The double taxation of corporate profits

A familiar claim in tax debates is that wealthy Americans who live off dividends pay far less tax than “hard-working” wage earners (e.g., Washington Post, New York Times, or economists). The argument is often illustrated with a statement by Warren Buffett, who once remarked that his secretary pays twice the rate he is paying and that this is “outrageous”. Such statements have fueled the perception that capital income enjoys privileged treatment, and that dividend recipients face unusually low tax burdens.

Look only at the personal income tax, and this view appears plausible. Qualified dividends in the United States are taxed at a federal rate of up to 20 percent, plus a 3.8 percent net investment income tax — well below the top marginal rate on labor income of up to 37 percent. But this narrow comparison ignores a crucial feature of the US tax system: corporate profits are taxed twice.

All income paid out as dividends by C-corporations is first subject to the corporate income tax. Only what remains after this initial levy reaches shareholders, who then pay personal taxes on dividends received. Any meaningful discussion of fairness in dividend taxation must account for both layers.[1]

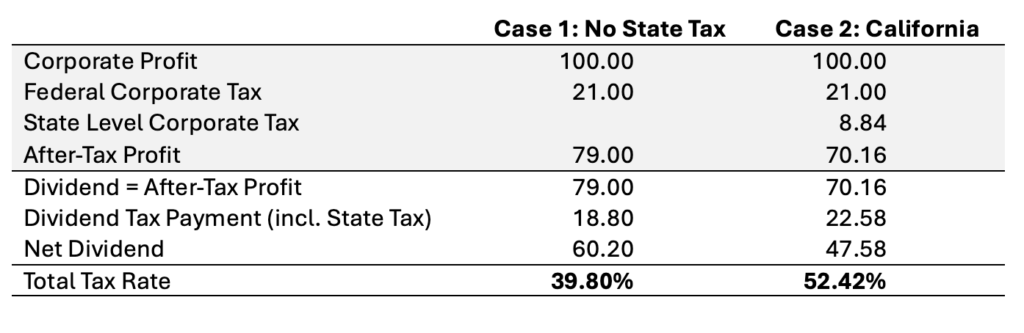

Consider the simple illustration shown in Table 1. Suppose a corporation earns a pre-tax profit of $100. Under current law, it pays a federal corporate tax of 21 percent. In a state with no corporate income tax — such as Texas — this leaves $79 available for distribution. When that amount is paid out as a dividend to a top-bracket taxpayer, it faces a combined federal dividend tax rate of 23.8 percent. The shareholder ultimately receives $60.20. In total, nearly 40 percent of the original corporate profit has been paid in taxes.

The burden is substantially higher in states with state-level taxes. In California, corporations face an additional state corporate tax of 8.84 percent, reducing after-tax profits to $70.16. Moreover, in California, dividends are subject not only to federal dividend taxes but also to California’s top personal income tax rate of 13.3 percent. Even after accounting for federal deductibility rules, the effective dividend tax rate rises to roughly 32 percent. The final after-tax dividend is just $47.58 — implying a combined tax rate exceeding 52 percent.

These figures, summarized in Table 1, put the popular narrative into perspective. In Texas, distributed corporate profits face a higher overall tax burden than the top federal marginal income tax rate on wages. In California, the combined burden far exceeds what most labor income ever faces. Dividend income, once corporate taxes are included, is not lightly taxed by any reasonable standard and can be over 50 percent in states like California.

Table 1: Combined Tax Burden of C-Corporation Income in the US

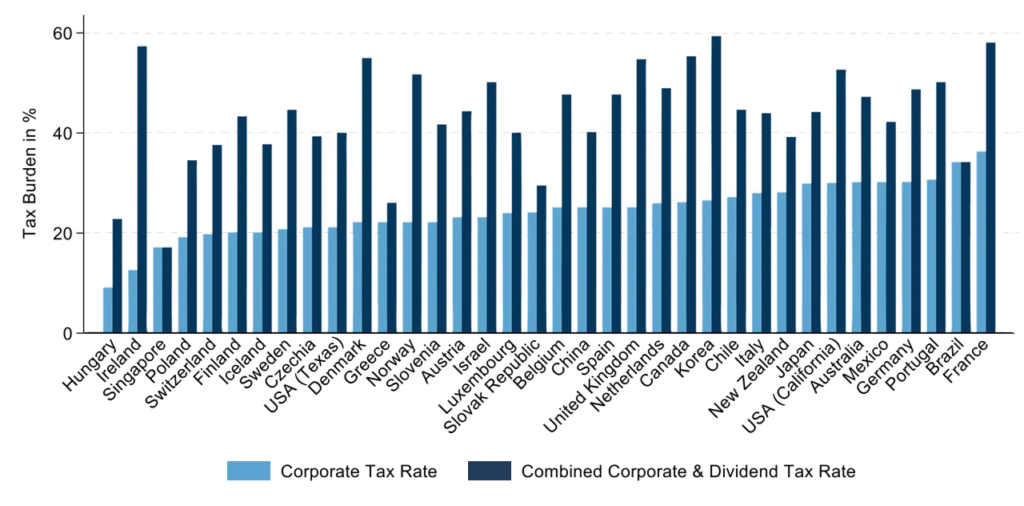

This pattern is not unique to the United States. International comparisons show that double taxation of corporate profits is the norm rather than the exception. While the US federal corporate tax rate is moderate by international standards, the combined corporate-plus-dividend tax rates in high-tax US states rank among the highest in the developed world. Countries such as France, Denmark, Ireland, Korea, and the UK all impose combined rates above 50 percent. Only a handful of jurisdictions—including Singapore and Brazil—fully exempt dividends from personal taxation. The overall message is however clear: Once there are state-level taxes, the combined tax burden in the US is far from small and is comparable to the tax burden in most other countries.

Figure 1: Comparison of Combined Corporate & Dividend Tax Rates Around the World

Proposals to raise dividend tax rates or to introduce wealth taxes to tackle this issue often rest on the assumption that capital income systematically escapes taxation. The arithmetic in Table 1 and Figure 1 tells a different story. Increasing dividend taxes would push combined effective tax rates on distributed profits even more above those faced by labor income, especially in states with high corporate and personal taxes. Whether this is desirable is a policy question — but it should be debated using accurate measures of tax burdens, not partial ones.

It is also worth noting that avoiding double taxation is not easy. Distributing earnings through share repurchases does not eliminate tax liability: capital gains are taxed at the same statutory tax rates as dividends, and unrealized gains are increasingly in policymakers’ sights (and then, one must account for the fact that retaining earnings comes with a host of other problems). In practice, corporate profits are taxed sooner or later.

The broader lesson is this: Focusing exclusively on shareholder-level taxes creates a distorted picture of how much taxes someone pays. Corporate taxes ultimately fall on people—shareholders, workers, and consumers—and dividend taxation is best understood as the second layer of that burden. Ignoring the first layer may be politically convenient, but it leads to misleading conclusions.

If the goal is a fair and efficient tax system, the debate must move beyond slogans and single-rate comparisons. Dividend income may appear lightly taxed at first glance, but once the full chain of taxation is considered, it clearly is not.

[1] S-Corporations pay personal income tax plus state taxes on profits.