Galle v Rauh: Comparing Two Revenue Estimates for California Billionaire Taxation

Abstract

California is considering a one-time tax on the wealth of billionaires. Two recent reports attempt to estimate the fiscal effects of the proposal. One, by Galle, Gamage, Saez, and Shanske (2026), provides the primary estimate cited by supporters of the policy. Another, by Rauh, Jaros, Kearney, Doran, and Cosso (2026), offers a much lower estimate and a broader analysis of fiscal consequences. Galle et al. estimate the tax will produce 2.5 times more revenue than Rauh et al., and Rauh et al. find that the total fiscal impact of the law may be negative. This note compares the methodology used in the two reports. Galle et al. rely on a simple static calculation based on Forbes estimates of billionaire wealth and assume that 10 percent of the tax base will be avoided. Rauh et al., in contrast, construct the tax base on a person-by-person basis, adjust the Forbes list for residency, incorporate evidence of migration from the literature, consider a wider range of behavioral responses drawn from the wealth-tax literature, and examine the fiscal consequences of lost income-tax revenue if high-wealth individuals leave the state. These methodological differences explain why the two reports arrive at dramatically different conclusions.

I would like to thank David Gamage for encouraging me to read both of these analyses carefully and compare the two, and Scott Dyreng and Martin Jacob for comments on an initial draft.

Introduction

California is currently considering a ballot initiative that would impose a one-time tax of 5 percent on the net worth of individuals with wealth exceeding $1 billion. The proposal has generated considerable commentary. Much of that discussion focuses on how much revenue would such a tax actually generate.

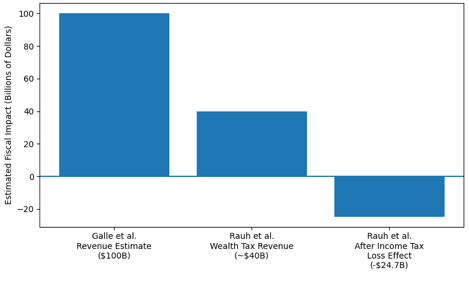

Two recent reports provide very different answers. One report, authored by Brian Galle, David Gamage, Emmanuel Saez, and Darien Shanske (2026), estimates that the tax would raise approximately $100 billion. A second report by Joshua Rauh, Benjamin Jaros, Gregory Kearney, John Doran, and Matheus Cosso (2026) estimates that the policy would raise roughly $40 billion and could even reduce overall state revenues after accounting for the possibility that billionaires who flee California no longer pay California income taxes.

Figure 1. Estimated Fiscal Effects of the California Billionaire Tax

These two estimates differ by tens of billions of dollars. The difference arises from the analytical approach each report takes to estimating the tax base and behavioral responses. This note compares the two methodologies. The two reports represent very different approaches to policy evaluation: one static and simplistic, the other dynamic and detailed (Galle et al., 2026; Rauh et al., 2026).

To lay my cards on the table, I believe that the world is complicated, and that when possible, empirical analysis should be done in as detailed a way as possible, and be informed by existing academic literature. That literature consistently shows that people respond to tax incentives, and as a consequence, are very likely to respond behaviorally to a wealth tax.

The Galle et al. Approach

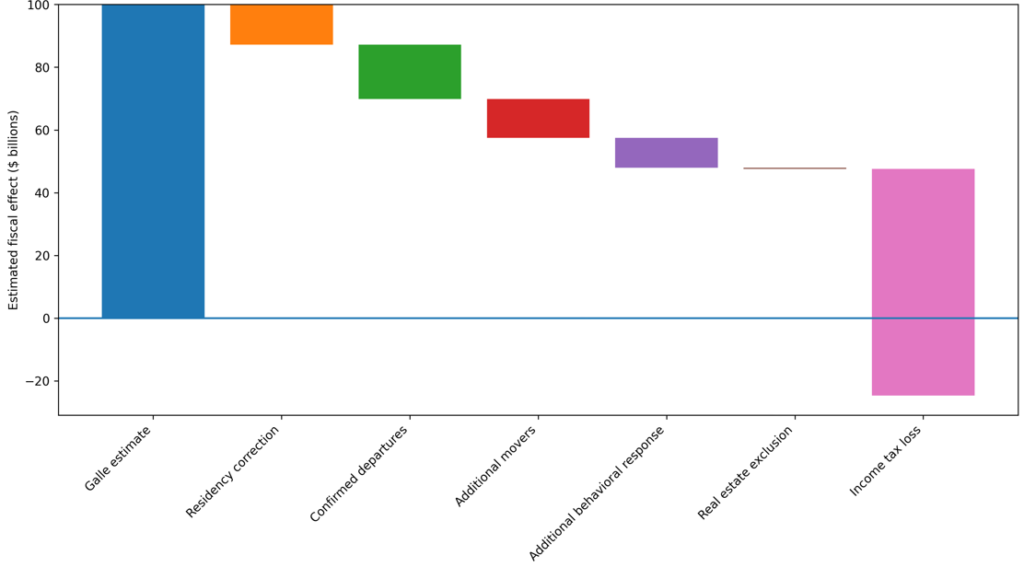

The analysis in Galle et al. begins with a simple calculation based on the Forbes real-time billionaire list. According to Forbes, there are approximately 213 billionaires residing in California with total wealth of about $2.18 trillion as of early 2026. The proposed tax rate is 5 percent. Applying the tax rate to this wealth base yields a gross revenue estimate of approximately $109 billion.

