Has Aggregate U.S. Outbound Income Shifting Decreased in Recent Years?

U.S. outbound income shifting, where U.S. corporations transfer income from the U.S. to foreign jurisdictions, has faced intensifying scrutiny from lawmakers, academics, and the media over the last 25 years. One reason for this is the concern that outbound shifting reduces U.S. tax revenue collections. Consequently, a stated goal of the Tax Cuts and Jobs Act of 2017 (or TCJA) was to combat and reduce U.S. outbound income shifting, thereby protecting U.S. tax revenue.

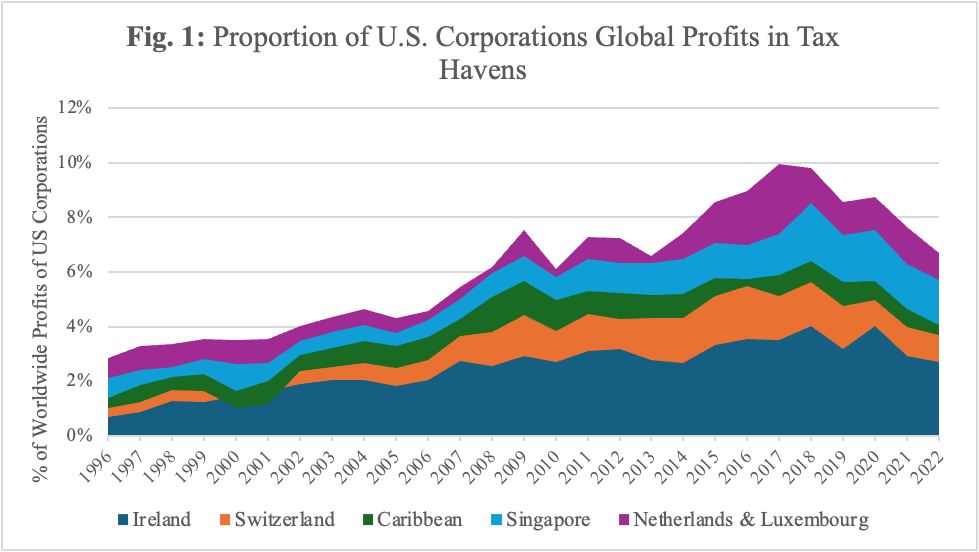

One way to examine how policy changes like the TCJA influence outbound income shifting is to track the share of U.S. corporate profits recognized in tax havens, which are destinations for shifting. For example, Garcia-Bernardo et al. (2022) suggest that the TCJA had minimal impact on this trend because, using data from the Bureau of Economic Analysis (BEA), they show that through 2020 the proportion of U.S. corporations’ global profits recognized in tax haven jurisdictions like Ireland, Singapore, Switzerland, Netherlands/Luxembourg, and the Caribbean remained at historic highs.

Figure 1 reproduces Garcia-Bernardo et al.’s (2022) analysis using the latest BEA survey data for 1996-2022. The figure reveals that the share of U.S. corporations’ global profits booked in tax havens peaked at nearly 10% in 2017 but has declined for most years since. By 2022, this proportion was at approximately 6.7%—a more than 30% decrease from the 2017 peak. If the proportion of U.S. corporations’ global profits booked in tax havens serves as an effective proxy for U.S. outbound income shifting, the evidence in Figure 1 suggests that shifting has, in fact, decreased in recent years.

