Latest

All Analysis & Commentary

| Title | Author | Topic | Publish Date | Excerpt |

|---|---|---|---|---|

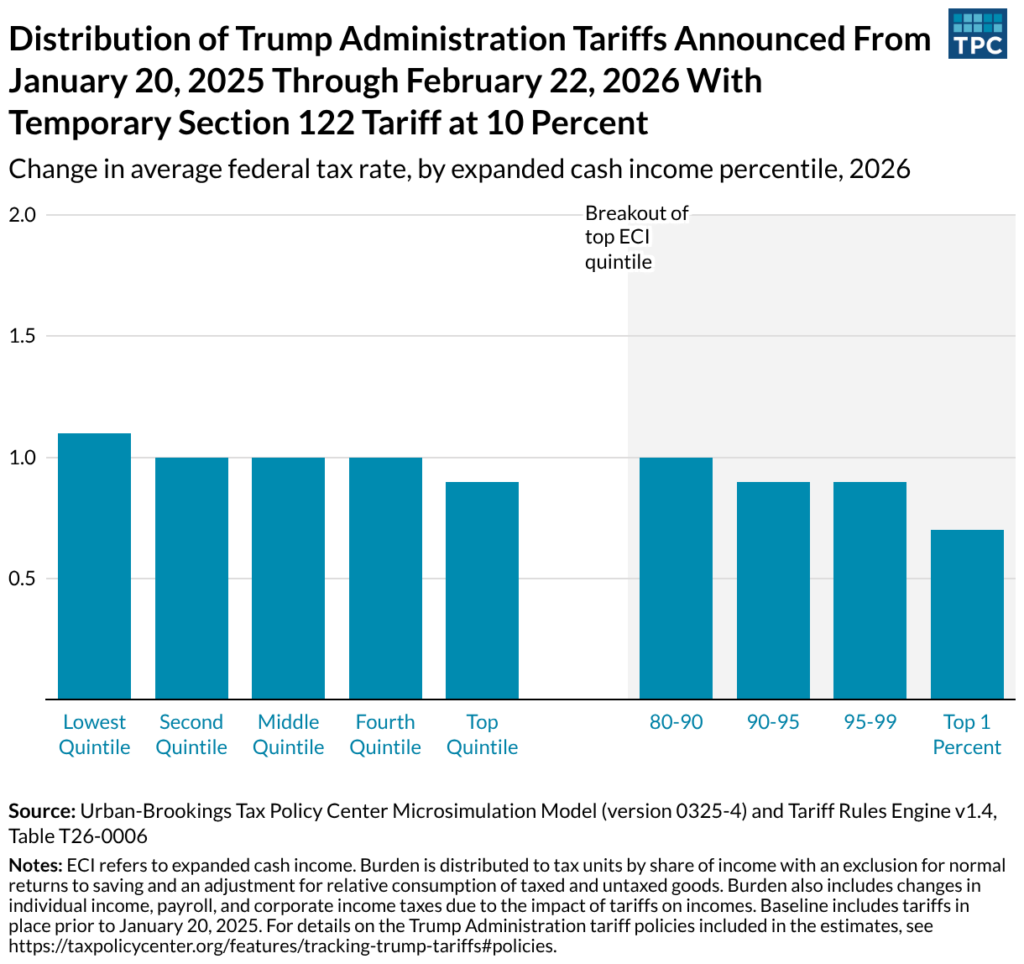

| Can Tariffs Replace the Individual Income Tax? | Bridget Stomberg | Uncategorized | 2026-03-31 | A proposal to replace the modern individual income tax system with tariffs raises fundamental concerns. The economic burden of tariffs falls disproportionately on lower-income households, and tariffs do not raise sufficient or stable revenues that can serve as a plausible substitute for the individual income tax. |

| Exempting the Working Class: Simplicity versus Cyclicality | Frank Murphy | Other | 2026-03-20 | |

