It’s Possible to Earn a Billion Dollars

Recently, Senator Alexandria Ocasio Cortez opined that it was impossible to “earn” a billion dollars. Robert Reich posted on X that it is not a long list of ways one can become a billionaire: monopoly, insider trading, political payoffs, fraud, and inheritance. That list is much too short. There are other ways to become a billion dollars, many of which involve “earning it”.

A longer list would have to take into account the fortunes of people like Taylor Swift, Oprah Winfrey, Rihanna, Tyler Perry, LeBron James, Jay-Z, Kim Kardashian, Steven Spielberg, and George Lucas, all, at least according to Forbes, billionaires. Their fortunes did not come from forcing people to buy their products. They came from songs, movies, shows, cosmetics, performances, stories, and brands that millions of people voluntarily purchased.

One can argue about whether any person “deserves” a billion dollars. That is a moral and philosophical question. But it is much harder to argue that these fortunes were not earned. Taylor Swift did not inherit a billion-dollar concert tour—through talent, luck, and vibes, she pleased the ears of hundreds of millions of people willing to pay to listen. Oprah did not inherit a national audience—through grit and determination, over a long time, she built a media empire. Tyler Perry did not inherit a studio. These people became extraordinarily rich because they created something other people valued, and because the scale of modern markets allows successful creators to reach millions, or even billions, of customers.

But let’s not beat around the bush by choosing only the most sympathetic billionaires. Let’s talk about one of the richer and more controversial ones: Jeff Bezos. Bezos is not a pop star. He is not a beloved athlete. He is the founder of Amazon, where his wealth comes from. And Amazon is easy to criticize. It is big. It is powerful. Its drivers pee in bottles (on one occasion at least). It has fundamentally changed retail, labor markets, local businesses, advertising, cloud computing, and logistics. Certainly, some of those changes deserve scrutiny.

But it is also worth saying something that critics often skip: Amazon became huge because people found it incredibly useful. For many Americans, Amazon turned shopping from an errand into a search bar. For elderly people, people with disabilities, parents with sick kids, people without reliable transportation, and people living far from specialty stores, the ability to have household goods, medicine cabinet items, books, groceries, replacement parts, and gifts delivered to the door is not a trivial convenience. It is a real improvement in daily life. Online shopping can reduce the travel, planning, and physical-store barriers faced by many people.

When people like something, and they voice their preferences with their dollars—no one forces them to shop on Amazon, and yet, they do. And, while the owners of shops and stores that provide goods at a higher cost might not like it, consumers are much better off for it. Millions of people clicked “Buy Now” because the product was cheaper, faster, easier, or more available than the alternative. That is not fraud. It is not insider trading. It is not inheritance. It is not a political payoff. It is the mundane miracle of voluntary exchange, repeated billions of times.

