gas companies get on their domestic income by comparing it with what they would pay at a full 21 percent ETR. I make this adjustment by calculating the amount of domestic tax each company would pay if they paid tax on their U.S. income at the statutory rate of 21 percent.

Figure 2. Reconciliation of the Ratio of Domestic to Total Cash Tax Paid

Note: The baseline is the ratio of the amount of cash tax paid for federal taxes to the total amount of domestic federal tax and foreign taxes. Adjustments are made to end at parity between federal domestic taxes and foreign taxes so that the end point will always be a 50/50 ratio. State taxes are excluded from these calculations. The adjustment for the long-run rate is accomplished by applying the five-year federal current effective tax rate to the 2025 domestic net income. The foreign rate adjustment modifies foreign taxes paid to be equal to the total foreign income multiplied by 21 percent. The equalization of income adjustment modifies domestic income to be equal to foreign income. The tax rate on income is assumed to be flat. Finally, the U.S. tax benefits adjustment modifies domestic taxes paid assuming a flat 21 percent rate. All amounts come from the firms’ Form 10-K filings. Adjustment calculations are done by the author.

As we can see in Figure 2 for all three companies, various factors contribute to the low ratio of domestic taxes to total taxes. Different adjustments require different policy solutions and policy tradeoffs. We can observe that the low ratio is not solely because of exemptions or credits that companies receive, but also because of the nature of the business (for example, where the income is earned and what the statutory tax rate is in foreign jurisdictions). This does not mean oil and gas companies don’t receive domestic tax benefits. U.S. tax benefits appear to significantly reduce the amount of tax that firms pay to the United States. We do not exactly know what these benefits are, but the financial statements offer some hints. As a primary example, the recent change to 100 percent immediate expensing likely played a large role in the reduced taxes for 2025.[14] For ExxonMobil and Chevron, their domestic current ETR was higher in the 2021 through 2024 period than in 2025 after the OBBBA made permanent full expensing. This difference indicates a potentially abnormal deferral of income tax in 2025. Also, property, plant, and equipment accounted for between 40 percent and 117 percent of the firms’ change in deferred tax liabilities between 2024 and 2025, indicating that a significant deferral of tax occurred because of property. Interestingly, it appears that tax credits are not a major source of tax reduction for these firms. For Chevron and CononcoPhillips, separately stated tax credits were less than 1 percent of the total tax expense.[15]

As with any tax policy, there is significant nuance and complexity in interpreting tax amounts, especially when the context of the number is not readily apparent. Policy advocates should be cognizant of the fact that the lay reader likely does not fully understand complex tax statistics. Even when writing for a more sophisticated audience, like lawmakers, greater explanation may be needed. Just like members of the general public, legislators may not necessarily have a depth of experience with taxes. In a recent survey of state legislators, my co-authors and I found that there is a significant knowledge gap among legislators regarding taxes.[16] When asked about three of the most common tax variables, 98 of 185 state legislators (53 percent) were unfamiliar with at least one of the measures. As policy advocates, our goal should be to make sure lawmakers understand both the full context and data behind a proposal. If a proposal is weakened by either, we shouldn’t shy away from it — even if it doesn’t fit the perfect narrative or make for a flashy headline.

[1]FASB, “Proposed Accounting Standards Update — Income Taxes (Topic 740): Improvements to Income Tax Disclosures” (May 8, 2023).

[2]See “Van Hollen, Democratic Senators Urge Greater Transparency in Tax Disclosures” (Sept. 30, 2019); and letter from Republican members of Congress to Richard Jones, FASB chair (July 24, 2023).

[3]See Mauri Webber Sadovi, “FASB Tax Disclosure Plan Draws Fire,” CFO Dive, June 1, 2023.

[4]Thomas Georges and Zorka Milin, “Take the Money and Run — Amidst Oil Price Windfalls, U.S. Oil Majors Continue to Pay Less Tax at Home Than Abroad,” FACT Coalition (Apr. 3, 2026).

[5]Matthew Gardner and Spandan Marasini, “At Least 88 Profitable U.S. Corporations Paid Zero Federal Income Tax in 2025,” ITEP (Apr. 14, 2026).

[6]Chevron, “2025 Annual Report” (2025). Chevron, Annual Report (Form 10-K) (2025).

[7]ExxonMobil, Annual Report (Form 10-K) (Feb. 18, 2026); ConocoPhillips, Annual Report (Form 10-K) (Feb. 17, 2026).

[8]EY, “EY Corporate Tax Guide” (2025).

[9]Corporate Tax UAE, “Official Framework for Energy and Natural Resource Sectors” (Dec. 2, 2025).

[10]In addition to more common issues, taxes paid can also contain errors if firms have audits or tax settlements with revenue agencies. These amounts can be related to tax years that are years or decades in the past.

[11]Scott D. Dyreng, Michelle Hanlon, and Edward L. Maydew, “Long‐Run Corporate Tax Avoidance,” 83(1) Acct. Rev. 61 (2008).

[12]Because domestic cash taxes paid were first reported in 2025, I use current tax expense, which is a similar construct but does not have the same timing differences. As companies file more Forms 10-K under the new reporting standard, we will be able to calculate a long-run domestic cash ETR. Importantly, this is likely to understate the amount of long-run tax owed, as it ignores deferred taxes, which may be paid in future years but will never appear as a current tax expense.

[13]Because the FACT Coalition report focuses on raw tax paid, differences in income can produce differences in amounts of tax, even if all else is equal. This step would not need to be done if an ETR measure were used as the initial basis for comparison.

[14]Although timing differences such as depreciation create temporary differences that reverse over time, in practice if a firm continues to acquire new property, past deferrals are replaced with new deferrals. Generally, when there have been business disruptions or tax law changes, deferred taxes will cause significant changes in the amount of cash taxes owed.

[15]Chevron reported $12 million of “Other” adjustments which include tax credits compared to $7,258 million of tax expense. ConocoPhillips reported $21 million of tax credits against net GAAP tax expense of $4,688 million. ExxonMobil reported $1,298 million of “Other” adjustments against $11,504 million of GAAP tax expense, but does not separately state or identify credit amounts. For all companies, it is likely that foreign tax credits are included in the net foreign adjustments and not separately stated.

[16]Andrew Belnap, Tyler Menzer, and Kyle Pomerleau, “Political Costs and Taxes: Evidence From a Survey and Artefactual Field Experiment,” Working Paper (2026).