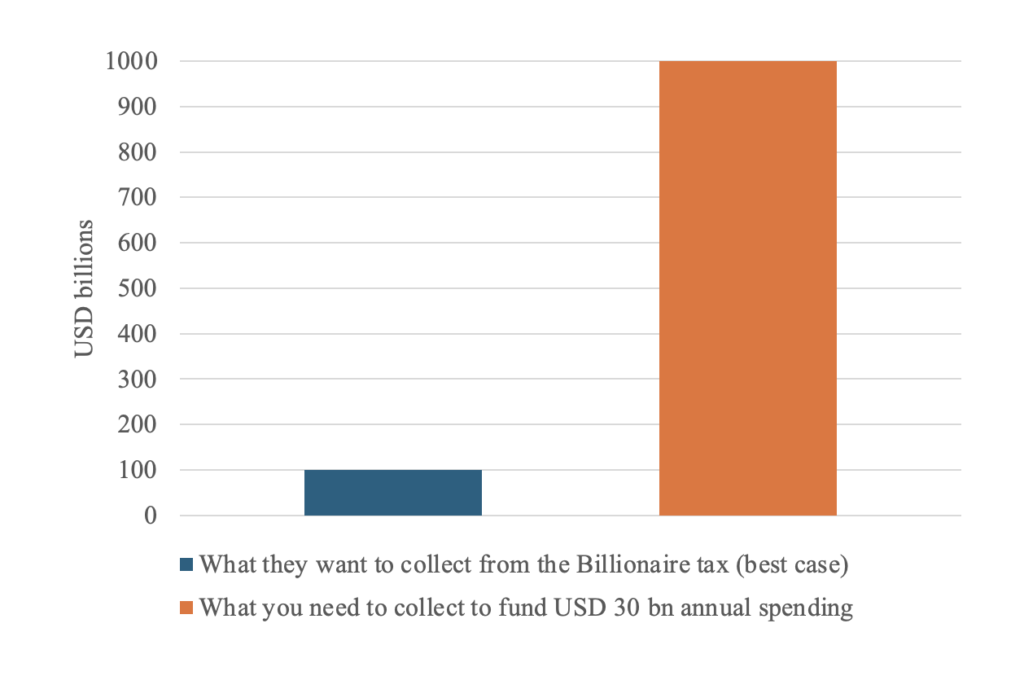

| The One Time Billionaire Tax: A One-Time Fix for a Permanent Problem? | Martin Jacob | Wealth Tax Issues | 2026-03-20 | California’s latest proposal to levy a one-time tax on billionaires has ignited the predictable controversial debate. Before taking sides in this debate, it is worth asking a more basic question: even if the tax works as advertised and raises $100 billion, would it solve the problem it is meant to address? |

| March Madness Has a New Entry Card: State Taxes | Martin Jacob | Other | 2026-03-20 | Like everyone else, athletes pay federal income taxes. But the key difference lies at the state level. Some states—such as Florida or Texas—have no state income tax, while others, like California, tax top incomes at rates above 13 percent. In new research, we study how this tax difference affects the success of college basketball programs. We analyze all Division I men’s basketball teams from 2016 to 2024 and compare their performance before and after NIL rules began. |

| Please Stop Trying to Tax Book Numbers, Even if Produced by Billionaires | Jeff Hoopes | Wealth Tax Issues | 2026-03-19 | There is a proposal to tax the wealth of billionaires in California. At first glance, it seems simple enough: take the net worth of the wealthy, multiply it by the tax rate (in this case 5 percent), and send a tax bill. But this simplicity masks a fundamental question. What exactly is that net worth? What number, precisely, is being taxed? |

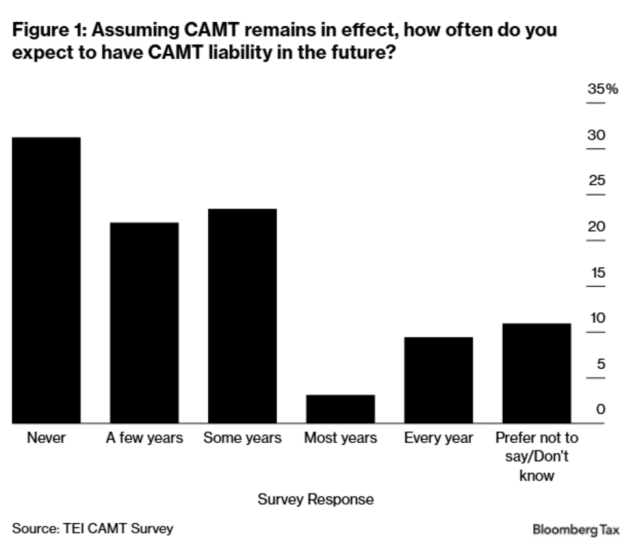

| How Complex Is the New Corporate Alternative Minimum Tax? | Andrew Belnap, Jeff Hoopes | Corporate Tax Burdens | 2026-03-19 | The corporate alternative minimum tax, enacted in 2022 as part of the Inflation Reduction Act, imposes a 15% minimum tax on “adjusted financial statement income” for certain large corporations and has multiple shortcomings. CAMT is conceptually flawed, involves very high compliance costs, does not meaningfully change corporations’ incentives, and raises little revenue. |

