Corporate Income – only a part of US Business Income

Introduction

In 2019, headlines broke: Despite doubling its profits to $11 billion in the previous year, Amazon had paid zero federal income tax.[1] Public outcry erupted, sparking heated conversations about the equity of tax systems. Then-presidential candidate Joe Biden stated, “No company pulling in billions of dollars of profits should pay a lower tax rate than firefighters and teachers.”

Yet understanding what actually happened in the Amazon case, and whether it represents a “loophole” or the tax system working as designed, requires moving beyond headlines to examine how business income is defined, measured, and taxed. What a company owes depends on a myriad of factors: its legal structures, investment choices, financing methods, assets valuations, just to name a few. Furthermore, the tax code doesn’t just measure these decisions: It actively influences them, creating a feedback loop between tax policy and business behavior. Understanding these nuanced mechanics is therefore essential for evaluating proposed reforms and their likely economic effects. This article aims to provide that foundation.

What is “Business” Income?

In 2022, corporate income taxes accounted for just 8.3% of federal tax revenue.[2] This modest share might suggest that business income plays a minor role in the American tax system. However, this statement would be an oversimplification of the ways in which business income manifests.

The 8.3% figure captures only C-corporations, who pay entity-level tax—a minority of American businesses. Most businesses don’t file as corporations at all. Instead, their income flows directly through to individual tax returns, where it appears and is taxed alongside wages, dividends, and other personal income. This “flow-through” structure means that business income’s role in federal taxation is far larger than corporate tax collections suggest. To understand its true significance, we must first establish what qualifies as “business income” in the US tax system.

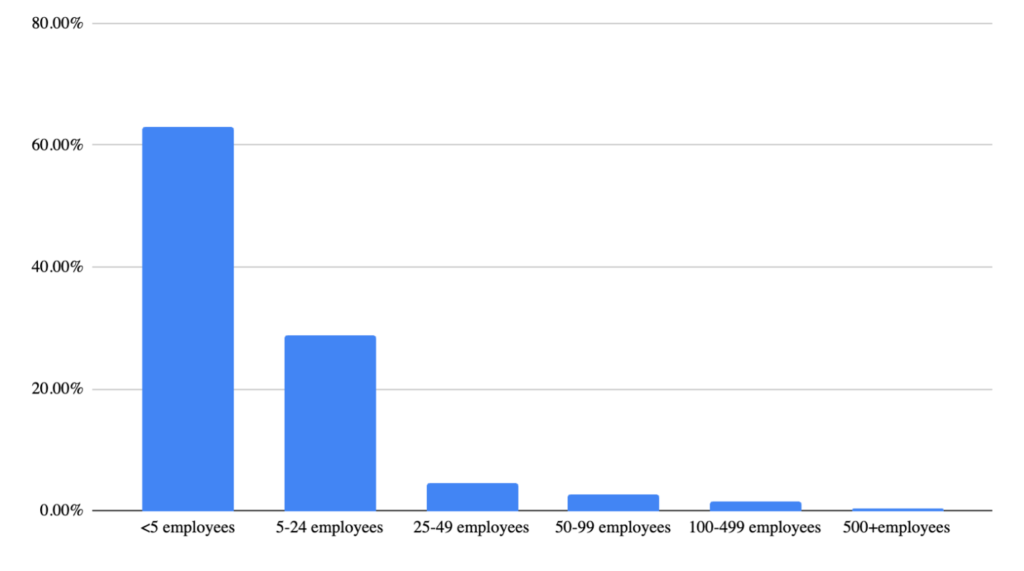

In 2022, approximately 6.4 million business entities operated in the United States, according to the US County Business Patterns and Economic Census. The vast majority of these were small operations: 63% employ fewer than 5 workers. Businesses with greater than 100 employees account for less than 2% of all businesses.

Figure 1: Distribution of Business Establishments by Employment Size (2022)

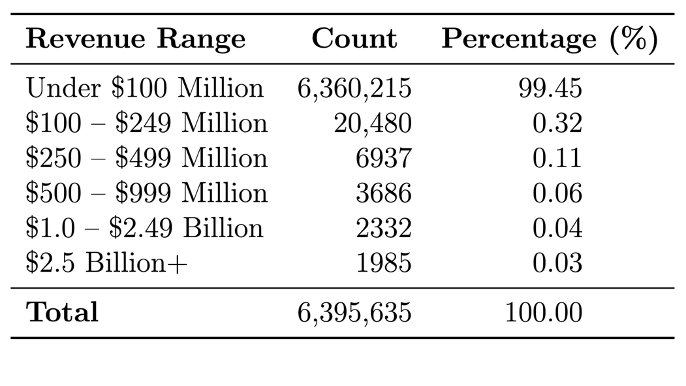

Yet from a tax revenue perspective, these small businesses generate a smaller proportion of revenues. The smallest 99% of firms by receipts collectively represent $12.8 trillion. In contrast, the remaining 1% together account for $38.5 trillion, nearly 75% of all business revenues reported; see Table 1 below.[3]

Table 1: Number of Business Establishments by Revenue Range

This correlation between firm size and entity choice has profound implications because business income does not follow a single tax path in the United States. Rather, it diverges sharply based on legal structure. Some businesses pay entity-level tax on their profits; others pass income directly through to their owners’ individual returns. Understanding this structural divide is essential to assessing business income’s true contribution to federal coffers.

