The One Time Billionaire Tax: A One-Time Fix for a Permanent Problem?

California’s latest proposal to levy a one-time tax on billionaires has ignited the predictable controversial debate. Before taking sides in this debate, it is worth asking a more basic question: even if the tax works as advertised and raises $100 billion, would it solve the problem it is meant to address?

The math suggests otherwise.

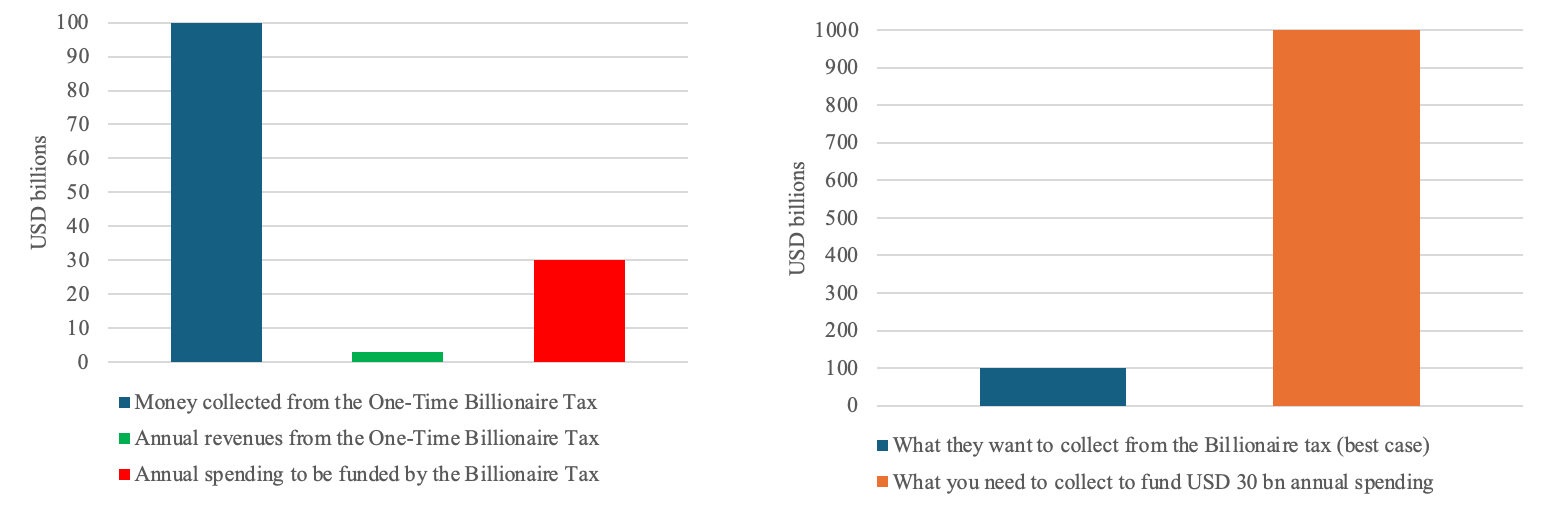

The proposal envisions raising roughly $100 billion through a one-off tax on billionaires. The idea, at first glance, is straightforward: collect the funds and deposit them into a dedicated account. When the time comes, use the proceeds to fund public services. The bill points to substantial funding needs—about $19 billion annually to offset federal cuts to Medi-Cal and another $7 billion to close existing state deficits in Medi-Cal. On top of that, there is an additional (unspecified) amount planned for education and food programs.

Taking these figures at face value—and setting aside the likelihood that actual spending pressures may be higher—California is contemplating ongoing commitments in the neighborhood of $30 billion per year. Against that backdrop, $100 billion, in the most optimistic scenario, would last just over three years.

The one-time billionaire tax is, at best, a temporary fix.

The mismatch between one-time revenues and recurring expenditures is a well-known principle in public finance. Governments can use temporary inflows, whether from asset sales or one-time taxes, to fund one-off investments: infrastructure, debt reduction, or transitional programs. But using them to finance permanent spending may buy time, but it does not alter the underlying budget constraint. Even if California collects USD 100 billion and invests it at 3% (which is the highest discount rate in Biden’s Climate Discounting), annual revenues are only USD 3 billion, which covers only roughly 10% of the annual spending of USD 30 billion. Hence, in order to generate permanent revenues of USD 30 billion to fund this spending out of the one-time wealth tax, California would have to collect a one-time amount USD 1,000 billion (=USD 30 billion / 3%). This USD 1 trillion is the present value of the future annual spending, and it is ten times the most optimistic one-time wealth tax revenue.

Proponents might respond that three years of funding is better than none, especially in the face of acute needs. That is true, as far as it goes. But it raises a more uncomfortable question: what happens in year four?

There are only a few plausible answers, none particularly reassuring. One is that policymakers return to voters with another “one-time” tax. Policymakers make the one time wealth tax permanent following the principle of “there is nothing more permanent than a temporary solution”. Another is that spending commitments, once established, prove politically difficult to unwind, leading to larger deficits or pressure on other tax bases.

None of these outcomes can be dismissed as far-fetched. Indeed, the political economy of public spending suggests the opposite: once programs are created and beneficiaries mobilized, cutting expenses is rare and hard for policymakers. The temptation to front-load spending—drawing down the windfall more quickly than planned—is also real. Fiscal discipline is easiest to promise in advance and hardest to maintain in practice.

How much will be really collected?

The headline figure of $100 billion rests on very optimistic assumptions about both the tax base and compliance. Wealth is not as easily measured or taxed as income, particularly at the upper end, where assets are often illiquid, mobile, and legally complex. The $100 billion estimate also rests on the assumption that billionaires stay and do not adjust their behavior. This appears unrealistic. More conservative estimates thus suggest significantly lower revenues and that there may be even a loss in revenues when considering that income tax revenues also decline (see also the Tax Policy Network article). If the collected revenues prove closer to realistic estimates, California could find itself committing to large, recurring expenditures on the basis of a revenue stream that falls short even in the short term.

In that scenario, the policy would not merely fail to solve the problem—it could exacerbate it because the billionaire tax may not even be able to fund one year of the suggested $ 30 billion in spending.

Permanent solutions are required

If the state intends to spend $30 billion annually on healthcare, education, and food assistance, it must identify revenue sources that are equally sustainable and permanent. That may involve difficult choices such as raising sales or income taxes. But it cannot be achieved through a one-time measure, however politically attractive.

Some supporters of the billionaire tax may recognize this implicitly and view the proposal as a first step toward a permanent wealth tax. That, however, opens a different set of challenges. A recurring wealth tax, in particular at rates as high as 5%, raises serious concerns about high effective tax burdens of over 100% of income and economic distortions.

For now, it is enough to note a simpler point. A one-time tax cannot sustainably fund ongoing obligations. California’s fiscal challenges require structural solutions, not temporary fixes.