Wealth taxes – mind the economic distortions

Wealth taxes are back in vogue. From California to Europe, policymakers and pundits argue that taxing fortunes—rather than just income—would reduce inequality and raise revenue from those most able to pay. The political appeal is obvious. The economic consequences are less so.

Much of the public debate focuses on practical challenges: valuation disputes, tax enforcement, constitutional hurdles. But suppose, for the sake of argument, that all implementation problems could be solved. Suppose assets could be valued accurately and enforced perfectly. Even then, a deeper question remains:

Is taxing wealth economically superior to taxing income?

The answer, once we examine what a wealth tax actually does, is no.

Wealth tax: Taxing Tomorrow’s Profits Today

An income tax applies to realized income—wages, dividends, business profits. A firm earns profits; the government takes a share. The firm pays a dividend; the government takes another share. Crucially, the tax is levied when profits are realized and not when they are expected.

No serious income tax system attempts to tax a start-up on its projected future earnings at the moment it is founded. That would be absurd. Those profits are uncertain, risky, and years away—if they materialize at all.

But that is effectively what a wealth tax does.

The market value of a company is the present discounted value of its expected future profits. Taxing wealth means taxing not just what has been earned, but what investors believe might be earned in the future. It is a tax on expectations.

This distinction matters. It fundamentally changes incentives.

1. High Effective Tax Rates on Capital

A modest-sounding wealth tax can translate into strikingly high effective tax rates on income. Consider a 2% annual wealth tax. If an asset yields a 4% annual return, that 2% wealth tax amounts to a 50% tax on the annual return—before income taxes are even considered. If returns fall to 3%, the effective tax rate rises to 67%. In low-yield environments, it can exceed 100%.

Layering a wealth tax on top of corporate income taxes and dividend taxes would push the total tax burden on capital to levels that meaningfully alter behavior.

We know from decades of research that higher tax rates on capital discourage investment, entrepreneurship and business formation. Capital is mobile. Entrepreneurs are mobile. Ideas are mobile.

It is hard to imagine that a government introducing a wealth tax would simultaneously abolish income and capital gains taxes. The more realistic outcome is double—or even triple—taxation of returns. That has consequences: Higher taxes will mean fewer start-ups, lower capital formation, and ultimately fewer jobs.

2. Distortions Across Industries

Income taxes are neutral across industries in a straightforward sense: $10 million in profits is taxed the same whether earned by a steel manufacturer or a software company.

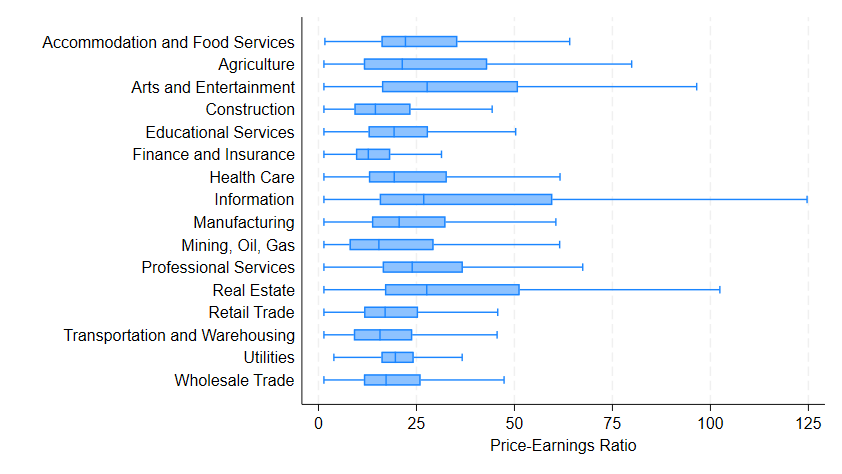

A wealth tax is different because it taxes valuation, not profits. And valuations vary dramatically across sectors. Technology firms, for example, often trade at high price-to-earnings (P/E) ratios because investors expect strong future growth. To illustrate this, the figure below plots the distribution of price-to-earnings ratios using the major industry classifications and price-to-earnings ratios of listed companies with profits over the period 2010-2025.

Utilities, financial companies, and construction firms typically trade at much lower multiples than, for example service companies, tech companies or entertainment firms, where price-earnings ratios reach or exceed a factor of 100. Something that is uncommon on many other industries.

Under a wealth tax, two entrepreneurs earning identical current profits would face very different tax bills if their industries command different market valuations. The owner of a high-growth tech company could owe several times more wealth tax than the owner of a mature industrial firm with the same annual profits.

This creates a powerful incentive for capital reallocation—not based on productivity or comparative advantage, but on tax minimization. Over time, such distortions skew investment toward low-valuation sectors and away from innovative, high-growth industries that typically drive productivity gains. Tax systems should aim for neutrality. A wealth tax does the opposite.

3. Volatility, Arbitrary Tax Burdens and Uncertainty

Market values fluctuate for reasons that may have little to do with a firm’s underlying operations. Changes in interest rates, shifts in global risk appetite, or macroeconomic news can move asset prices sharply even if expected cash flows of a single company are unchanged.

When the Federal Reserve lowers interest rates, discount rates fall and asset prices rise. Under a wealth tax, that mechanical valuation increase would immediately raise tax liabilities—without any change in actual profitability. This makes tax burdens volatile and partly arbitrary.

Economic research consistently shows that tax uncertainty dampens investment. When faced by unpredictable future tax payments, we see larger precautionary cash buffers and delayed investments. Capital that could finance innovation, expansion, and hiring sits idle instead. This slows long-term growth.

4. Perverse Risk Incentives

Wealth taxes are often described as progressive—you want to tax the rich or ultra-rich. However, in economic terms, wealth taxes are regressive and create perverse incentives.

Because the wealth tax is levied on the stock of assets rather than the flow of returns, the effective tax rate relative to income falls as returns rise. An entrepreneur earning a 10% return pays a far lower effective wealth tax rate on income than one earning 3%. Put differently, the most successful entrepreneur pays a lower effective tax than a less success one. This makes the wealth tax regressive.

This feature has important economic consequences because it encourages risk-taking—not necessarily the productive kind, but the kind aimed at boosting returns to offset the fixed annual wealth levy.

Individuals with lower risk tolerance or more conservative portfolios will bear a heavier effective wealth tax rate. A wealth tax punishes risk-averse investors. To maintain some level of after-tax returns, they will feel pressure to shift toward riskier assets. Managers, too, may be incentivized to pursue higher-return, higher-risk strategies to boost returns and cover recurring wealth tax liabilities.

Tax policy should not systematically push investors and managers away from their individually optimal risk profiles and investment decisions. A wealth tax does exactly that.

Growth Is Not an Afterthought

Proponents of wealth taxes argue that they target idle fortunes and enhance fairness. But wealth is not a vault of dormant gold. For the overwhelming majority of whoever will be called the wealthy under a wealth tax, assets consist of business equity—claims on factories, research labs, logistics networks and start-ups. Taxing wealth means taxing the capital stock of the economy.

Even if every valuation problem could be solved and every dollar is perfectly enforced, the economic logic remains: A wealth tax is a recurring tax on expected future profits. It raises effective tax rates on capital, distorts investment across industries, amplifies uncertainty and alters risk-taking behavior. These are not technical footnotes. They are central features.

Before embracing wealth taxes as an easy solution to fiscal and distributional challenges, policymakers should ask a more basic question: Which tax system raises revenues with the least economic distortions: a tax system that targets income when it is earned—or one that taxes tomorrow’s uncertain profits already today? The difference is not semantic. It is economic.