Private Equity in Accounting – Not Just Another Business

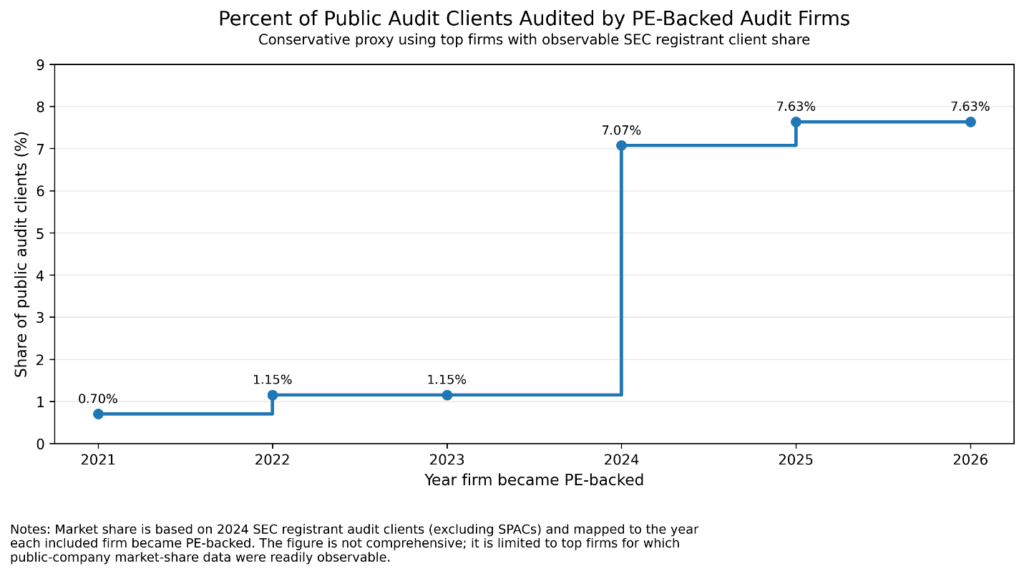

Private equity has purchased accounting firms at a remarkable pace.[1] For some observers, that is just the latest example of financial capital flowing into a fragmented industry. For others, it raises a deeper question: should the ownership of certain professional service firms be treated differently from the ownership of traditional businesses?

That question is especially important in accounting. If private equity buys a chain of restaurants, society may worry about prices, wages, or product quality.[2] But if private equity buys accounting firms, the stakes are higher. Accountants and auditors play a public-trust role in the economy. They help determine whether financial statements are reliable, whether tax positions are credibly supported, and whether investors and regulators can trust what firms report.

That is why the debate over private equity ownership in accounting should not be reduced to a simple ideological issue. The question is whether certain ownership structures create incentives that are poorly matched to professions that serve an important public function.

My own research suggests the answer is yes.

To be clear, private equity is not always a villain. Private equity firms often identify opportunities to improve the operations or governance of the businesses they acquire. In other work, I find evidence that private equity can sometimes improve corporate value by easing short-term market pressures.[3] In that setting, private equity takeovers of public corporations are associated with less focus on short-term earnings, more investment in R&D, and higher productivity. That evidence is important because it shows that concentrated ownership and access to capital can, in some contexts, support longer-run decision-making rather than undermine it.

But accounting is a different setting.

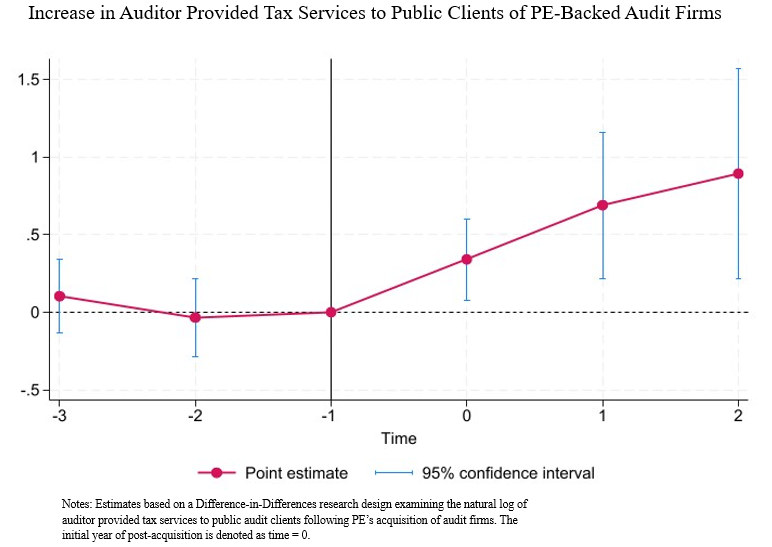

In recent research on private equity ownership in public accounting, my co-authors and I examine what happens when private equity acquires accounting firms with public clients.[4] Private equity is in the business of buying firms, changing incentives, and eventually exiting with gains. Consistent with that model, we find that private equity significantly increases audit firms’ sales of tax services to their audit clients. That is consequential because the same firm is both advising the client on tax planning and compliance and judging the financial reporting consequences of that advice.

