Exempting the Working Class: Simplicity versus Cyclicality

Who pays federal income taxes in America? Under Senator Cory Booker’s (D-NJ) recently proposed Keep Your Pay Act, the answer could be millions fewer individuals than today. Married couples earning less than $75,000 would see substantial tax relief, with some receiving net payments from the government (i.e., a negative effective income tax rate) due to refundable credits.

The proposal expands three common tax breaks: the standard deduction, the Earned Income Tax Credit (EITC), and the Child Tax Credit. The natural follow-up question is how will this policy be financed? Booker proposes increasing taxes on high-income individuals and corporations—framed as requiring them to “pay their fair share.” This raises a broader issue: as the income tax base becomes more concentrated, does tax revenue become less stable? As anyone who has leaned back on two legs of a chair instead of four knows, stability depends on a broad base. The more weight you place on fewer points, the easier it is to tip—much like relying on a narrower group of taxpayers (i.e., tax base) to fund federal revenue.

On its face, the distributional effects are straightforward. Lower- and middle-income households—especially families with children—would benefit the most. Because most lower-income taxpayers already take the standard deduction, increasing it would further reduce their tax liabilities. Expanding the refundable portions of the Child Tax Credit and EITC would push many filers to a zero or negative effective tax rate.

At the same time, tax compliance would likely become simpler. Fewer taxpayers would itemize deductions, reducing the need for extensive recordkeeping. No more shoebox of receipts at tax time.

The Bigger Picture: Where Revenue Comes From

One often overlooked point is the relative size of federal revenue sources (see Lester and Ahokovi 2026 for an overview). According to Congressional Budget Office (CBO) projections, individual income taxes account for the largest share of federal revenue—on the order of trillions annually—while corporate income taxes are a much smaller share, in the hundreds of billions.

This distinction matters. While political rhetoric often focuses on large corporations, much of U.S. business activity occurs through pass-through entities (such as S-corporations and partnerships), whose income is taxed under the individual income tax system rather than the corporate tax (Hess 2026). As a result, increasing “corporate” taxes does not necessarily capture the true share of total business income.

The Tax Foundation reports that in 2022, the bottom 50% of the income distribution paid a relatively small share of total federal income taxes (about $63 billion out of more than $2.1 trillion) and faced low average effective tax rates (around 3%). Many in this group already receive tax credits that reduce or eliminate their income tax liabilities. This suggests that further increasing this group’s standard deduction would have little budgetary impact; however, expanding refundable credits could significantly increase future budget deficits.

At the other end of the income spectrum, the top 10% of earners pay over 70% of all federal income taxes. Much of this is concentrated among the top 1%, who on average pay over $500,000 in taxes and collectively contribute more than 40% of total income taxes.

Debates about fairness often hinge on how one interprets these distributions. Some argue that tax burdens should be proportionate to income; others support more progressive tax systems, where higher earners pay a larger share. Tax Foundation data from 2022 suggest that households in the 5th–10th income percentile pay roughly in proportion to their income—about 11% of both total income and total taxes. Those below this group pay less, while those above pay more.

Tax Base and Cyclicality

Estimates from PolicyEngine US (an open-source policy simulation tool) suggest that less than two percent of taxpayers would see tax increases under the Keep Your Pay Act. However, they also estimate a large fiscal cost over a decade (over $5T). This is a far cry from the notion that the proposal could be fully offset, as Booker has stated, by closing tax loopholes and increasing taxes on corporations and the wealthy—for example, by raising the corporate tax rate, tightening rules around executive compensation, and increasing taxes on stock buybacks. Thus, the revenue impact of higher taxes on corporations and high-income households remains an open question and would depend heavily on the specific policy design and behavioral responses.

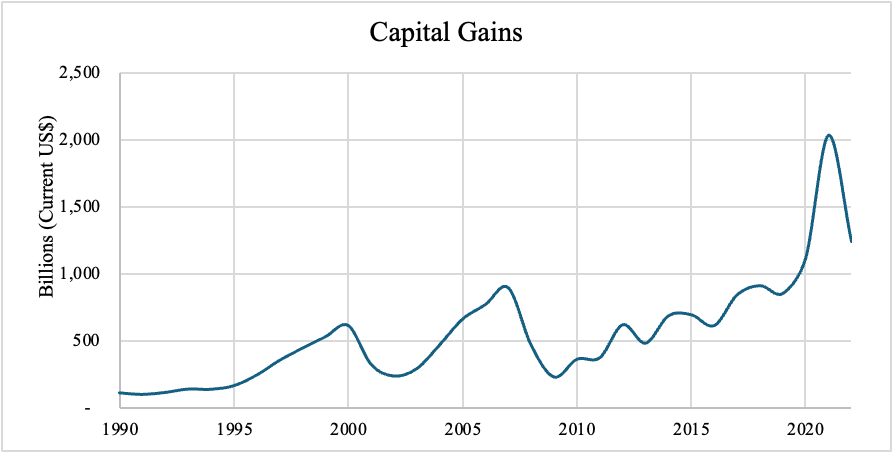

One concern with concentrating the tax base among high earners is revenue cyclicality. During economic expansions, tax revenues rise sharply. During downturns, they can fall just as quickly. High-income taxpayers tend to derive a large share of their income from capital gains, business profits, and performance-based compensation—all of which are sensitive to economic conditions. Capital gains can be broadly thought of as gains or losses from selling stock or similar assets. In contrast, lower earners derive a larger share of their income from salaries and wages. In Figures 1 and 2 below, I plot IRS data from 1990–2022 to show that salaries and wages consistently exceed capital gains and that capital gains are far more volatile. Because these gains are concentrated among higher earners, a tax system that relies more heavily on them may experience sharper revenue swings during economic downturns.

These figures highlight the volatility of a major revenue source that Booker’s policies aim to target. By lowering our reliance on a stable tax base in favor of increasing taxes on the top earners, this policy risks revenue shortfalls during economic downturns.

Figure 1: Capital Gains by Year

Figure 2: Salaries and Wages by Year

Cyclicality creates challenges for policymakers, who must balance the need for stable revenue with the desire to provide stimulus during economic downturns, when tax revenues are often lowest. A narrower tax base may exacerbate this tension. With policymaking, the devil is in the details, but at first blush, this seems the equivalent of leaning back on only two legs of the taxing stool and hoping we don’t fall.

Conclusion

Expanding tax relief for lower-income households is a clear policy choice with well-understood distributional and compliance effects. The more difficult questions lie in public financing and stability: who ultimately bears the cost, and how resilient the resulting tax system is over time.

References:

R. Hess (2026). Why should we care about partnership businesses? https://taxpolicynetwork.org/why-should-we-care-about-partnership-businesses/

R. Lester & T.M. Ahokovi (2026). Why Do We Tax Businesses, and What Types of Taxes are There? https://taxpolicynetwork.org/why-do-we-tax-businesses-and-what-types-of-taxes-are-there/

Tax Foundation. (2024). Summary of the Latest Federal Income Tax Data, 2025 Update. https://taxfoundation.org/data/all/federal/latest-federal-income-tax-data-2025/