Are Profitable Corporations Underpaying Their Taxes?

A recent study by ITEP claims that many publicly traded firms pay no federal income taxes, despite reporting substantial pretax profits to their shareholders. Is this an open-and-shut case of large corporations failing to pay their fair share of taxes, or is there something more subtle (and interesting) happening here?

Let’s start our examination by considering the evidence ITEP presents, which consists primarily of two numbers, pretax profits and cash taxes paid to the federal government. The pretax profit comes from firms’ financial statements, which are based on generally accepted accounting principles (GAAP). These statements are intended to represent, as near as possible, the economic pretax profit each firm generates each year. Importantly, to best approximate economic profit, these financial statements do not rely solely on cash payments and cash receipts. Instead, they recognize revenue when it is earned (regardless of when the revenue is received) and the statements recognize expenses when they are incurred (regardless of when paid). These accrual rules are essential to match revenue with the related expenses, and they are also intended to place activities within the correct reporting year.

Complexity arises when these carefully constructed pretax profit amounts are compared to cash taxes paid during the year. The issue is that there is no assurance that the cash taxes paid relate solely (or even partially) to that year’s economic profits. If there are timing mismatches between the pretax profit amount and the taxes paid, it may appear that a firm is underpaying (or overpaying) its expected taxes.

The simplest and most well-known example of this mismatch issue involves tax loss carryforwards. Under U.S. tax law, corporations that generate a loss do not receive a refund from the government, at least not directly. Instead, firms are allowed to carry forward the tax loss to later years, reducing future years’ taxable profits. This common situation can make cash taxes paid in profitable years appear too low.

NOL Carryforward Example

The following example illustrates how a net operating loss (NOL) carryforward distorts a cash tax based effective tax rate methodology. A firm incurs a $100 loss in Year 1 and a $200 profit in Year 2. There are no book-tax differences.

| Year 1 | Year 2 | Combined (Yr 1+2) | |

| Pretax income / (loss) | ($100) | $200 | $100 |

| Less: NOL carryforward | — | ($100) | — |

| Taxable income | ($100) | $100 | $100 |

| Cash tax paid (21%) | $0 | $21 | $21 |

| Cash ETR | 0% | 10.5% ($21/$200) | 21% ($21/$100) |

| Statutory rate | 21% | 21% | 21% |

| Apparent gap vs. statutory | — | −10.5 pp | 0 pp |

Key takeaway: When evaluated in isolation, Year 2 shows an apparent cash effective tax rate of $21/$200 = 10.5%, half the 21% statutory rate, because the NOL carryforward from Year 1 reduces taxable income below book income. However, looking at the whole picture, over both years, cumulative pretax income is $100 and total tax paid is $21, yielding an effective rate of exactly 21%. The firm has not underpaid its taxes; instead, the single-year cash-paid tax rate is downwardly biased and can be misleading.[1]

So, if using cash taxes can give misleading results, what is the alternative? An ideal tax burden measure would be synchronized with the pretax profit reported each year, to avoid these year-to-year mismatches. It would also consider all income taxes, not for just one or two jurisdictions, to provide a more complete understanding of the firm’s total tax burden. Fortunately, there is no need to create a new metric from scratch; GAAP provides a well-calibrated measure of the current year’s tax burden: GAAP tax expense. GAAP tax expense is an accrual measure, meaning that it is not based solely on cash tax payments. Instead, it considers both taxes that have been incurred (but not yet paid) as well as tax benefits generated (but not yet received). One feature of this measure is that it is computed for us and reported in each public firm’s financial statements. Furthermore, each public firm is required to reconcile the overall effective tax rate (computed with this measure) to the 21 percent federal statutory tax rate showing, in detail, the specific reasons a firm’s taxes are higher or lower than expected. For anyone interested in why firms are paying more or less than the expected level of tax, this is the best place to start.

