S Corps and How They Are Taxed

Overview

Business activities can be organized in several ways that carry important tax and non-tax tradeoffs. One popular form that start-up businesses elect is the Subchapter S corporation, commonly referred to as an “S corporation” or “S corp.” Under Subchapter S of the U.S. Internal Revenue Code, the S corporation’s income, losses, deductions, and tax credits are reported on their shareholders’ individual tax returns. Importantly, the income of S corporations is not taxed at the business entity level. Rather, all income “flows through” to the individual owners and are reported on their personal tax returns. As a result, S corporation business income is subject to personal, not corporate, tax rates.

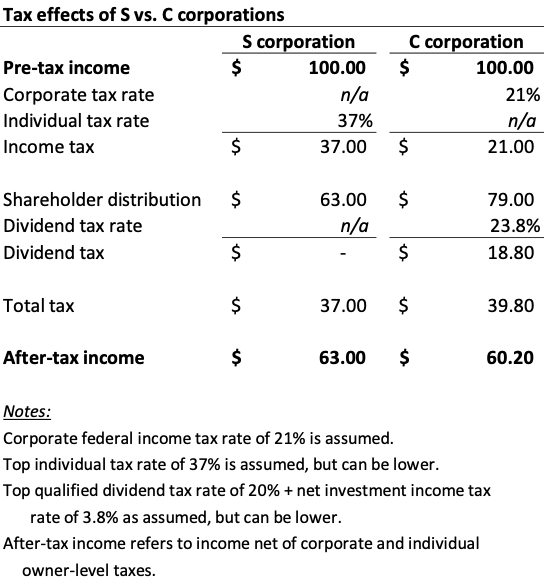

This flow through feature differs from another type of corporation, the C corporation, or “C corp.” In contrast to S corporations, C corporations are subject to “double taxation.” This means that income earned by C corporations is subject to tax both at the business entity level and again at the individual level to the extent dividends are paid to its shareholders. The example below illustrates the different tax burden for an S corporation vs. C corporation with $100 of pre-tax income. The S corporation owner retains $63.20 after-tax, versus $60.00 for the C corporation shareholder.

From a non-tax perspective, however, S corporations retain the same liability protections and formal corporate structure as C corporations, since corporations are recognized legally as a separate entity from its shareholders.

S corporations account for the majority of U.S. corporate entities

Although most of us think of Apple, Amazon, or Ford when we hear the word “corporation,” most businesses are in fact not organized in this manner. Although economically important, C corporations represent only 23.5% of U.S. corporate tax returns, or 1.6 million entities as of 2022 using the most recent IRS data. In contrast, S corporations, along with other less commonly used flow-through corporations known as real estate investment trusts (REITs) and regulated investment companies (RICs), account for almost 76.5% of all corporate tax returns, or 5.2 million entities. Therefore, S corporations reflect widespread adoption by many small and mid-size firms.

For a start-up considering organizing as an S corporation, several tax and non-tax tradeoffs are especially important.

Taxed regardless of cash distributions: First, as noted above, S corporation profits and losses flow through to shareholders, who report them on their individual tax returns. However, business owners should be aware that their share of the S corporation’s income is taxed regardless of whether the S corporation distributes that income in cash. Therefore, shareholders need to monitor cash distributions to ensure adequate liquidity to cover the personal tax related to the owner’s share of the S corporation income. If the business is a start-up that incurs early losses, shareholders may see that those losses can pass through to their personal returns, potentially lowering their total income tax liability. However, obstacles may arise. For example, S corporation losses can be limited by the shareholder’s basis (i.e., investment in the business), at-risk rules, and passive activity loss rules, and thus not currently deductible on the individual’s tax return. Therefore, start-ups without active income or adequate capital may be unable to fully utilize the tax benefits of early losses.

Shareholder eligibility rules limit capital raising: The second tradeoff revolves around eligibility restrictions. S corporations can only be domestic, have no more than 100 shareholders, and only one class of stock. Therefore, it becomes challenging to attract additional capital. In effect, S corporations cannot go public, and institutional venture capital typically prefers entities that can issue multiple classes of stock and have a broader range of eligible investors. As a result, start-ups seeking outside equity investment may find S corporations less flexible than C corporations or other forms of organization.

Salary and compensation rules: A third consideration relates to shareholders who manage the S corporation. Shareholders who work in the business must receive a “reasonable” salary, which is subject to payroll or self-employment taxes (i.e., for Social Security and Medicare). The IRS closely scrutinizes the reasonableness of a shareholder-manager’s compensation because any distributions received by the shareholder-manager above the salary level would in fact not be subject to payroll or self-employment taxes. Therefore, S corporation status can be abused by setting salary unreasonably low so that more of the cash received could be classified as a “distribution” (i.e. not subject to payroll taxes) rather than “salary” (subject to payroll taxes).

State and local tax treatment: A final consideration relates to non-federal taxation. While U.S. tax law provides for flow-through treatment of S corporations, states and municipalities can differ in their treatment. Some do not recognize S status (e.g., New Hampshire, Tennessee, New York City, and the District of Columbia), others double-tax S corporations and/or apply a franchise tax (e.g., Michigan, California, New York, and New Jersey), while others tax a limited amount or type of income (e.g., Massachusetts, Indiana, Kentucky, Maine, and Wisconsin). Thus, state and local tax burdens may differ from federal treatment.

Academic accounting research shows that the tax and non-tax differences between S and C corporations matter to owners, customers, and employees. For example, in research focusing on the banking sector, researchers have found that C corporation banks that compete against more S corporation banks are more likely to convert to S status in the future, likely due to the competitive pressure applied by these tax-advantaged S banks. In particular, by converting from C status, the new S banks offer higher interest rates to depositors and increase advertising to attract more customers. Other research finds that S corporation banks generally pay more in wages and dividends than C banks. The results suggest that different structures alter after-tax rates of return, allowing businesses to compete more effectively.

Overall, S corporations occupy a central area in the U.S. business landscape. While S corporations can deliver tax advantages that can affect the competitiveness of a business, they also come with various restrictions that start-ups should consider carefully.

Sources

https://www.irs.gov/pub/irs-pdf/p5655.pdf

https://www.irs.gov/businesses/small-businesses-self-employed/s-corporations

https://www.scorporationsexplained.com/how-do-states-treat-s-corporations.htm

https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12464

https://www.journals.uchicago.edu/doi/10.17310/ntj.2015.4.04