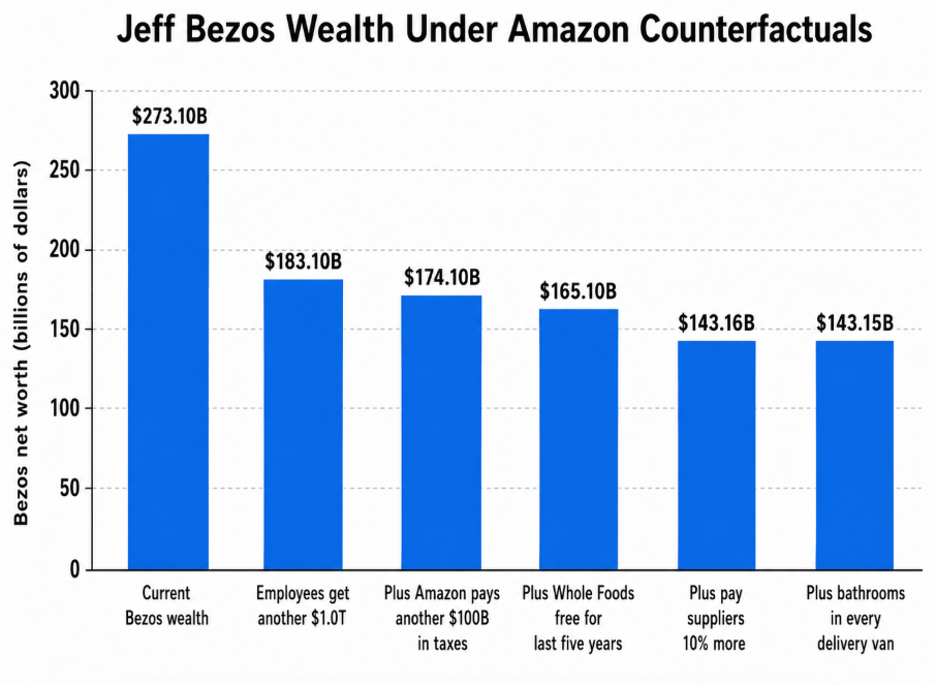

But how did the stuff get so cheap, and get delivered so quickly? Perhaps Bezos is rich because Amazon paid its employees too little, paid too little in taxes, charged customers too much, used its market power to squeeze suppliers, and made drivers pee in bottles. Fine. Let’s adjust for those problems as aggressively as possible, taking action today to remedy all the wrongs of the past. Suppose Amazon sent a check today to every current and former employee equal to all the compensation Amazon had already paid them over its entire history—roughly another $1 trillion. Using the simple assumption that Bezos owns 9 percent of Amazon, that would reduce his wealth by about $90 billion, from $273.1 billion to $183.1 billion. Now assume Amazon also paid another $100 billion in taxes—roughly tripling what it has paid in cumulative corporate income taxes. That would cut Bezos’s wealth by another $9 billion, leaving him with about $174.1 billion. Now assume Amazon refunded every dollar of Whole Foods sales for the last five years—making groceries free for every Whole Foods customer over that period. That would knock off another $9 billion, leaving Bezos with about $165.1 billion. Next, assume Amazon had paid suppliers 10 percent more for everything it ever sold, adding roughly $243.7 billion in historical cost of goods sold. At 9 percent, that would reduce Bezos’s wealth by about $21.9 billion, leaving him with about $143.2 billion. Finally, let’s add a $5,000 personal bathroom in each of Amazon’s 30,000 delivery vans, for a total cost of $150 million. Bezos’s 9 percent share of that cost would be only about $13.5 million, leaving him with roughly $143.15 billion. Even after all five adjustments—another $1 trillion for employees, another $100 billion in taxes, five years of free Whole Foods, 10 percent more for suppliers, and 30,000 delivery-van bathrooms—Bezos would still be worth well over $100 billion. These are not small adjustments. They are enormous, deliberately punitive assumptions. Yet the basic fact remains: even after paying workers, governments, customers, and suppliers vastly more, Amazon still would have created enough value to leave its founder one of the richest people on earth.*

That does not settle every tax question. We can still ask whether billionaires should pay more in taxes, and what those taxes should look like, whether capital gains should be taxed differently, whether inheritances should face higher taxes, or whether monopoly profits should be treated differently from competitive profits, etc. But we should start from a more robust premise. Some billionaires are rich because they extracted wealth. Some are rich because they inherited it. But many became rich because they created enormous value for enormous numbers of people. A serious tax policy debate should be able to admit that.

* Some details on my calculation: The figure reports a deliberately aggressive set of counterfactual calculations intended to ask how much Jeff Bezos’s wealth would remain if Amazon had shared vastly more of its historical value with employees, governments, customers, and suppliers. The starting point is Bezos’s estimated net worth of $273.1 billion. For simplicity, the calculation assumes Bezos owns 9 percent of Amazon. Rather than modeling changes in Amazon’s market capitalization, each counterfactual simply takes the added cost to Amazon, multiplies it by 9 percent, and subtracts that amount directly from Bezos’s wealth. Thus, each bar is calculated as: Bezos counterfactual wealth = Bezos current wealth – 9% × cumulative added counterfactual cost. The first adjustment assumes Amazon immediately sends a supplemental check to current and former employees equal to all compensation Amazon has already paid them over its history. Because Amazon does not disclose one clean cumulative payroll number, I estimate this using Amazon’s disclosed employee counts and a segment-by-segment compensation model. The estimate divides Amazon employment into fulfillment/logistics/customer service, corporate/offices, AWS/cloud/data centers, and Whole Foods/grocery/physical stores, and assigns rough all-in compensation amounts to each category over time. This produces an estimated cumulative compensation total of about $1.0 trillion. As a reasonableness check, Amazon’s cumulative sales over its history are about $4.643 trillion, so a $1.0 trillion compensation estimate would imply lifetime compensation equal to about 21.5 percent of revenue, which is plausible for a company combining retail, logistics, grocery, cloud computing, software engineering, advertising, customer service, and corporate infrastructure. Under the 9 percent ownership assumption, this additional $1.0 trillion employee payment would reduce Bezos’s wealth by $90.0 billion, from $273.1 billion to $183.1 billion. The second adjustment assumes Amazon paid an additional $100 billion in income taxes. Amazon’s cumulative income tax expense in the spreadsheet is roughly $48.8 billion over 1995–2025, so adding another $100 billion would roughly triple Amazon’s cumulative income tax payments. Under the 9 percent ownership assumption, this tax adjustment reduces Bezos’s wealth by another $9.0 billion, from $183.1 billion to $174.1 billion. The third adjustment assumes Amazon gave customers a 100 percent refund for all Whole Foods physical-store sales over the last five years. Amazon does not disclose Whole Foods revenue separately, so the calculation uses Amazon’s “Physical stores” sales as a proxy, which totaled roughly $100 billion over the last five fiscal years. Under the 9 percent ownership assumption, this customer-refund adjustment reduces Bezos’s wealth by another $9.0 billion, from $174.1 billion to $165.1 billion. The fourth adjustment assumes Amazon paid its suppliers 10 percent more for everything it ever sold. The spreadsheet reports cumulative historical cost of goods sold of approximately $2.437 trillion, so a 10 percent supplier premium equals about $243.7 billion. Under the 9 percent ownership assumption, this supplier adjustment reduces Bezos’s wealth by about $21.9 billion, from $165.1 billion to $143.16 billion. The fifth and final adjustment assumes Amazon spent an additional $150 million adding bathrooms to every delivery van, based on 30,000 vans and $5,000 per bathroom. Under the 9 percent ownership assumption, this reduces Bezos’s wealth by only about $13.5 million, from about $143.16 billion to about $143.15 billion. These calculations are intentionally mechanical and punitive. They do not model general equilibrium effects, taxes on Bezos personally, changes in Amazon’s growth path, investor discounting, behavioral responses, financing choices, or the possibility that higher wages, lower prices, higher supplier payments, or better working conditions could themselves increase productivity, demand, retention, or goodwill. The purpose is not to provide a precise valuation model, but to show scale: even after assuming Amazon doubled its estimated lifetime employee compensation, roughly tripled its cumulative income tax payments, refunded five years of Whole Foods physical-store sales, paid suppliers 10 percent more over its entire history, and added bathrooms to every delivery van, Bezos would still be worth about $143 billion under this simple 9 percent ownership approach. I thank Will Yoder for inspiring this piece.