The authors then assume that 10 percent of the tax base will be lost to avoidance or evasion. After applying this adjustment, the estimated revenue falls to roughly $99 billion, which they round to $100 billion for simplicity.

That is the end of their revenue estimate.[1]

In short, the Galle et al. analysis offers a simple static estimate of the revenue potential of the tax, adjusted modestly for avoidance behavior. All behavioral effects are either assumed to be trivial, or rolled up in the “10% of tax avoidance” parameter.

The Rauh et al. Approach

The analysis by Rauh et al. takes a very different approach. Rather than relying on the aggregate Forbes wealth total, the authors attempt to reconstruct the tax base on a person-by-person basis.

Their starting point is also the Forbes billionaire list. However, they do not assume that every individual identified by Forbes as residing in California would necessarily be subject to the tax. Instead, they examine the residency status of individuals on the list and remove those who appear to have already relocated to other states prior to the relevant date.

The authors also add individuals who they believe should have been included but were omitted from the Forbes classification of California residents. After making these adjustments, they arrive at a revised estimate of the wealth held by California billionaires.

Rauh et al. then make several additional adjustments to the tax base.

First, they take the exclusion of directly held residential real estate seriously. The proposed tax explicitly exempts real estate property directly held by taxpayers. To account for this provision, the authors estimate residential real estate holdings for individual billionaires using property records, public reporting, and real estate valuation sources such as Zillow and Redfin. Where direct information is unavailable, they impute residential real estate using observed median ratios of real estate wealth to net worth.

This adjustment reduces the estimated taxable base by approximately $8 billion among the billionaires who remain in the California tax base after residency adjustments.

Second, the authors incorporate evidence of migration. They identify several individuals who have publicly announced relocations away from California and treat those individuals as having exited the tax base prior to the tax’s implementation. The departure of even a small number of extremely wealthy individuals can substantially reduce the aggregate tax base because billionaire wealth is highly concentrated. For example, flight from California by Larry Page alone represents more than 10% of the tax base.

Third, the authors attempt to incorporate behavioral responses drawn from the broader wealth-tax literature. In particular, they use estimates from studies of wealth taxation in Europe, especially Switzerland, to calibrate plausible responses in the form of relocation, tax planning, and avoidance.

The authors estimate a tax base approximately $40 billion, less than half of the $100 billion figure proposed by Galle et al.

Importantly, the Rauh et al. analysis emphasizes that this estimate is uncertain and depends heavily on assumptions about behavioral responses. The authors provide several scenarios based on different levels of migration and avoidance, as one would expect from a serious estimate from economists.

Behavioral Responses and the Wealth-Tax Literature

The largest difference between the two reports concerns the assumed magnitude of behavioral responses.

Galle et al. assume that avoidance and evasion, as well as every other possible response, will reduce the tax base by 10 percent. The report does not provide justification for this figure, and it appears to function as a simple adjustment intended to account for some level of planning or valuation disputes.

Rauh et al., in contrast, assume substantially larger behavioral responses. Their estimates draw on empirical research examining how taxpayers respond to wealth taxes in other countries. In particular, they cite evidence suggesting that wealth taxation can lead to relocation, tax planning, tax evasion, and other behavioral responses that reduce the effective tax base.

Galle et al. apply a 10% adjustment factor because they expect behavioral responses to be small, citing Galle, Gamage, and Shanske (2025) in support. That assumption reflects the lowest end of what evidence from other wealth taxes might justify. I think it is reasonable to assume larger behavioral responses in California. California’s institutional setting may make avoidance easier than in many of the European cases studied in the literature. To escape a California wealth tax, a taxpayer would only need to move to another U.S. state. By contrast, avoiding a national wealth tax in Europe usually requires moving to another country. The California proposal also sets a tax rate that is far higher than the rates historically used in most European wealth taxes, while applying to a much smaller group of taxpayers. That means the departure of even one taxpayer could significantly reduce the tax base. In addition, the people subject to the California tax are likely to be especially mobile. European wealth taxes often reached taxpayers at wealth levels that could include high-earning professionals, such as law or economics professors. The California proposal, by contrast, targets only the ultra-wealthy. Those households may be much more willing to take major steps to avoid tax liabilities that could reach billions of dollars, rather than the much smaller liabilities, often measured in thousands of euros, associated with European wealth taxes. Because the barriers to relocation are likely lower in California, it is plausible that mobility responses there could be at least as large as, and possibly larger than, those observed in international settings.

Of course, these responses are necessarily assumptions. The exact magnitude cannot be known in advance—both author groups are predicting the future. Both reports ultimately rely on judgments about behavioral responses, but they adopt very different assumptions.

