Multinational Profit Shifting: A Primer to the Academic Debate

A substantive share of economic activity is organized within multinational enterprises (MNEs), posing an inherent mismatch with corporate taxation that is designed and administered at the national level. This puts the spotlight on international tax rules, which specify how tax base is allocated across jurisdictions in which an MNE operates.

Under the current framework, this allocation relies on pricing intra-firm transactions at arm’s length, meaning that MNEs’ internal transfer prices mirror those set by unrelated parties. In recent decades, policymakers and civil society have become increasingly concerned that MNEs may exploit the flexibility inherent in these rules to shift pre-tax profits from high-tax to low-tax jurisdictions in order to reduce their effective tax costs—a practice commonly referred to as multinational profit shifting.

How Much Profit Is Shifted?

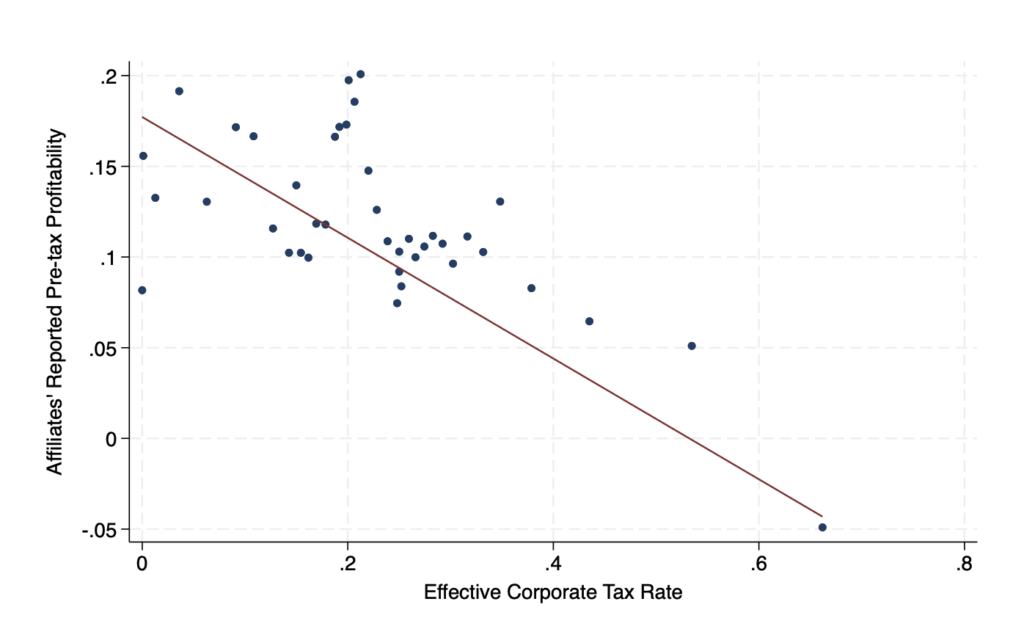

The academic literature provides overwhelming evidence consistent with profit shifting behavior. Both firm-level and macro data show that profits reported by affiliates in low-tax jurisdictions are disproportionately large relative to the real economic activity undertaken there, exceeding profitability levels observed at high-tax locations by a factor 10 or more. Moreover, reported pre-tax profitability has been shown to respond sensitively to tax incentives: consensus estimates suggest that a 10 percentage-point higher corporate tax rate is associated with roughly an 8% reduction in reported affiliate profits. The binned scatter plot in Figure 1 illustrates this relationship (drawing on unconsolidated accounting data for MNEs in the EU plus Norway, the United Kingdom, Switzerland, and Iceland during the period 2008–2019). Recent studies further document that high-tax affiliates report profits at or close to zero more frequently than comparable domestic firms, again consistent with income relocation across jurisdictions.

While this body of evidence strongly supports the existence of profit shifting, its aggregate magnitude remains debated. Quantifying profit shifting is inherently challenging: it requires detailed data on multinational operations and crucially hinges on the modeling of a credible counterfactual of how profits would be allocated across MNE affiliates in the absence of tax-motivated behavior. Such counterfactuals must account for the fact that higher profitability in low-tax locations may reflect real differences in capital intensity, productivity, or business models rather than tax planning alone. Researchers adopt different data and strategies to address these challenges, all relying on assumptions — translating in a relatively broad range of estimates: recent prominent studies, for example, place shifted profits at around 12% versus roughly 36% of high-tax firms’ pre-tax incomes.

How Is Profit Shifted?

The literature has identified several key channels through which MNEs shift profits across jurisdictions.

Transfer pricing and intra-group service charges. Around half of global trade occurs within multinational networks. This offers opportunities to relocate profits across affiliates by mispricing intra-group transactions. While intra-firm transfer prices are legally required to follow the arm’s length principle, comparable third-party transactions are often difficult to find in practice, particularly when goods and services are firm-specific, bundled, or tied to proprietary technologies – thus offering some leeway for strategic price distortions. Consistent with this notion, studies based on granular firm-level trade data show that MNEs adjust intra-firm trade prices in ways consistent with profit shifting, especially in more differentiated product categories.

