A Year After Liberation Day What are Corporate Filings Revealing About the Tariff Era?

On April 2, 2025, “Liberation Day,” the Trump administration announced sweeping reciprocal tariffs that redrew the map of U.S. trade policy overnight. One year later, the landscape looks nothing like what was announced that day. During the last year, various countries have agreed to new trade deals with the Trump administration, while, at a firm level, tariff policy has at times been implemented on a case-by-case basis, for example, the notable exemption for Apple iPhones, and the additional duties levied on certain computing chips. Further, the Supreme Court struck down the IEEPA-based tariffs on February 20, 2026, leading to a “replacement” 10% global tariff that was issued by executive order the same week. Meanwhile, section 301 tariffs and section 232 levies on steel and aluminum remain in place, some of which turn 8 years old this summer.

Through all of it, American corporations have been communicating tariff risks and/ or impacts through annual filings. I conducted an analysis of the 80 annual 10-K reports filed by S&P 100 companies between January 1 and April 29, 2026 to see what firms are saying a year after “Liberation Day”.

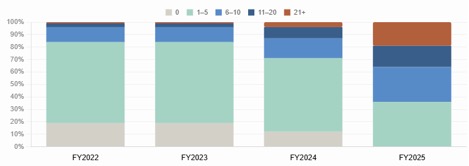

The word “tariff” appears in every single filing

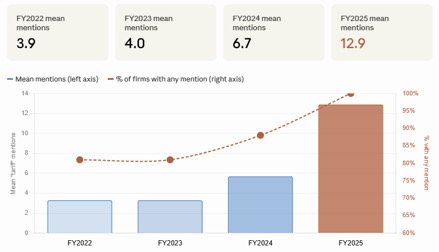

All 80 filings mention tariffs at least once. More telling though, is what happened to the intensity of disclosure over the last four years. The figures below track the same firms from FY2022 through FY2025.

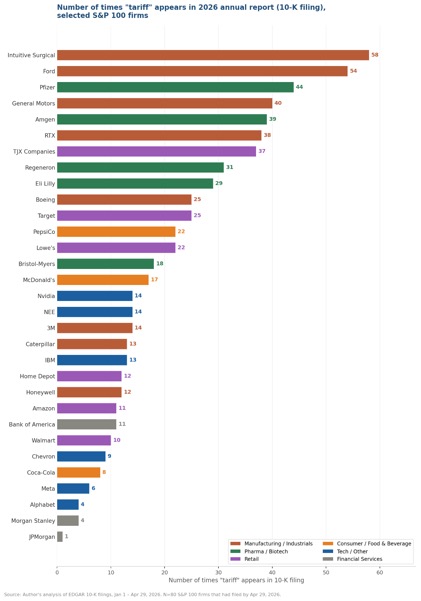

Three years ago, the median (average) S&P 100 company mentioned tariffs twice (four times) in its annual report. Today, the median (average) is eight (thirteen) times, with firms like Ford (54 mentions) and General Motors (40 mentions) discussing tariff exposure repeatedly throughout their filings, directly addressing the “disruptive” nature of tariffs on their operations and quantifying their costs.

What types of companies are impacted?

The variation across companies reveals something about who is absorbing the tariff burden. General Motors quantifies a $3.1 billion EBIT impact in 2025 and projects $3 to $4 billion for 2026. Ford estimates a $2 billion EBIT impact in 2025 after offsets. Other firms such as Intuitive Surgical (producer of da Vinci surgical robots) focus more heavily on uncertainty and risk around the current tariff environment, they do however attribute their decreasing year-over-year profit margin partially to new tariffs. The pharmaceutical companies tell a different story; Bristol-Myers Squibb, Eli Lilly, Pfizer, and Regeneron all rank among the highest-mention firms, but their disclosures share a common thread: exemptions on pharmaceuticals, and the uncertainty around those exemptions.

At the opposite extreme sit the financial and software companies. JPMorgan mentions tariffs exactly once. Goldman Sachs, Morgan Stanley, and Citigroup are similarly terse. Since banks generally are not significant importers, tariffs matter primarily if they affect the credit quality of borrowers, the economy as a whole, or the volatility of financial markets; and, interestingly, banks seem to be limited their discussion of these types of risks. The gap between JPMorgan’s single mention and GM’s forty is a reminder that tariff incidence is highly uneven, with heavy impact on manufacturing, retail, and technology hardware, and minimal impact on financial services and software.

The refund question

The Supreme Court’s February 20, 2026 ruling in Learning Resources, Inc. v. Trump struck down all IEEPA-based tariffs as exceeding the president’s statutory authority. This introduced a new element to an already complex tariff environment: the potential for mass tariff refunds. U.S. Customs and Border Protection (CBP) estimates that approximately 330,000 importers paid around $166 billion in IEEPA duties.

This ruling clearly entitles numerous major corporations to sizable refunds. For example, in their most recent 10-Q filing, Ford disclosed that they anticipate a $1.3 billion refund related to the IEEPA ruling. However, this also adds a level of complexity for firms in trying to navigate the current political climate. Several firms, most notably Apple and Amazon, have reportedly not yet sought tariff reimbursements. While to date these firms have not discussed this decision, President Trump said during an interview on CNBC’s “squawk box” he would “remember” companies that do not seek refunds, implying this might be an attempt by corporations to curry favor with the executive branch.

Firms seeking refunds face a further complication: class action lawsuits from consumers who paid higher prices during the tariff period and now want their share of any government refund. One firm notably dealing with this type of issue is Fedex. In their most recent 10-Q filing they discuss the Supreme Court ruling and disclose that they have filed a lawsuit against CBP to recover IEEPA tariffs. However, in the same note, they acknowledge that “five class action lawsuits seeking refunds of IEEPA tariffs from FedEx were filed in U.S. district courts in South Carolina, Florida, New York, Tennessee, and Delaware.”

In short, while Learning Resources, Inc. v. Trump seems to have mandated government refunds associated with unlawful tariffs, in most cases it remains uncertain when refunds will be received, who will file for refunds, and if some refund money will end up being paid back to customers.

Conclusion

The picture that emerges from the current disclosure environment is one of gradual adaptation. Companies are not treating tariffs as a crisis to be managed but as a recurring cost to be disclosed, quantified, and planned around. Firm financial filings do make it clear that, even a year after “liberation day,” uncertainty around tariffs is still significant, especially for heavily impacted industries. Refund litigation is ongoing, the replacement 10% tariff faces its own legal challenges, and trade policy more broadly remains subject to executive action and political whims.