There is, of course, a literature on wealth taxation in other countries. So, what does the literature actually say? Scheuer and Slemrod (2021), summarize a few key papers, and all point to reductions in the tax base in excess of 10%:

“How effective such expanded enforcement would be in restraining evasion has been controversial. Saez and Zucman (2019) claim that evasion would shrink the wealth tax base by just 15 percent. Kopczuk (2019) expresses skepticism, noting that the most effective tax enforcement relies on market transactions reported by third parties, which would be absent for much wealth.

Alstadsæter, Johannesen, and Zucman (2019) link the account names from the HSBC leak with individual tax data for Norway, Sweden, and Denmark and find that 95 percent of these foreign account-holders did not report the existence of the account to the tax agency. They show that evasion rates rise sharply across the income distribution and conclude that the top 0.01 percent in the income distribution evade about 25 percent of the income and wealth taxes they owe. Guyton et al. (2020) combine random audit data with data on offshore bank accounts and show that tax evasion for US taxpayers through offshore financial institutions is highly concentrated at the very top of the income distribution, and that random audits virtually never detect this form of evasion.”

The Treatment of Income Tax Revenues

Another major difference between the two analyses concerns the treatment of California income tax revenues. Rauh et al. note that if billionaires relocate to avoid the wealth tax, they will stop paying California income taxes. The authors attempt to estimate the income tax contributions of California billionaires and calculate the present value of those future revenues. They then compare the one-time wealth-tax revenue with the potential long-run loss of income tax collections.

Applying reasonable assumptions about discount rates, mobility effects, etc., they conclude that the net present value of the wealth tax could be negative. The long-run loss of income tax revenue might exceed the one-time wealth tax collected.

Galle et al. discuss the effect of lost income taxes, but do not net this effect against their wealth tax estimate. Rather, they just suggest very few income taxes are paid and assume that the effect will be, in essence, zero, because billionaires are so lightly taxed, and because they will display very low mobility rates.

Figure 2. Sequential Adjustments From Galle Estimate To Rauh Net Fiscal Effect

Other Issues

There are many other issues to consider when considering a wealth tax. Regardless of the amount raised in revenue, the cost of collecting and administering a tax which will have serious valuation issues, the scope of avoidance and evasion responses, the stability of the base, the constitutionality, the signal to capital, the effects on job creation, investment, innovation, etc., should all be considered. This report focuses entirely on two estimates of revenue and ignores all these other issues.

Conclusion

The Galle et al. analysis provides a straightforward static estimate based on aggregate wealth data and a modest behavioral adjustment. The Rauh et al. report constructs the tax base more carefully, incorporates assumptions about mobility and avoidance drawn from the literature, and considers the broader fiscal implications of taxpayer relocation.

These methodological differences explain why one report estimates revenue of roughly $100 billion while the other estimates closer to $40 billion—2.5 times more revenue from Galle et al. than from Rauh et al. Ultimately, the true outcome would depend on how taxpayers respond to the policy if it is enacted.

References

Alstadsæter, Annette, Niels Johannesen, and Gabriel Zucman. 2019. “Tax Evasion and Inequality.”American Economic Review 109 (6): 2073–2103.

Galle, B. D., Gamage, D., Saez, E., and Shanske, D. (2026). Expert Report on the California 2026 Billionaire Tax: Revenue, Economic, and Constitutional Analysis.

Galle, B., Gamage, D., & Shanske, D. (2025). Money moves: Taxing the wealthy at the state level. California Law Review.

Guyton, John, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman. 2020. “Tax Evasion by the Wealthy: Measurement and Implications.” In Measuring and Understanding the Distribution and Intra/Inter-Generational Mobility of Income and Wealth, edited by Raj Chetty, John Friedman, Janet Gornick, Barry Johnson, and Arthur Kennickell.

Kopczuk, Wojciech. 2019. “Comment on ‘Progressive Wealth Taxation’ by Saez and Zucman.” Brookings Papers on Economic Activity 2019: 512–26.

Rauh, J. D., Jaros, B., Kearney, G., Doran, J., and Cosso, M. (2026). The Net Present Value of the Billionaire Tax Act: An Assessment of the Fiscal Effects of California’s Proposed Wealth Tax.

Saez, Emmanuel, and Gabriel Zucman. 2019a. “Progressive Wealth Taxation.” Brookings Papers on Economic Activity 2019: 437–511.

Scheuer, Florian, and Joel Slemrod. 2021. Taxing Our Wealth. Journal of Economic Perspectives 35 (1): 207–30.

[1] The entirety of their analysis reads, “The Forbes billionaire list has 213 California billionaires with a collective wealth of $2.182 trillion (which is 26.6% of the US wide $8.189 trillion owned by all 938 US billionaires). A 5% tax on $2.18 trillion raises $109 billion. Factoring in 10% of tax avoidance and evasion leads to a scoring of $99 billion that we round to $100 billion for simplicity.”