Increased tax services, by itself, is not necessarily problematic. There is reason to think private equity can improve accounting firms’ capabilities. A private equity sponsor with a broad portfolio may help an audit firm deepen industry expertise, invest in technology, and expand the scale of its tax practice. Breadth across many portfolio companies may also give private equity-backed audit firms wider exposure to tax-planning strategies and implementation experience. In that sense, private equity could make tax services genuinely more valuable to clients.

My research does find some evidence consistent with that expertise channel. The increase in auditor-provided tax services is strongest where auditors lacked prior regional industry tax expertise, suggesting that private equity may help firms access or deploy specialized tax knowledge.

But the broader pattern of results is harder to explain with expertise alone and points more strongly to changes in judgment.

Private equity ownership reduces partners’ downside exposure while putting more weight on growth and billing. That combination can make partners more willing to sell tax services and more willing to accept aggressive judgments around the financial reporting for those positions. This matters because aggressive tax strategies are often uncertain, and firms are supposed to reflect that uncertainty in reserves that reduce reported earnings.[5] If auditors become more permissive, clients can report lower tax expenses without bearing the full reporting consequences of that uncertainty.

That is consistent with what I find. Public companies that purchase tax services from private-equity-backed auditors report lower GAAP tax expense without comparable reductions in cash taxes paid, lower reserves for tax uncertainty, and a greater likelihood of subsequent tax-related financial misstatements. In other words, these clients appear to receive reporting benefits up front that later prove difficult to sustain. That pattern is hard to explain as benign expertise alone. It is more consistent with private-equity-backed auditors becoming more permissive in the judgments that surround the tax services they sell. That should matter to shareholders. Investors rely on auditors to ensure that reported earnings reflect economic reality, not aggressive assumptions that simply flatter the numbers. If tax-related judgments become more permissive, shareholders may see stronger reported earnings without any matching improvement in underlying cash flows.

Supporting evidence points in the same direction. In my research, the increase in auditor-provided tax services is strongest where one would expect a leniency story to matter most: among clients with weaker external monitoring and lower general financial reporting quality. That suggests these services become especially valuable when aggressive reporting is less likely to be detected or challenged.

That is why accounting is different from ordinary businesses.

When incentives distort judgment in accounting, the effects spill beyond the accounting firm and its owners to the clients’ shareholders, creditors, and regulators who rely on credible financial statements. Once that is true, ownership in accounting is no longer just a private contracting matter; it becomes a question of how to protect the integrity of information on which public markets depend.

Defenders of the current system may point out that private equity-backed accounting firms use an Alternative Practice Structure, under which the audit practice remains fully owned by CPAs. That is true as a formal matter. But my research shows why formal separation is not the same as economic separation. In these structures, the audit entity sends its profits to a private equity-controlled non-audit entity through shared-services agreements, audit partners still share in the economics of that broader platform, and private equity can influence firm-wide growth targets, budgets, and resource allocation. The result is that CPA ownership may remain intact on the organizational chart even as the commercial incentives surrounding audit judgment are shaped elsewhere.

Private equity may bring capital, scale, and expertise. But when the business depends on independent professional judgment, the first question should not be how much growth a new owner can generate, but whether that owner’s incentives are compatible with the duty to exercise judgment on behalf of the public. For audit and closely related tax services, initial evidence suggests those incentives deserve much closer scrutiny.

[1] https://www.thomsonreuters.com/en-us/posts/tax-and-accounting/private-equity-accounting-firms/

[2] https://www.cnbc.com/2025/02/25/red-lobster-tgi-fridays-bankruptcies-private-equity.html

[3] Hribar, P., Kravet, T., and Krupa, T. 2025. Earnings myopia and private equity takeovers. Review of Accounting Studies 30: 994-1035. https://doi.org/10.1007/s11142-024-09844-6

[4] Cui, J., Kleppe, T., and Krupa, T. 2026. Private equity ownership in public accounting: enhanced expertise or a threat to auditor independence? Working paper, available at SSRN: https://ssrn.com/abstract=6410258

[5] Dyreng, S., Hanlon, M., Maydew, E. 2019. When does tax avoidance result in tax uncertainty? The Accounting Review 94 (2): 179-203. https://doi.org/10.2308/accr-52198