Why Do We Tax Businesses, and What Types of Taxes Are There?

Benjamin Franklin is credited with saying that nothing is certain except death and taxes. What he did not mention is just how many kinds of taxes there are, especially for businesses. Every sale, every paycheck, every piece of property, every dollar of profit triggers a tax. But why do governments tax businesses in the first place? There are three broad reasons:

- To raise revenue. Governments need to fund roads, schools, national defense, and social programs. In fiscal year (FY) 2025, the U.S. federal government collected $5.23 trillion in tax, the largest amount in the country’s history. Corporate income taxes contributed around $575 billion to the total (about 11% of receipts).[1]

- To shape behavior. Want companies to invest in new equipment? Offer a tax deduction. Want to reduce pollution? Tax carbon emissions. Policymakers can leverage the tax code to nudge businesses toward activities society deems beneficial.

- To redistribute resources. The tax system is the way through which money gets redistributed from one part of the population to other parts. For example, when governments collect taxes and then fund public services or build infrastructure, the government is effectively redistributing wealth across the economy.

Example of Business Taxes

In practice, the tax landscape for businesses is broader than many realize. Most people focus on income tax – tax on how much a business earns – but in practice, businesses get taxed in many ways.

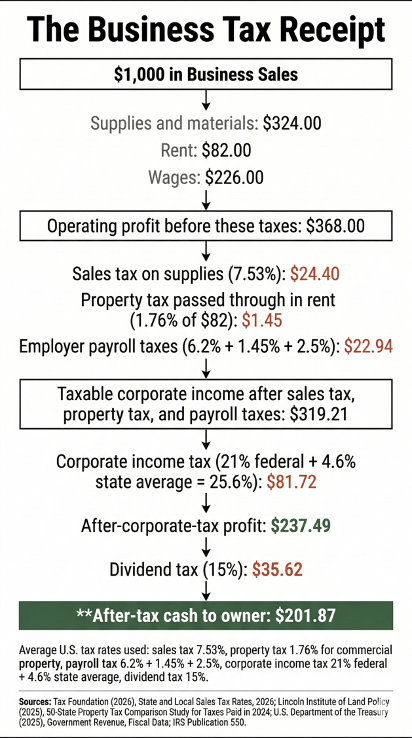

Figure 1 walks through an oversimplified example of a hypothetical business that has $1,000 in sales. This figure illustrates the variety of taxes potentially imposed on such a business.

Let’s follow the money more closely:

Purchasing supplies: Businesses must pay tax on inventory and supplies used in their business, averaging 7.53% combined.[2] While some items might be exempt if the products are immediately resold, many purchases that go into a production process are subject to sales tax. In our example, about $24 in sales tax would be due on the $324 worth of goods and materials. Out-of-state purchases without collected sales tax still trigger “use tax” owed directly to the state from which they were purchased, and imported materials face customs duties at the border.

Setting up shop: A business must pay property taxes on its facilities. Property taxes apply to real estate and, in many states, equipment. These taxes fund local schools, roads, and services. Commercial property averages about a 1.76% effective rate, though it varies widely—from 0.60% in Cheyenne, WY to 4.00% in Detroit, MI.[3] Even if a company does not own its property and instead rents property, a business could effectively pay some portion of the property tax if landlords pass along the tax in the form of higher rent. In our example in Figure 1, roughly $1.45 in property tax would be added onto the rent if all the tax was passed along (and rental rates accurately reflected property values).

Hiring employees: A business must pay payroll taxes for its employees. Employers pay 6.2% for Social Security, 1.45% for Medicare, plus unemployment taxes averaging roughly 2.5%.[4] That’s about $23 on $226 in wages. Employers also withhold income taxes and the employee’s half of payroll taxes on the government’s behalf. Collectively, payroll taxes generate a third of federal revenue at approximately $1.8 trillion annually.[5]

Earning a profit: What remains after costs faces income tax. Assuming that the business is organized as a corporation, that tax would be 21% (federal income tax), plus 4.6% average state rate, for a combined 25.6%.[6] In our example, about $82 goes to income taxes on $319 of pre-tax income. Some cities add local business taxes, and international operations face foreign taxes plus complex crediting rules.

