Why should we care about partnership businesses?

In the landscape of American tax law, entities organized as C corporations often grab the headlines. Debates over the 21% flat rate, double taxation, and corporations paying their fair share dominate. However, the true engine of modern finance, real estate, and professional services is far more elusive: the partnership. Governed by the notoriously difficult Subchapter K of the Internal Revenue Code, partnership taxation has evolved from a niche specialty into a powerful tool for tax planning and significant challenge facing tax authorities.

A key feature: flexibility

Technically, a partnership is not a taxpayer; it is a “flow-through” (or pass-through) entity. Unlike a C corporation, which pays taxes at the entity level before distributing dividends to shareholders, a partnership calculates its income or loss and then “flows” those amounts out to its partners. Each partner then reports their share on their individual tax return. While 80% of partnerships are single partnerships owned exclusively by individuals, the remaining 20% exist in “spiderwebs”—complex, multi-tiered structures where partnerships own other partnerships in a large array of overlapping tiers comprised of hundreds or thousands of entities and individual owners.[1] Partnerships then have the flexibility to strategically allocate gains and losses among partners, which cost the federal government $200 billion from 2011-2020.[2]

This flexibility is the hallmark of the partnership. For example, under certain U.S. Treasury regulations (known as “check-the-box” regulations), a wide variety of entities, such as Limited Liability Companies (LLCs), can simply elect to be treated as partnerships for tax purposes. This allows them to avoid the double-taxation trap while maintaining the liability protection of a corporation.

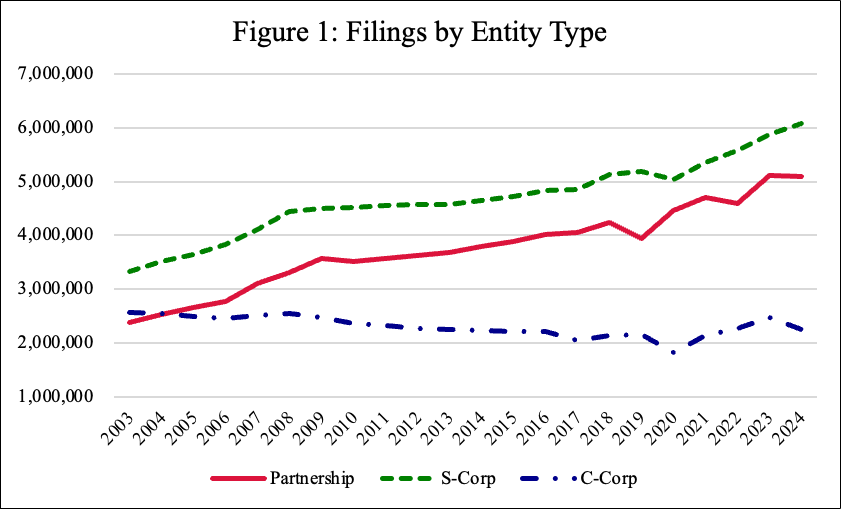

Growth in partnership use

To understand the importance of partnership taxation, we simply have to look at the scale of the data. Over the last two decades, there has been a massive shift away from traditional C corporations toward pass-through entities. In 2003, there were slightly more C corporations (2.5 million) than partnerships (2.4 million). However, by 2024, partnerships outnumbered C corporations by more than 2-1, with over 5 million partnerships filing returns, representing more than $50 trillion in assets. Figure 1 details the growth across entity types by year.

Partnerships are the vehicle of choice for:

- Real estate: Almost every major commercial development is structured as a series of tiered partnerships, and this industry accounts for about half of all partnerships.

- Private equity and hedge funds: More than half of all partnership assets are held by financial partnerships that manage trillions in global capital.

- Large professional firms: Law, accounting, and architecture firms are commonly structured as partnerships.

Partnership Contribution to the Tax Gap

The sheer number of partnerships, volume of wealth, and complexity of ownership structures means that partnerships contribute significantly to the “tax gap” — the difference between the tax that is owed and is paid. For 2022, the tax gap was estimated to be $696 billion. Flow-through entities (including partnerships and S corporations) are estimated to contribute $194 billion to this amount. Michael Love, an Associate Professor at Columbia Law School, provides evidence on where some of this money goes. Over $1 trillion flowed from U.S. partnerships to tax havens between 2011 and 2019, much of it escaping taxation entirely.[3]

Partnership Audits and Enforcement

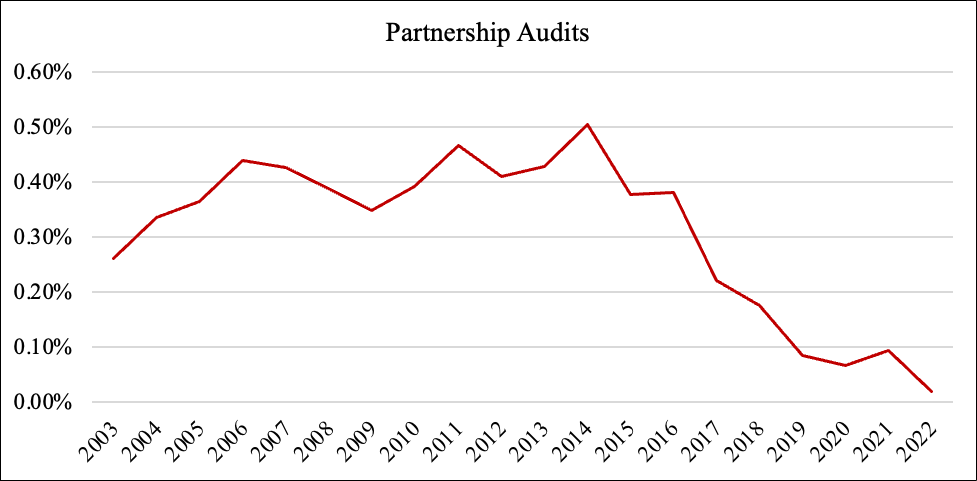

Despite the size of noncompliance from flow-throughs, due to IRS resource constraints, the audit rate of partnerships is at historic lows. Since 2002, an average of about 13 thousand partnerships are audited per year, which represents only ~0.3% of all partnerships. Figure 2 details partnership audit rates by year. The challenge for tax authorities is not merely the number of entities, but the lack of transparency inherent in tiered structures. Because these “spiderwebs” can span multiple jurisdictions, it can be difficult to identify the ultimate beneficial owner of the income, allowing complex arrangements to remain shielded from routine oversight even when the potential for tax recovery is high.

Figure 2: Partnership Audit Rates

This does not mean audits do not yield results. Although complex partnerships are actually less likely to be assessed additional tax when audited, simply because they are so difficult for agents to untangle, when the IRS does successfully audit these organizations the return on investment is nearly $20 per dollar spent—eight times higher than for corporate audits.

Conclusion

As partnerships continue to dominate the economy, partnership taxation represents the intersection of economic efficiency and social equity. On one hand, the flexibility of Subchapter K encourages investment and innovation by allowing bespoke financial arrangements. On the other hand, the complexity of the rules provides a playground for aggressive tax engineering that remains largely inaccessible to the average taxpayer.

Sources

[1] Hess, R., Black, E., Javed, Z., Hennessy, J., Lester, R., Goldin, J., Ho, D., & Portz, A. (2025). The spiderweb of partnership tax structures.

[2] Love, M. (2025). Who benefits from partnership flexibility?. Journal of Public Economics, 251, 105493.

[3] Love, M. (2021). Where in the world does partnership income go? Evidence of a growing use of tax havens.