Tax Transparency Changes Where Firms Invest: Implications for Global and Local Tax Policies

Essay for the Tax Policy Network based on the insights from De Simone and Olbert (2022).

Tax Transparency as a Panacea?

Policymakers around the world have embraced tax transparency as a tool to curb corporate tax avoidance. The logic and policy objective are intuitive: if tax authorities can see where multinational firms earn profits, employ workers, and hold assets, they can better detect profit shifting. More information should mean less tax avoidance, either through a deterrence effect of stricter enforcement in tax audits.

But transparency can change economics more broadly. When governments change what they monitor, firms change how they operate. And sometimes, those changes occur in places policymakers may not expect.

A striking example comes from Country-by-Country Reporting (CbCR), introduced in the European Union in 2016 as part of the OECD’s Base Erosion and Profit Shifting (BEPS) initiative. Under CbCR, large multinationals with more than €750 million in revenue must privately disclose to tax authorities detailed country-level information: revenues, profits, employees, tangible assets, and taxes paid. Crucially, this information is shared among tax authorities across jurisdictions.

In our research, we examined how firms responded to this new transparency regime. The findings illustrate an important, and somewhat counterintuitive, surprising consequence.

Firms Don’t Just Move Profits. They Move Activity.

We find clear evidence that, when faced with greater scrutiny of profit allocations, firms respond not merely by adjusting accounting choices but by reallocating real economic activity—moving assets and employees so that reported profits appear better aligned with underlying operations.

After the introduction of private CbCR, multinationals above the reporting threshold increased tangible investment and labor expenditures in European jurisdictions with preferential tax regimes, including Ireland, Luxembourg, the Netherlands, Malta, Cyprus, and Switzerland.

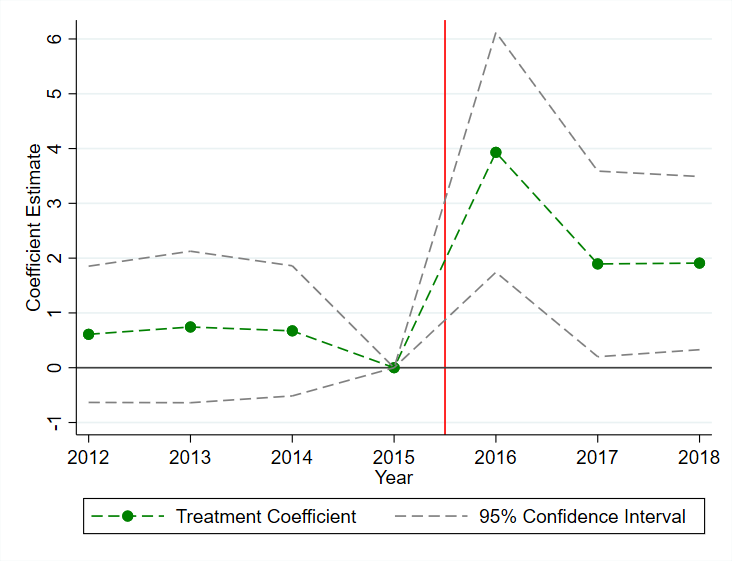

Panels A and B of Figure 1 present the estimated effects. Relative to slightly smaller firms not subject to CbCR, treated firms increased subsidiarylevel capital investment in these jurisdictions by about 2 percentage points of assets and labor expenditures by roughly 5 percentage points. These effects are economically meaningful: for the average subsidiary, they imply double-digit millions of euros in additional tangible assets and several million euros in additional payroll.

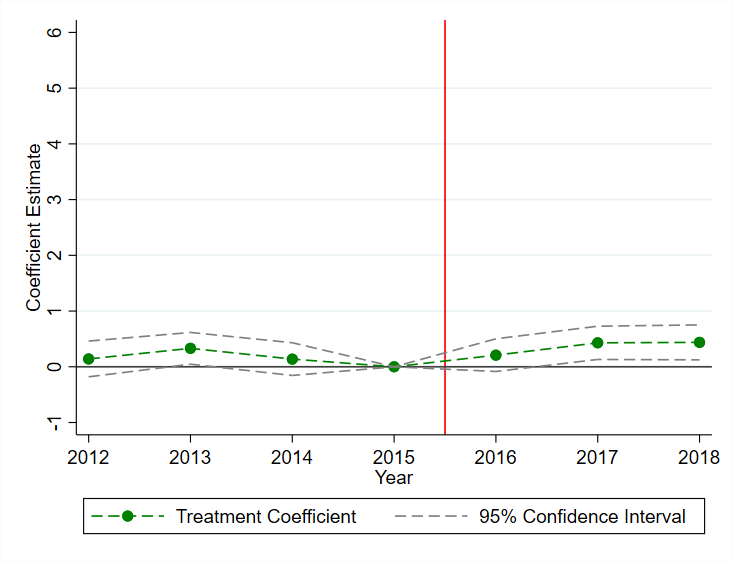

Importantly, we do not find comparable increases in other European countries. Nor do we observe an increase in total consolidated investment at the firm level. The evidence instead suggests reallocation: firms appear to shift capital and labor within Europe toward jurisdictions offering preferential tax treatment.