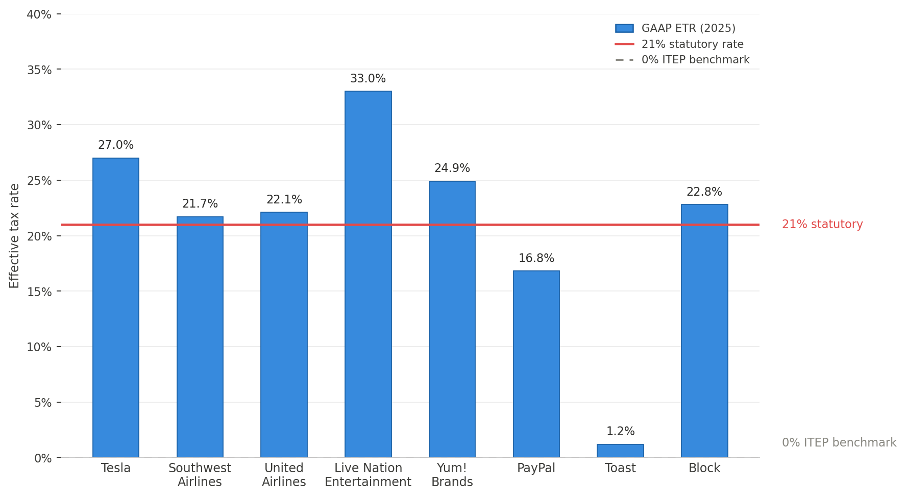

So, what insight does this measure provide? The ITEP report lists 88 firms that have large pretax profits but no cash tax payments. That report highlights eight firms (Tesla, Southwest Airlines, United Airlines, Live Nation Entertainment, Yum! Brands, PayPal, Toast and Block), so I also focus on those same highlighted firms. Based on the logic above, I focus on their GAAP effective tax rate (ETR) as our measure of tax burden.

2025 GAAP Effective Tax Rates vs. Statutory and Cash Tax Benchmarks

The chart below shows the 2025 GAAP effective tax rates (ETRs) for a sample of corporations highlighted in ITEP reporting, comparing those GAAP ETRs against the 21% federal statutory corporate tax rate and the 0% cash tax benchmark.

These tax burdens are higher than the zero percent cash effective tax rates that ITEP reports, and six of the eight highlighted firms have GAAP effective tax rates higher than the federal statutory rate. Incidentally, other than PayPal and Yum! Brands, all these highlighted firms have material domestic net operating loss carryovers at the end of 2025. This means that using cash tax measures in the future can generate downwardly biased tax burden estimates.

The advantage of using cash taxes paid as a measure of tax burden is that it is simple. The disadvantage is that the cash tax payments may not relate to the year of payment, making each year’s calculations suspect. In contrast, the GAAP tax expense measure is designed to associate the correct tax burden with the corresponding pretax profit, helping to ensure that the ratio of GAAP tax expense to GAAP pretax income in each year is meaningful.

[1] Prior year tax losses are not the only reason that cash taxes paid can fail as a measure of the current year tax burden. Other common situations include settlement of tax audits of prior years, or the late payment of the current year’s taxes after year end, due to imprecision in estimated tax payments. In these situations, note that at least two years are being distorted in every case, not just one year. This adds to the mismeasurement issue.

[2] Even though PayPal has a GAAP effective tax rate of less than 21 percent for 2025, the financial statement disclosures show that it paid $535 million in federal income tax payment on $1,453 million in U.S. profits, for a cash tax rate of about 37 percent, well above the 21 percent statutory tax rate. This is a good example of the limitation of cash tax payments to determine a firm’s tax burden. Also, since the firm paid cash taxes to the U.S. for the year, it probably should not have been included in the ITEP list, which is supposed to include only firms making no federal tax payments.

[3] Virtually all the difference between Toast’s 1.2 percent effective tax rate and the 21 percent statutory rate arises from share-based payment awards (stock option exercises). While this does save the firm taxes at the 21 percent corporate tax rate, the executive likely has corresponding income taxed at rates as high as 37 percent, so this favorable ETR represents a net win for the taxing authority, rather than a loss. This helpful detail is visible in the GAAP effective tax reconciliation table, but it is not observable when using cash taxes paid.