Intellectual property location and royalty flows. Patents, trademarks, algorithms, and other intangible assets play a central role in modern value creation. Their legal ownership can be separated from the location of real activity, allowing firms to place them in low-tax jurisdictions and use intra-group royalties or licensing fees to shift taxable income away from high-tax affiliates. Empirical literature drawing on administrative data on patent applications confirms this type of strategic holding of (foreign-developed) intellectual property at low-tax locations within multinational groups.

Internal debt and interest deductions. Multinational groups can further relocate income by financing high-tax affiliates with intra-group loans from low-tax entities. The schemes exploit that interest payments are tax-deductible in high-tax countries and can through internal lending be stripped from heavy taxation. Empirical studies confirm the relevance of intra-firm debt-shifting, documenting significant increases in intra-firm lending when corporate tax rates at high-tax locations rise.

All three shifting channels are quantitatively relevant. Broadly speaking, non-financial means of income shifting—transfer pricing, royalties, and related internal charges—appear to dominate debt-based shifting. Meta-analytic evidence indicates that the former mechanisms account for roughly three-quarters of total shifting activity.

Is Profit Shifting Heterogeneous Across Firms?

Profit shifting is widespread across industries, locations, and firm-size classes, but important heterogeneity exists. First, large MNEs account for the majority of global shifting activity. Evidence for Germany, for example, suggests that about 95% of shifted income relates to MNEs with consolidated revenues above €750 million. While larger firms mechanically shift more income in absolute terms, their shifting also appears to be larger in relative terms, likely reflecting fixed costs associated with setting up sophisticated tax planning structures.

Second, shifting correlates with firms’ business models – it is, for example, more prevalent in intangible-intensive industries. Organizational features also matter: better-managed firms tend to shift more, while countervailing incentives can dampen profit shifting—for example, when tax-strategic mispricing of imports raises firms’ import tariff liabilities. Third, there is regional variation. U.S.-headquartered MNEs, for structural and historic reasons, on average, engage in more shifting than their European counterparts. And developing countries appear to be particularly exposed to tax avoidance, reflecting their weaker administrative and enforcement capacity.

Evidence also suggests that profit shifting has increased over time. Historically, business income was tightly anchored to geographically immobile production factors such as physical capital and labor. Intra-firm trade was limited and focused on standardized goods for which arm’s length prices were readily observable. As a result, opportunities for systematic income relocation were limited. This has changed markedly. Mobile assets such as intellectual property now play a central role in the value creation of many MNEs, operations across affiliates are highly integrated, and intra-firm trade has expanded significantly, often involving firm-specific goods and services—with all of these developments arguably raising the scope for strategic profit allocation.

Why Does Profit Shifting Matter?

Profit shifting has several important economic and policy consequences.

Most prominently, it reduces corporate tax revenue collected in high-tax countries, forcing governments to shift the tax burden to other bases, cut spending, or tolerate higher deficits.

Profit shifting may also distort competition. Large multinationals with access to sophisticated tax planning can achieve systematically lower effective tax rates than smaller domestic firms, potentially creating an uneven playing field.

There are also distributional concerns. Profit shifting comes with benefits – which accrue to firm shareholders and, according to recent evidence, partly to leading workers in the firm. As shareholders and top workers are located at the upper end of the income distribution, profit shifting can reduce the progressivity of national tax systems.

Profit shifting might also undermine the legitimacy and the trust in the tax system. Visible cases where highly profitable firms pay little tax where they operate can undermine taxpayer confidence in the tax system. Finally, observers have raised concerns that profit shifting can foster international corporate tax competition: If profits flee the country when corporate taxes are high, governments may feel pressured to lower statutory corporate tax rates or introduce special tax regimes, which target the mobile shifting profit. The latter development was visible in the early 2000s when a number of countries began granting special low-tax rates on income from mobile intellectual property – so-called IP box regimes.

What to do about?

Over recent decades, countries have increasingly introduced and strengthened rules aimed at curbing profit shifting, first unilaterally and more recently through coordinated multilateral efforts. Key instruments include:

- Transfer pricing rules and documentation requirements, which regulate that firms must set their internal trade prices at arm’s length and are required to contemporaneously document their price choices.

- Deduction limits which constrain the deductibility of debt costs and license payments from the income tax base if these costs are deemed excessive.

- Controlled-foreign company rules which make passive foreign income at low-tax locations taxable in firms’ parent countries.

Empirical evidence points to some effectiveness of all of these rules in putting relevant constraints on the targeted shifting channels. But open questions remain. Importantly, it is still unclear whether and to what extent firms—and their advisors—actually find new ways to avoid taxes in a cat-and-mouse dynamic.

