Can Tariffs Replace the Individual Income Tax?

“And as time goes by, I believe the tariffs, paid for by foreign countries, will, like in the past, substantially replace the modern-day system of income tax, taking a great financial burden off the people that I love.” — President Donald Trump, State of the Union Address, 2026

President Trump’s statement draws on a historical comparison and suggests that if tariffs comprised a larger portion of federal tax collections, individuals would benefit. However, a proposal to replace the modern individual income tax system with tariffs raises fundamental concerns. The economic burden of tariffs falls disproportionately on lower-income households, and tariffs do not raise sufficient or stable revenues that can serve as a plausible substitute for the individual income tax.

What Is a Tariff, What Is It For, and Who Pays?

A tariff is a tax levied by a government on imported goods, typically expressed as a percentage of value. By increasing the price of foreign goods, tariffs may protect domestic industries from foreign competition, address perceived unfair trade practices, and generate government revenue.

Although tariffs are legally imposed on importers, the economic burden is often borne in substantial part by domestic consumers and businesses through higher prices. The precise degree of pass-through varies across products and market conditions, but the conventional view is that tariffs are not simply paid by foreign governments (or their citizens). Recent estimates suggest that the current U.S. tariff regime imposed an average burden of between $1,000 and $1,230 per U.S. household in 2025.

Distributional Effects

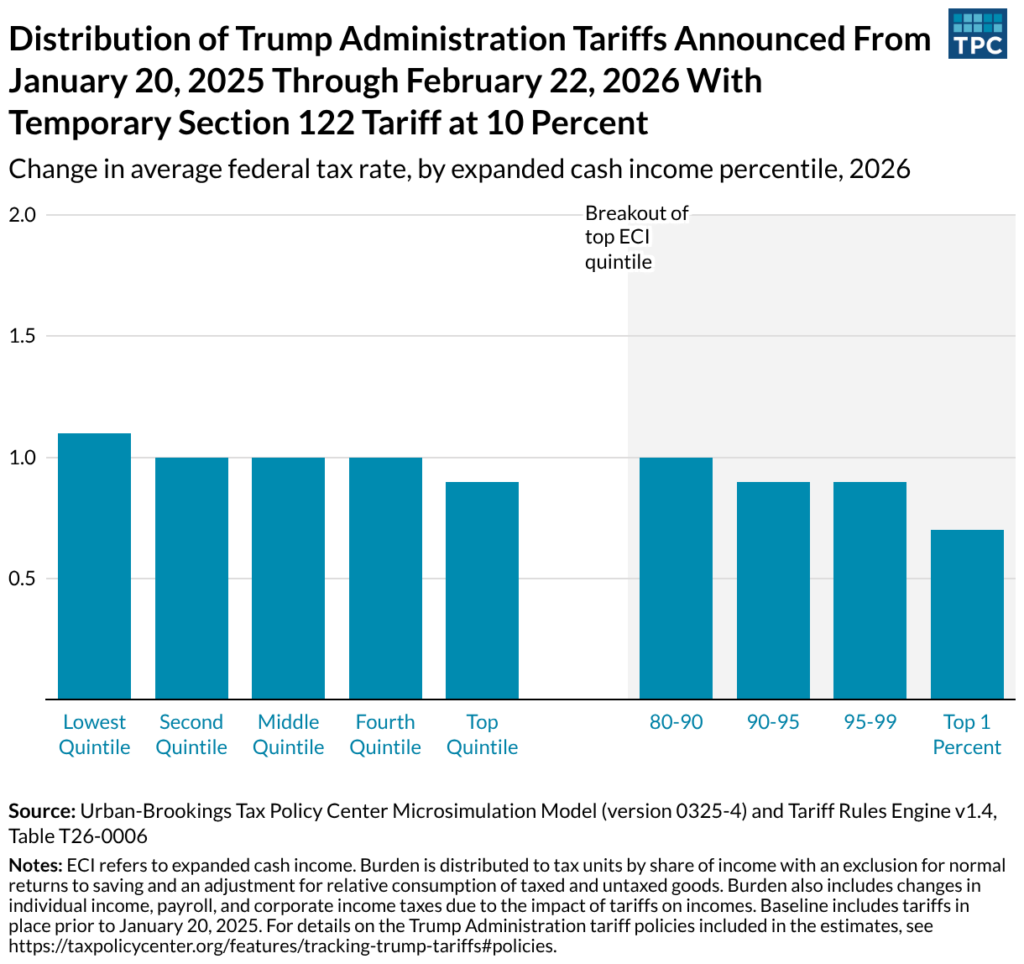

Tariffs are generally regressive, falling hardest on households with the lowest incomes. In 2026, tariffs raised the effective federal tax rate by 1.1 percentage points for households in the bottom income quintile compared to only 0.9 percentage points for those at the top. That modest difference understates the true inequity, however. Lower-income households spend a far greater share of their income on goods in categories that are most heavily exposed to tariffs, including essentials like clothing, textiles, and food.