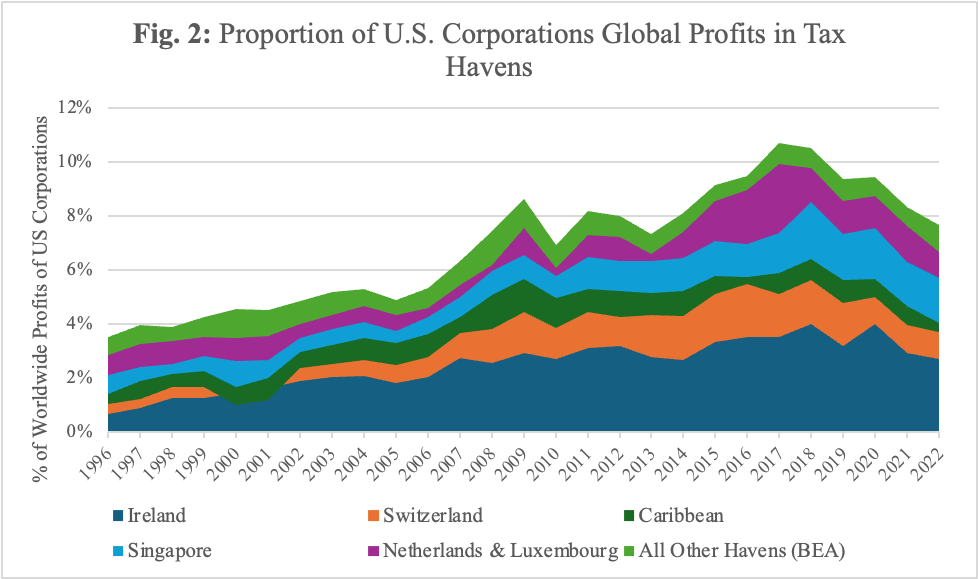

While Figure 1 follows Garcia-Bernardo et al. (2022) by focusing on five specific tax haven jurisdictions, Figure 2 expands the scope to include all tax havens with available BEA data. Data associated with these additional haven jurisdictions (Costa Rica, Barbados, Hong Kong, Netherlands, Antilles, and Malaysia) are combined into a new jurisdictional category called “Other Tax Havens (BEA)”. This group accounts for less than 1% of U.S. corporations’ global profits in most years, suggesting their inclusion does not significantly alter the primary findings. Notably, Figure 2 confirms the proportion of U.S. corporations’ profits booked in tax havens has trended downward since peaking in 2017.

Do alternative data sources yield similar inferences?

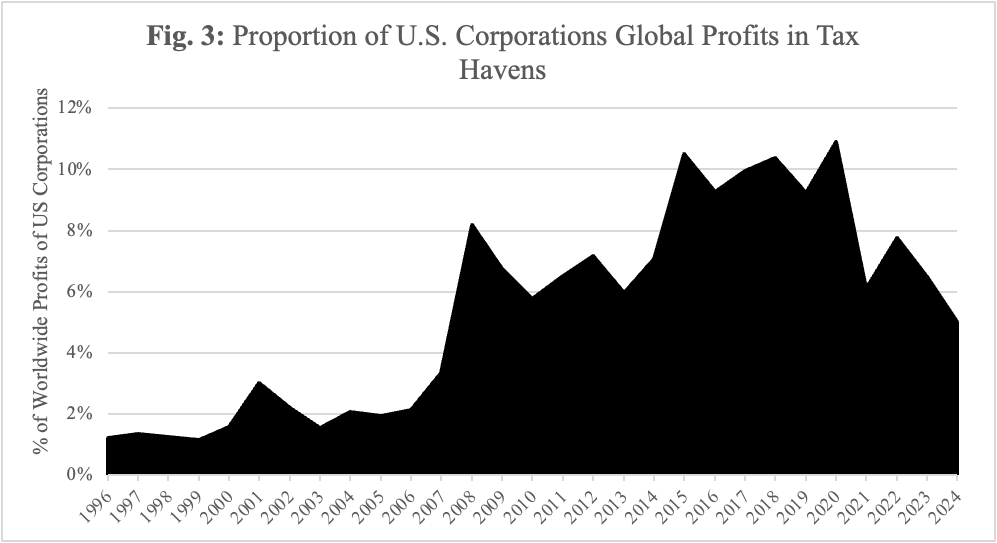

Research highlights that differences in U.S. outbound income shifting estimates often stem from differences in data sources, such as macroeconomic data (for example, those provided by the BEA) versus microeconomic, or firm-level, data. Thus to triangulate the findings in Figure 1 and 2, Figure 3 reports the proportion of U.S. corporations’ global profits recognized in tax havens when using an approach from Dyreng et al. (2022) which relies on firm-year data. One caveat to this approach is that while it yields firm-year estimates for profits booked in tax havens, it lacks jurisdictional granularity regarding where those profits are recognized.

Figure 3 reveals several key findings:

- Discrepancy with BEA data: For 1996-2007 the proportion was generally below 3%, which is notably lower than the levels observed in the BEA data for the same period.

- Post-TCJA Peak: The proportion was at its highest between 2015-2020, peaking at 10.8% in 2020. This suggests U.S. outbound shifting may have remained elevated for at least a few years after the TCJA.

- Recent Decline: Since 2020, the proportion has dropped sharply to a low of approximately 5% in 2024, representing a more than 50% decrease from its 2020 peak. This decline is consistent with Figures 1 and 2, suggesting U.S. outbound income shifting has decreased in recent years.

Collectively, evidence from both BEA and firm-level datasets reveals a marked decline in the proportion of U.S. corporations’ global profits booked in tax havens. This consistent trend suggests U.S. outbound income shifting has decreased in recent years, particularly after the TCJA.

References

Dyreng, S., R. Hills, and K. Markle. 2022. Tax deficits and the income shifting of US multinationals. Available at SSRN.

Garcia-Bernardo, J., P. Janský, and G. Zucman. 2022. Did the Tax Cuts and Jobs Act Reduce Profit Shifting by US Multinational Companies? National Bureau of Economic Research.