In other words, when transparency increased enforcement risk around profit-location decisions, firms increased real substance where profits were already tax-advantaged. The—perhaps surprising—winners of CbCR are Ireland, the Netherlands, and Luxembourg, while high-tax industrial countries such as Germany and France benefit little, if at all.

This reallocation has broader implications. Ideally, capital and labor should flow to their most productive uses. Yet after CbCR, capital investment became less sensitive to underlying investment opportunities, suggesting that tax considerations exert greater influence on real decisions. As a result, tax competition may intensify in favor of preferential-regime countries, while investment becomes more tax-distorted—and less economically efficient—than before.

Effects on Tax Avoidance

At the same time, we find that firms reduced organizational complexity after CbCR. Specifically, they decreased the number of subsidiaries in preferential tax regimes and in tax havens more broadly, particularly at lower tiers of the corporate hierarchy.

This suggests a second response margin: firms simplified their structures to reduce the appearance of aggressive tax planning. Increased visibility to tax authorities appears to have made overly complex corporate structures less attractive.

In light of concurrent findings in the literature showing that overall tax aggressiveness declined following CbCR Joshi (2020); Hugger (2024), the transparency mandate may indeed have achieved part of its intended goal—limiting tax avoidance. However, our evidence indicates that the associated costs in the form of distorted and reallocated investment may be substantial, potentially outweighing the modest reduction in tax avoidance among a subset of large multinationals.

What Does This Mean for Policy?

None of this implies that transparency is misguided. On the contrary, improved information can strengthen enforcement and promote fairness. But the evidence highlights an important lesson: anti-avoidance regulation is not a free lunch.

Our findings have direct implications for tax policy in an increasingly competitive global economy.

Most directly, our findings speak to transparency initiatives in Europe which are currently moving even further. Country-by-Country Reporting (CbCR), which has so far been private and available only to tax authorities, will now be made public across the EU due to a 2021 EU regulation, with the first public reports released in 2025 in early adopter countries and the rest coming in 2026.

In light of our evidence, it is unclear whether making CbCR public will meaningfully strengthen tax enforcement. Instead, it may introduce additional and potentially distortionary incentives. Public disclosure exposes firms not only to tax authorities but also to stakeholders, activists, and competitors. The proprietary costs may be substantial. Competitors will gain detailed insight into where firms invest, how much capital they deploy, and how profitable those operations are. Such information can deter investment, reduce risk-taking, and dampen innovation.

The broader takeaway is not that transparency or other anti-tax avoidance rules should be abandoned, but that their design matters. Effective tax transparency requires coordination across countries and complementary policies that anchor real investment. Above all, policymakers must account for behavioral responses. This is precisely where rigorous, evidence-based research can play a crucial role in informing sound policy design.

Figure 1: Investment Effects and Descriptive Insights from Private CbCR in Europe

(A) Investment Effects of CbCR in European Countries with Preferential Tax Regimes

(B) Investment Effects of CbCR in Other European Countries

Notes: These graphs plot the difference-in-differences coefficients and their 95 percent confidence intervals from regressions of subsidiary-level Capital Investment on indicators for each year in the sample period interacted with a treatment indicator taking on the value of 1 for treated CbCR firms (firms reporting more than 750 million in 2016 revenue). Graph is based on the subsample of European countries with preferential tax regimes (Cyprus, Ireland, Luxembourg, Malta, The Netherlands, Switzerland), and graph (2) is based on the subsample of all other European countries. These results are taken from De Simone et al. (2022). Figure 2 Panels (3) and (4), with further definitions and details on the estimation provided in the paper.

Bibliography

De Simone, L., Klassen, K. J., and Seidman, J. K. (2022). The effect of income- shifting aggressiveness on corporate investment. Journal of Accounting and Economics, page 101491.

De Simone, L. and Olbert, M. (2022). Real effects of private country-by- country disclosure. The Accounting Review, 97(6):201–232.

Gschossmann, E. and Olbert, M. (2025). Taxes and the global spillovers of ai investments. Available at SSRN 5196844.

Hugger, F. (2024). Regulatory avoidance responses to private country-by- country reporting. International Tax and Public Finance.

Joshi, P. (2020). Does private country-by-country reporting deter tax avoid- ance and income shifting? Evidence from BEPS Action Item 13. Journal of Accounting Research, 58:333–381.