| The New CAMT Does Not Meaningfully Alter Corporate Tax Outcomes | Andrew Belnap, Jeff Hoopes | Corporate Tax Burdens | 2026-03-19 | Our analysis examines CAMT’s impact on corporate tax planning and estimated tax revenue, demonstrating that despite imposing substantial new compliance and planning costs, CAMT appears to have done little to change who pays corporate income tax or how much they pay. |

| Galle v Rauh: Comparing Two Revenue Estimates for California Billionaire Taxation | Jeff Hoopes | Other | 2026-03-18 | California is considering a one-time tax on the wealth of billionaires. Two recent reports attempt to estimate the fiscal effects of the proposal. |

| Indexing Capital Gains: Good Economics, but an Administrative Nightmare | Douglas Shackelford | Other | 2026-03-18 | A large body of empirical research demonstrates that taxing capital gains upon realization discourages investors from selling appreciated assets, thereby reducing capital mobility and potentially slowing economic growth. However, acknowledging the reality of lock-in does not mean indexing capital gains is a practical solution. The administrative and structural complications associated with indexing are substantial enough to outweigh its theoretical appeal. |

| Why should we care about partnership businesses? | Ryan Hess | Understanding Business Taxation | 2026-03-13 | Partnerships have become the dominant business structure in the U.S., outnumbering C corporations by more than 2-to-1 and representing over $50 trillion in assets. As flow-through entities with significant flexibility in allocating gains and losses among partners, partnerships play a central role in real estate, private equity, and professional services—yet they also contribute substantially to the tax gap and face historically low audit rates. This analysis examines partnership taxation, structural complexity, and enforcement challenges. |

| S Corps and How They Are Taxed | Pete Lisowsky | Understanding Business Taxation | 2026-03-13 | S corporations account for the majority of U.S. corporate entities, with 5.2 million filing returns compared to 1.6 million C corporations. Unlike C corporations, S corporations are flow-through entities where income passes to shareholders' individual tax returns, avoiding double taxation. This analysis examines how S corporations are taxed, the eligibility restrictions they face, compensation rules for shareholder-managers, and the tax and non-tax tradeoffs that affect competitiveness and organizational choice. |

| Why Do We Tax Businesses, and What Types of Taxes Are There? | Rebecca Lester, T. M. Jensen Ahokovi | Understanding Business Taxation | 2026-03-12 | Businesses face far more than just income taxes. From sales tax on supplies to payroll taxes on wages, property taxes on facilities, and dividend taxes on distributions, taxes touch nearly every stage of business operations. This analysis examines why governments tax businesses, walks through the full spectrum of business tax obligations using a simplified example, and compares the U.S. tax structure to other developed economies. |

| Corporate Income – only a part of US Business Income | Rebecca Lester, Tina Li | Understanding Business Taxation | 2026-03-12 | Corporate income taxes account for just 8.3% of federal revenue, but this figure tells an incomplete story. Most U.S. businesses operate as flow-through entities—sole proprietorships, partnerships, and S corporations—where income is taxed on individual returns rather than at the entity level. This analysis examines how business income is defined, measured, and taxed across different entity structures, and why understanding these distinctions is essential for evaluating tax policy debates. |

| Can Wealth Taxes Substantially Tax Power Away from Billionaires? | Jeff Hoopes | Wealth Tax Issues | 2026-03-03 | Recent wealth tax proposals cite billionaire political influence as a key concern, arguing that reducing concentrated wealth would diminish political power. But would wealth taxes actually achieve this goal? This analysis examines whether the amounts required to influence elections and policy are large enough that wealth taxation would meaningfully constrain political spending by the very wealthy—and finds that political influence may be far cheaper than advocates assume. |

| Please Don’t Make Our Tax System Any More Fair | Jeff Hoopes | The Tax Fairness Debate | 2026-02-27 | "Fairness" is invoked across the political spectrum in tax debates, yet the word means fundamentally different things to different advocates—from keeping what you earn to redistributing resources. This analysis argues that the vagueness of "fairness" as a policy objective obscures real tradeoffs and leads to symbolic legislation designed to satisfy feelings rather than solve clearly defined problems. Examples include the Corporate Alternative Minimum Tax and stock buyback excise tax. |

| Wealth taxes – mind the economic distortions | Martin Jacob | Wealth Tax Issues | 2026-02-27 | Wealth taxes have gained political momentum as a tool to address inequality and raise revenue. But setting aside practical implementation challenges, how do wealth taxes compare to income taxes in purely economic terms? This analysis examines a fundamental distinction: income taxes apply to realized profits, while wealth taxes effectively tax expected future earnings. The implications for investment incentives, industry distortions, risk-taking, and economic growth may be significant. |