How does business income get taxed?

Business income in the United States is broadly taxed through two different methods, depending on the entity structure. The key difference is whether a firm is a corporate entity “C Corporation” or if it is a flow-through entity (sole proprietorships, partnerships, or S corporations).

Corporate Taxation:

C-corporations (what people colloquially know as “corporations”) face a distinct two-tier tax structure. First, the corporation pays tax on its profits at the entity level (currently a flat 21% federal rate). Then, when after-tax profits are distributed to shareholders as dividends, those distributions are taxed again on shareholder’s individual returns at qualified dividend rate (0%, 15%, or 20% depending on level of taxable income). This “double taxation” can result in a combined effective tax burden upwards of 40% for certain shareholders.[4]

Flow Through Taxation:

Flow-through entities are business structures that do not pay taxes at the entity level. Instead, all income passes directly (i.e. “flows through”) to the tax returns of its owners, shareholders or investors, where it is taxed only once at the owner’s level.

Sole proprietorships are the simplest flow-through; a sole proprietor reports all business income on his/her personal income tax return. The income is subject to both ordinary federal income tax (up to 37%) and a self-employment tax (~15.3%), which covers both social security and medicare obligations.

Partnerships operate similarly but instead may involve multiple owners. The partnership itself files an informational return (Form 1065) but pays no tax. Each partner receives a Schedule K-1 showing the proportionate share of partnership income, deductions, and credits, which is the reported on each partner’s own return. Partners can be individuals and corporations. Partners can also be other flow-through entities, which means that partnership income can flow through many layers.

Like partnerships, S-corporations file information returns and issue K-1s to shareholders. However, S corporation status is only available to businesses meeting strict eligibility requirements: they can only have a single class of stock, they must have 100 or fewer shareholders, and the shareholders are limited to U.S. citizens, residents, and certain trusts. Despite these restrictions, S corporations represented approximately 55% of all corporations in 2022, making them one of America’s most popular business structures.

Composition of Businesses in the US

Thus, when we talk about “business income” in the US, namely that corporations seem to contribute a relatively small portion of that income, it is important to remember that business income gets earned in other forms and types of entities. Business income is not only corporate income – it also includes income earned in sole proprietorships, partnerships, and S corporations.

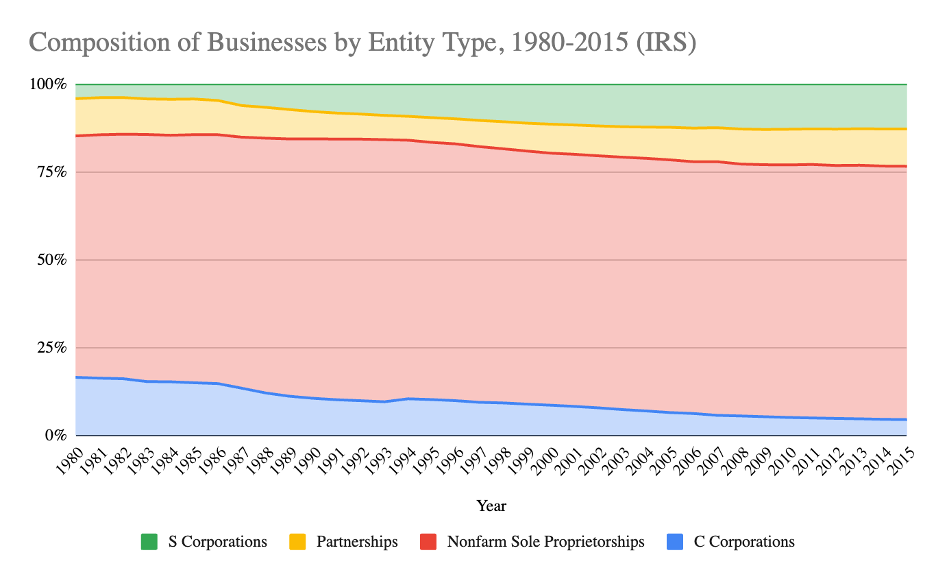

This distinction is important because the number of corporate entities has been declining over time. The figure below plots the number of entities by each type, dating back to 1980. As individual tax rates have declined (thus making flow-through entities relatively more attractive), the number of flow-through entities has increased.

Figure 2: Composition of business establishments by entity type, 1980-2015. In 2015, C corporations comprised of around 4.6% of all business establishments. S corporations, ~12.8%; Partnerships, ~10.6%; Nonfarm sole proprietorships, ~71.9%.

Understanding this key fact is important because individual tax rate changes also impact flow-through businesses. And “business income” affects many more taxpayers than those we typically talk about as corporations.

[1] https://itep.org/huffington-post-amazon-has-doubled-profit-to-11-billion-but-will-pay-0-in-taxes-in-2019-report/

[2] https://taxfoundation.org/data/all/federal/us-tax-revenue-by-tax-type/

[3] 2022 SUSB Annual Data Tables, “The Number of Firms and Establishments, Employment, Annual Payroll, and Receipts by Industry and Enterprise Receipts Size: 2022”: https://www.census.gov/data/tables/2022/econ/susb/2022-susb-annual.html

[4] https://taxpolicycenter.org/briefing-book/corporate-income-double-taxed