Paying the owner. Distributed profits from corporate entities face dividend taxes of 0%, 15%, or 20% at the individual level, based on the tax bracket of the owner.[7] This “double taxation” means corporate profit is taxed when earned and again when distributed. At the 15% rate, this takes another roughly $36 from our example.

And more taxes…. Figure 1 merely summarizes the broad categories, but a real business might encounter dozens of distinct tax obligations across federal, state, and local jurisdictions. Additional taxes not detailed above include:

- Excise taxes: These taxes target specific types of goods of inputs. For example, businesses with vehicles will pay fuel taxes, which average 51 cents per gallon combined.[8] Other types of excise taxes include utility taxes, environmental taxes, and industry-specific taxes on products such as alcohol and tobacco.

- License and registration fees: Most businesses pay registration and licensing fees to set up a business or operate in a local jurisdictions.

- Other taxes:

- Some states add franchise taxes or gross receipts taxes (which tax total revenue rather than profits). Newer types of taxes include “headcount taxes” – local taxes that tax businesses based on the number of employees they have.

- State disability insurance

- Import/export fees beyond customs duties

- Industry-specific environmental levies, such as superfund excise taxes for hazardous waste cleanup, carbon taxes/pricing in states like California and Washington, and fees for hazardous waste generation and disposal.

- Some states add franchise taxes or gross receipts taxes (which tax total revenue rather than profits). Newer types of taxes include “headcount taxes” – local taxes that tax businesses based on the number of employees they have.

The full tax picture ultimately depends on a company’s location, industry, supply chain, and corporate structure.

How does the U.S. compare internationally?

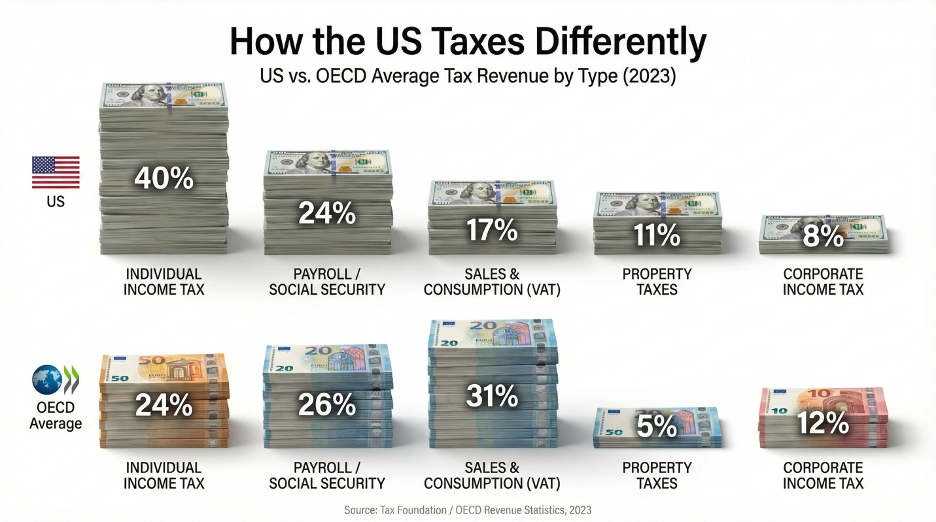

As Figure 2 below shows, the overall U.S. tax structure looks quite different from other developed economies.[9] For these figures, we include all individual income tax as well, especially given that a good chunk of business income (non-corporate income) gets taxed as part of the individual income tax system.