In contrast, the income tax is intended to be progressive. The top 1 percent of earners pay an average federal income tax rate of approximately 23.1 percent, whereas the bottom half of taxpayers pay roughly 3.7 percent. Replacing income taxes with tariffs would not remove a financial burden from working people. Instead, it would shift the federal tax burden down the income distribution.

Revenue Comparisons

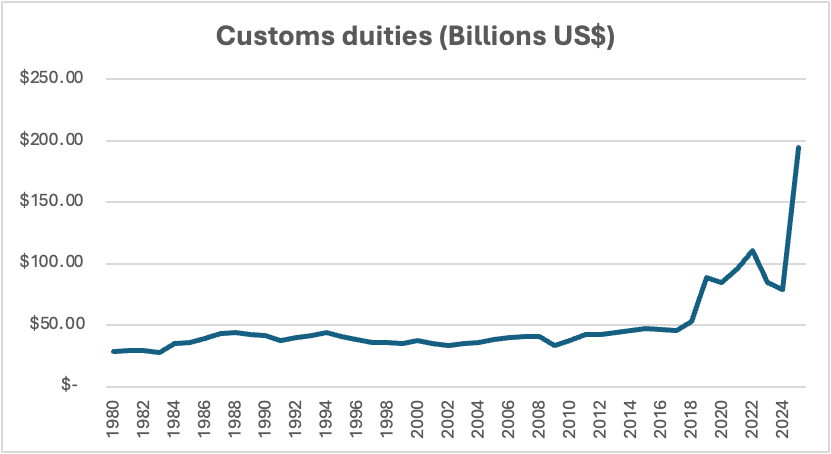

Current tariff revenues are only a fraction of individual income tax revenues. In fiscal year 2025, the federal government collected approximately $2.66 trillion in individual income taxes. Even in the most comprehensive tariff environment of the modern era, before the Supreme Court’s February 2026 ruling struck down tariffs imposed under the International Emergency Economic Powers Act (IEEPA), estimated annual tariff revenue for 2026 was only $246 billion.

The gap between tariff revenue and income tax revenue is not a rounding error — it is a ratio of nearly 11 to 1. Closing that gap would require imposing tariffs so expansively that they would either substantially reduce import volumes, thereby shrinking the tax base, or significantly increase consumer prices. Either outcome would undermine the claim that tariffs can function as a realistic substitute for the individual income tax.

Historical Context

President Trump’s historical comparison is not wrong, but it is incomplete. Before the ratification of the Sixteenth Amendment in 1913 to establish the federal income tax, tariffs were the primary source of federal revenue, at times generating 50 percent or more of all federal collections.

But the federal government of that era was fundamentally smaller and more limited in function than the one that exists today. Federal spending in the pre-income-tax era amounted to approximately 2–3 percent of GDP. Today it is over 20 percent. The federal government of today finances a range of services and institutions that did not exist in their present form in the early nineteenth century. Thus, the fact that tariffs once supported a significant portion of federal expenditures does not necessarily mean they could do so under current fiscal conditions.

Administrative and Institutional Considerations

Beyond regressivity and extreme estimated revenue shortfall, three additional operational realities deserve attention. First, although tariffs are often characterized as simpler than an income tax, they still impose compliance costs on multinational businesses with global supply chains. These costs, like the tariffs themselves, can ultimately be passed on to consumers.

Second, tariffs are often praised for being simpler to collect and harder to evade than income taxes. But when any tax becomes high enough, it incentivizes avoidance. In 2025, the U.S Department of Justice announced the creation of a new Trade Fraud Task Force to investigate and prosecute criminal tariff evasion, which includes falsifying goods’ value, country of origin or classification to minimize or avoid tariffs. These activities threaten tariff revenue and raise enforcement costs.

Third, revenue stability is compromised under a tariff-dominated regime. Before the Supreme Court’s ruling invalidating IEEPA tariffs, estimated tariff revenues for 2026 were $246 billion. After the ruling, Yale’s Budget Lab projected revenues would collapse by nearly 95 percent, to only $13 billion. The Trump administration has since announced its intent to impose new tariffs under alternative legal authorities, which could push revenues back toward earlier, higher estimates. In short, tariff revenues under the current regime can swing by hundreds of billions of dollars depending on a single court ruling or executive action. Relying on tariffs for the bulk of government revenue creates volatility that makes it difficult to effectively plan. Statutory income taxation, in contrast, rests on a more stable foundation and is less vulnerable to abrupt executive actions or shifting legal authorities.

Conclusion

Well-designed tariffs can achieve legitimate policy goals, including protecting domestic industries, responding to unfair trade practices, and raising modest revenue. But they are not well suited to replace the individual income tax. Their regressive effects, narrow tax base, and unstable revenue make them a poor substitute.