| Is a 4% wealth tax the same as a 120% income tax? | Jeff Hoopes | Wealth Tax Issues | 2026-02-27 | Wealth tax proposals often sound modest when expressed as a percentage of assets—but how do they compare to income taxes in economic terms? By examining the relationship between wealth and the income it generates, this analysis demonstrates how to convert wealth tax rates into their income tax equivalents. The results reveal that seemingly small wealth taxes can translate into surprisingly high effective tax rates on income, depending on rates of return. |

| Tax Transparency Changes Where Firms Invest: Implications for Global and Local Tax Policies | Marcel Olbert | The Profit Shifting Debate | 2026-02-20 | Country-by-Country Reporting was designed to help tax authorities detect profit shifting by requiring multinationals to disclose detailed financial information across jurisdictions. But new research reveals an unexpected consequence: firms responded not just by changing accounting practices, but by reallocating real economic activity—moving tangible assets and employees to low-tax jurisdictions. This analysis examines how transparency regulations can reshape where companies invest and what that means for tax policy. |

| The double taxation of corporate profits | Martin Jacob | Understanding Business Taxation | 2026-02-14 | Are dividend recipients lightly taxed? A common claim suggests wealthy investors pay lower tax rates than wage earners. But this comparison typically overlooks a key feature of the tax system: corporate profits are taxed twice—first at the corporate level, then again when distributed as dividends. This analysis examines the combined tax burden and compares it across countries. |

| Has Aggregate U.S. Outbound Income Shifting Decreased in Recent Years? | Robert Hills | The Profit Shifting Debate | 2026-02-13 | Has U.S. outbound income shifting—where corporations transfer income from the U.S. to foreign tax havens—decreased following the Tax Cuts and Jobs Act of 2017? Using data from both the Bureau of Economic Analysis and firm-level sources, this analysis tracks the share of U.S. corporate profits recognized in tax haven jurisdictions over nearly three decades to assess recent trends. |

| Multinational Profit Shifting: A Primer to the Academic Debate | Nadine Riedel | The Profit Shifting Debate | 2026-02-13 | Multinational enterprises can shift profits across borders to reduce tax burdens, but quantifying this practice and designing effective policy responses remain challenging. Drawing on academic research, this analysis examines the evidence for profit shifting, the mechanisms firms use, variation across companies and countries, and the evolving international policy landscape aimed at curbing these practices. |

| Enforcement: The Engine of Tax Compliance | Erin Towery | Understanding Business Taxation | 2026-02-13 | The IRS audits only a small fraction of tax returns, yet enforcement plays a critical role in revenue collection. With an annual tax gap exceeding $600 billion, research shows that enforcement affects not just direct collections, but also voluntary compliance through deterrence. This analysis examines how enforcement capacity shapes taxpayer behavior and government revenue. |

| Why do we tax corporations? | Scott Dyreng | Corporate Tax Burdens | 2026-02-13 | Why do we tax corporations? Common answers focus on corporate wealth, infrastructure use, and market power. But these explanations may not capture the full picture. This article examines both the weak and strong justifications for corporate taxation, exploring what corporate taxes actually accomplish in the broader tax system. |

| How Much Do Companies Around the World Actually Pay in Corporate Taxes? | Martin Jacob | Corporate Tax Burdens | 2026-02-13 | Do large companies actually pay corporate taxes? Using data from over 18,000 firms across 27 countries, this analysis examines effective tax rates—what companies actually pay relative to their profits. The findings reveal a more complex picture than political rhetoric suggests, with significant variation across countries and important exceptions to common assumptions. |

| The Corporate Tax Avoidance Crackdown Already Happened | Martin Jacob | The Profit Shifting Debate | 2026-02-11 | Corporate tax avoidance remains a central concern in public debate, with claims that multinational companies exploit loopholes to reduce their tax burdens. But much of the evidence cited comes from decades-old data. This analysis examines how international tax rules have fundamentally changed over the past ten years, and asks whether policy discussions have kept pace with regulatory reforms already in place. |

| When More Tax Transparency May Make Things Worse | Martin Jacob | The Tax Fairness Debate | 2026-02-10 | Policymakers worldwide are requiring companies to publicly disclose tax information, with the goal of helping investors and consumers identify aggressive tax avoidance. But does public tax transparency actually work as intended? Recent experimental research examines whether ordinary users of information can meaningfully interpret corporate tax disclosures—and the findings challenge common assumptions about disclosure's effectiveness. |