Enforcement: The Engine of Tax Compliance

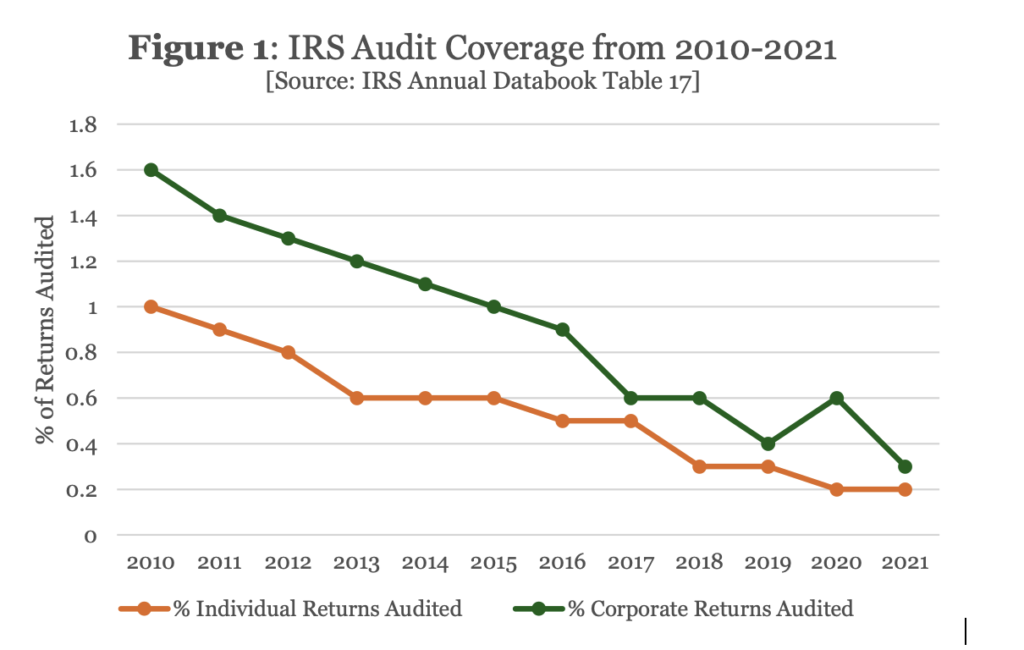

Every spring, Americans are reminded of a central feature of the U.S. tax system: much of it runs on honesty. Individuals and businesses calculate what they owe, file a return, and send a payment, often without ever hearing from the government again. The Internal Revenue Service (IRS) audits only a small share of those returns, and audit rates have fallen substantially over the past several years (see Figure 1). Yet decades of research show that even a limited enforcement presence has an outsized effect on how much tax revenue the government ultimately collects.

The stakes are large and increasingly well documented. The IRS’s most recent estimates indicate that the federal government now loses well over $600 billion each year because taxes that are legally owed are not fully paid. This “tax gap” reflects underreported income, overstated deductions, and taxes that are assessed but never collected. It is not confined to any one group of taxpayers or type of income; it arises wherever reporting is complex, income is hard to observe, or enforcement is limited. A substantial body of research shows that enforcement capacity plays a central role in determining how large this gap becomes.

The most visible role of enforcement is straightforward. When the IRS audits a return, identifies unpaid taxes, and collects them, government revenue increases. Audits routinely uncover underreported income and improper deductions, especially when tax rules are complex or income does not flow through traditional reporting channels. These direct collections are real and measurable, and they often feature prominently in budget debates.

But direct collections tell only part of the story. Across many studies, economists find that enforcement has powerful spillover effects. When taxpayers believe there is a meaningful chance of being audited by the IRS, they tend to report more income and claim fewer questionable deductions, even if they are never audited. These deterrence effects can persist for years, shaping behavior long after an enforcement action occurs. In fact, the evidence suggests that deterrence often generates as much or more revenue than audits alone, making it a critical but less visible component of enforcement’s payoff. When audit rates fall for sustained periods, as they have over much of the past decade (Figure 1), taxpayers perceive a lower risk of detection, which weakens deterrence and reduces voluntary compliance even among those who are never audited.

A simple real-world example helps illustrate why. Imagine a self-employed contractor whose income is not reported by an employer. If audits are common and enforcement is visible, the contractor knows that underreporting carries real risk and reports the business income honestly. Now imagine audits become rare and news stories highlight staffing shortages at the IRS. The risk of detection feels remote. Under those conditions, the contractor may decide to underreport some income, not because they expect to be audited, but because they expect they will not. Multiply that decision across millions of taxpayers, and the revenue consequences can quickly add up.

The level of enforcement also matters. When the IRS has more staff, time, and expertise, it audits more returns and examines them more thoroughly. When enforcement resources are cut, research shows that audit rates fall and inspections become narrower. The resulting revenue losses from fewer and narrower audits can exceed the savings from cutting enforcement budgets, even before accounting for broader deterrence effects.

Importantly, enforcement today is not just about investing in auditors. The IRS has increasingly focused on using technology, artificial intelligence and data analytics to make enforcement more effective and targeted. Improved data matching, analytics, and risk-scoring tools allow the agency to better identify returns with a higher likelihood of noncompliance. Investments in information reporting and automated screening can help direct enforcement resources toward high-risk areas.

The policy implications are clear. The empirical evidence consistently shows thatinvestments in tax enforcement tend to raise more revenue than they cost. Cutting enforcement may reduce government spending in the short run, but it often leads to larger revenue losses that offset or exceed those savings. Once deterrence effects are taken into account, the return on enforcement spending becomes even larger.

The takeaway from decades of research is simple: tax enforcement is not just a bureaucratic expense. It is a revenue-raising investment that encourages compliance. Strong enforcement helps ensure that the taxes Congress has enacted are the taxes that are actually paid. Weak enforcement quietly shrinks the tax base and leaves hundreds of billions of dollars on the table each year.