Compared to other developed nations in 2023, the U.S. leans more heavily on income taxes and less on consumption taxes. Individual income taxes account for 40% of U.S. revenue in 2023 versus 24% in the average OECD country, while consumption taxes bring in just 17% compared to 31% abroad.[10]

Business taxation is broad, layered, and touches nearly every stage of a business’ operations. The types of taxes vary—sales, property, payroll, income, excise, etc.—but the pattern is consistent: governments tax what businesses buy, own, earn, and distribute.

References

[1] U.S. Department of the Treasury. (2025). Government Revenue. Fiscal Data. https://fiscaldata.treasury.gov/americas-finance-guide/government-revenue/

[2] Tax Foundation. (2026). State and Local Sales Tax Rates, 2026. https://taxfoundation.org/data/all/state/sales-tax-rates/

[3] Lincoln Institute of Land Policy. (2025, June). 50-State Property Tax Comparison Study for Taxes Paid in 2024. https://www.lincolninst.edu/publications/other/50-state-property-tax-comparison-study

[4] Tax Foundation. (2026). State Corporate Income Tax Rates and Brackets, 2026. https://taxfoundation.org/data/all/state/state-corporate-income-tax-rates-brackets/

[5] U.S. Energy Information Administration. (2024, July). How Much Tax Do We Pay on a Gallon of Gasoline and Diesel Fuel? https://www.eia.gov/tools/faqs/faq.php?id=10&t=10

[6] Tax Foundation. (2024). Does Your State Have a Gross Receipts Tax? https://taxfoundation.org/data/all/state/state-gross-receipts-taxes-2024/

[7] Internal Revenue Service. (n.d.). Publication 550: Investment Income and Expenses. https://www.irs.gov/publications/p550

[8] Ernst & Young LLP and Council on State Taxation. (2025, December). Total State and Local Business Taxes: State-by-State Estimates for FY24. https://www.cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/2511-10951-cs-50-state-report-final.pdf

[9] Enache, Cristina. (2025, May). Sources of US Tax Revenue by Tax Type, 2025. Tax Foundation. https://taxfoundation.org/data/all/federal/us-tax-revenue-by-tax-type/ (Original data from OECD (2025). Revenue Statistics 2025)

[1] U.S. Department of the Treasury. (2025). Government Revenue. Fiscal Data. https://fiscaldata.treasury.gov/americas-finance-guide/government-revenue/

[2] Tax Foundation. (2026). State and Local Sales Tax Rates, 2026. 7.53% is the population-weighted average combined sales tax rate. https://taxfoundation.org/data/all/state/sales-tax-rates/

[3] Lincoln Institute of Land Policy. (2025, June). 50-State Property Tax Comparison Study for Taxes Paid in 2024. https://www.lincolninst.edu/publications/other/50-state-property-tax-comparison-study

[4] U.S. Department of the Treasury. (2025). Government Revenue. Fiscal Data. https://fiscaldata.treasury.gov/americas-finance-guide/government-revenue/

[5] Ibid.

[6] Tax Foundation. (2026). State and Local Sales Tax Rates, 2026. https://taxfoundation.org/data/all/state/sales-tax-rates/

[7] Internal Revenue Service. (n.d.). Publication 550: Investment Income and Expenses. https://www.irs.gov/publications/p550

[8] U.S. Energy Information Administration. (2024, July). How Much Tax Do We Pay on a Gallon of Gasoline and Diesel Fuel? https://www.eia.gov/tools/faqs/faq.php?id=10&t=10

[9] Enache, Cristina. (2025, May). Sources of US Tax Revenue by Tax Type, 2025. Tax Foundation. https://taxfoundation.org/data/all/federal/us-tax-revenue-by-tax-type/ (Original data from OECD (2025). Revenue Statistics 2025)

[10] Enache, Cristina. (2025, May). Sources of US Tax Revenue by Tax Type, 2025. Tax Foundation. https://taxfoundation.org/data/all/federal/us-tax-revenue-by-tax-type/ (Original data from OECD (2025). Revenue Statistics 2025)