More recently, international coordination has intensified through the OECD/G20 Base Erosion and Profit Shifting (BEPS) project and the global minimum tax (Pillar Two), both joined by more than 140 countries.

BEPS streamlined and tightened existing anti-profit shifting rules and introduced a number of new measures, among others stricter rules against harmful tax practices. Prime target of the latter regulations are IP box regimes: New nexus rules require IP boxes to link preferential tax treatment of IP income to local R&D activity. Early evidence suggests that these reforms reduced the relocation of foreign-developed patents to low-tax jurisdictions and increased domestic innovation activity in IP box countries.

BEPS further introduced Country-by-Country Reporting (CbCR), requiring large multinationals to disclose detailed information on profits and real activity across jurisdictions. Early evidence suggests that these rules led to some closures of low-tax affiliates and modest increases in MNEs’ effective tax costs. At the same time, firms appear to have responded by maintaining income at low-tax locations but backing it up by real activity. The latter effect is a broad theme across many BEPS measures, reflecting the intervention’s intent to curb profit shifting but not real activity location at low-tax entities.

The global minimum tax, designed to ensure that large MNEs face a minimum effective tax rate of 15% on their global income, represents the most recent multilateral reform and has been implemented in many countries, particularly within the European Union following the 2022 directive. Evidence on its effects is still emerging. Simulations point to some reductions in profit shifting and moderate revenue gains – which by design of the regulations largely accrue to low-tax countries.

Roads ahead

Despite substantial progress, important challenges remain. The complexity of overlapping anti-avoidance rules has increased firms’ compliance costs, especially in the transfer pricing domain and under the global minimum tax. Survey evidence suggests that these burdens are sizable, though non-survey evidence remains limited.

There is also evidence for inefficiencies in tax enforcement, rooting in the challenge to cleanly identify arm’s length prices for intra-firm trade. Tax authorities have incentives to tilt MNEs’ price choices in their favor – in both, high-tax and low-tax trade alike. Consistent with this notion, evidence for Denmark suggests that transfer pricing audits fail to be well-targeted at low-tax country trade.

More fundamentally, it remains unclear how the tightening of anti-profit shifting rules will affect international tax competition. While limiting profit shifting could reduce incentives for countries to lower tax rates to attract the mobile shifting profit, it may also encourage governments to more strongly compete for real investments instead. Consistent with this notion, evidence shows that the location and size of real investments become more tax sensitive when firms have less options to lower their effective tax costs through international tax avoidance.

Similarly ambiguous predictions on corporate tax setting emerge for the global minimum tax. While standard theory suggests that minimum taxes dampen international tax competition and raise corporate tax rates relative to the counterfactual, inverse effects may also emerge: High-tax countries might more aggressively lower their tax rate when countries at the minimum tax threshold cannot retaliate by lowering their rate in return. Evidence from the introduction of a minimum tax in the context of the German local business tax suggest that the latter effect dominates.

Finally, deeper structural challenges persist. Allocating profits across group affiliates based on arm’s length pricing of intra-firm trade is inherently flawed as national firms and multinationals structurally differ, rendering national firms’ pricing a distorted benchmark for MNEs’ true underlying price choices. The application of the arm’s length principle also remains challenging in a world where a sizable part of intra-firm trade is firm-specific, and ambiguities in transfer pricing induce uncertainty and disputes between authorities, as reflected by large numbers of mutual agreement procedure cases.

Alternative systems, such as formula apportionment and destination-based corporate taxation, have been proposed both in academia and in policy debates. Under formula apportionment, a multinational’s consolidated profits are allocated across jurisdictions using a formula based on observable factors such as sales, employment, and/or capital. Destination-based cash-flow taxation allocates taxing rights primarily to market countries, i.e., where final consumption occurs. These approaches are conceptually appealing because they can substantially weaken firms’ incentives to locate reported profits in low-tax jurisdictions and they reduce the central role of the arm’s length principle in allocating taxable income. However, they would not eliminate tax planning altogether: incentives would shift toward manipulating the location of sales or other apportionment factors, and transfer-pricing issues may remain relevant for non-income taxes (e.g., customs duties) or in systems that are not fully harmonized. Tying taxing rights more strongly to destination, however, can have efficiency-enhancing effects in the sense that consumer markets are relatively less mobile than profits or production, although firms may still respond through prices, product mix, or market participation. Implementing such far-reaching reforms—which redistribute tax base across countries and create winners and losers—would require substantial international coordination and cross-country compensation schemes that are difficult to achieve in an increasingly fragmented geopolitical environment.

In the meantime, a pragmatic path forward may lie in refining the current international tax system: simplifying overlapping anti-profit shifting rules, introducing safe harbors in the application of the global minimum tax, and systematically evaluating the effects of recent anti-profit shifting reforms and screen for remaining loopholes.