Hidden in Plain Sight: U.S. Corporate Tax Haven Activity

When you close your eyes and picture a tax haven, what pops into your mind? Blue waters meeting shimmering sand in a tropical oasis? Most likely. What about the Cliffs of Moher in Ireland; a bustling Singaporean nightlife; or acres of tulips of the Netherlands? Our recent research (Murphy and Vernon, forthcoming) demonstrates these are the picturesque visions that should come to mind when considering the countries enabling the vast majority of tax haven activity for U.S. multinational corporations. Moreover, we argue that the efforts to unveil corporate funds being stored in small offshore countries are likely misguided as most activity occurs in just a handful of major economies used to facilitate tax efficient operations worldwide. The income U.S. corporations are shifting away from U.S. tax authorities is simply hidden in plain sight – in the largest tax havens that are the U.S.’s major allied economies.

The Tax Havens

Our research shows just a few tax havens serve as an outsized public finance threat to U.S. corporate tax revenues – and they aren’t the small, low-tax, high financial secrecy countries. Out of 52 tax haven countries examined, we identify seven tax havens – the Netherlands, Singapore, Cayman Islands, Luxembourg, Switzerland, Ireland, and Hong Kong – holding a combined 81 percent of all U.S. corporate tax haven subsidiaries in 2021. We find even after the Tax Cuts and Jobs Act of 2017 investment continues to flow into these seven tax havens but not to other havens. Thus, despite the policy’s intentions to broadly lessen tax haven use, we continue to see these top havens dominating the foreign tax planning marketplace.

Why These Havens?

Why have these tax havens distanced themselves from the other tax havens? On a tax front, these seven tax havens provide planning opportunities more valuable in the current international tax landscape than simply providing a 0% corporate tax rate. The complexity of global tax policy requires sustainable and defendable tax positions – which is where these seven havens shine. They offer traditional tax advantages through various tax credits, tax holidays, preferential tax regimes, and strategic global tax treaty infrastructures.

However, potentially more important to their success is that these havens deliver tax benefits beyond activity in the haven itself – they allow companies to globally move capital in a tax efficient manner. Prior research suggests these countries are “flow-through” economies, which is beneficial as CFOs do not want to have to pay to access their own cash held in a different country. These tax havens allow companies to tax-efficiently move capital where it is needed often by avoiding burdensome withholding taxes, a type of exit tax designed to keep capital within the bounds of a country. The cash isn’t necessarily stored indefinitely – these countries are not simply large piggy banks – but rather a strategic part of a firm’s overall tax-efficient cash and liquidity management policy.

Besides numerous tax advantages, these countries, as compared to other haven options, offer economic and political stability along with world-class financial systems using highly traded currencies. In short, from a corporation’s perspective, these countries are simply better in nearly every aspect than any other tax haven option – more stable, more connected, and more tax-advantaged.

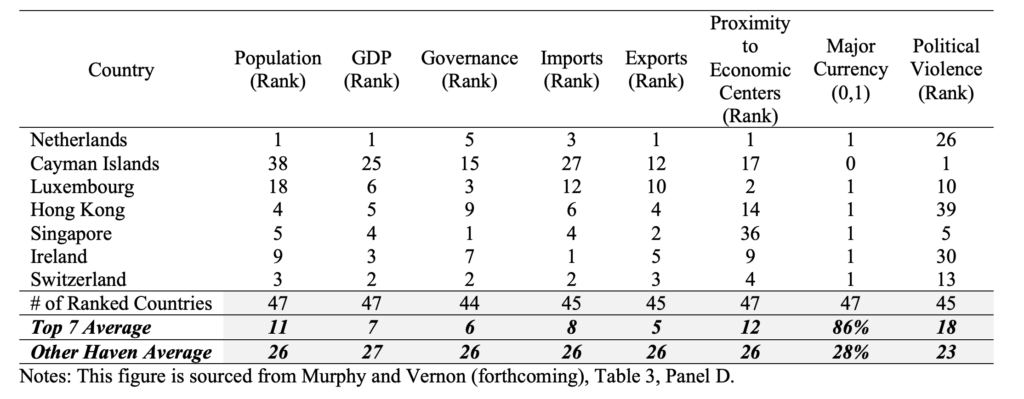

Additionally, many of the smaller tax havens have what we view as a fatal flaw. For example, it is hard to envision tax planners opting to route a transaction through a country involved in numerous armed conflicts when there are safer options. We include a table ranking the tax havens in our study across several non-tax attributes – lower numbers represent a better outcome. Despite all the countries in our sample providing some degree of tax benefit, these also provide legitimacy, proximity to economic hubs (i.e., U.S., Germany, and China), and stability.

Implications for a Changing Tax World

Our findings represent a period (1996-2021) when international tax planning became both incredibly sophisticated (view the ICIJ website, searching LuxLeaks for hundreds of examples[1]) and insatiably lucrative. Watching the taxable funds seemingly flow swiftly out the front door, policymakers have taken action and continue to implement policy addressing the public finance threat of tax haven use over this period.

The OECD has proposed a series of action items under their Base Erosion and Profit Shifting (BEPS) initiative. Two key Pillars from BEPS are now being slowly implemented globally (another Tax Policy Network article explains these plans in more detail).

As tax laws shift worldwide, which tax havens are the most economically impactful will likely change over time. Policies change strategies. But the U.S. ingenuity does not stop at the assembly line or world-altering technology. Corporations will undoubtedly pivot and determine how to engineer new strategies and structures to take advantage of the evolving global tax landscape to achieve tax efficiency and move capital worldwide.

Conclusion

In conclusion, academics and policymakers need to stay fully informed as to what and where tax planning is taking place to make accurate empirical inferences and create effective global tax policy. Treating all corporate tax havens as equal threats misses the point: most activity is concentrated in a handful of jurisdictions, making it like searching for loose change under the couch while ignoring the wallet on the counter.

Our research is not without caveats. First, we take a U.S. corporation perspective. Other tax havens may cater to corporations headquartered in different countries. Second, individual taxpayer tax evasion was not considered. Tiny islands in the Caribbean may be an excellent choice for these activities despite not being high on corporations’ usage priorities. To this angle, we provide no evidence.

References:

Murphy, F. and M. E. Vernon. 2026. The Rich Get Richer: An Examination of Tax Haven Concentration and the New “Top 7”. The Accounting Review, forthcoming.

[1] Found at https://www.icij.org/investigations/luxembourg-leaks/explore-documents-luxembourg-leaks-database/