Is Cryptocurrency Cake?

Cryptocurrency has promised financial innovation in the form of a decentralized payment network. However, that innovation has created regulatory challenges and debates. This note focuses on one long-running debate, the taxation of staking rewards. In Jarret v. United States., the plaintiff argued that the cryptocurrency received from staking was “like a baker who bakes a cake” and should not be taxed until the cryptocurrency is sold. The opposing view, taken by the Internal Revenue Service, is that staking rewards are income when received.[1] Rather than focus on the legal debates around current law,[2][3] I examine the question through general tax policy goals to argue that staking block rewards should be income when received. I find that although there are tax policy goals that may support very limited deferrals, the analogy is weak when applied to cryptocurrency and may create opportunities to structure blockchain protocols for tax avoidance.

Background

To understand the blockchain, it is useful to think of it is as a “distributed ledger.” There exists, floating in the ether of the internet, a list of transactions, the ledger, and everyone has access to it all at once. But, for this system to work, some people must be authorized to record transactions, and compensated for doing so. It is like paying an accountant to keep the blockchain’s books. Proof-of-stake blockchains use staking to determine which users (called validators) are allowed to record transactions to the blockchain. Blockchains use a carrot and stick approach to incentives. There are generally use two methods to reward validators. The first is block rewards. The validator who writes the block to the blockchain is rewarded with a fixed amount of cryptocurrency as a block reward. This cryptocurrency is newly created and increases the total supply of cryptocurrency in circulation. The second method is transaction fees. In order to engage in a transaction on the blockchain, a user may pay a fee. The fee is then paid to the validator who processes the transaction. On the other side validators also bear some economic cost as staked cryptocurrency can be subject to loss in a process known as slashing.

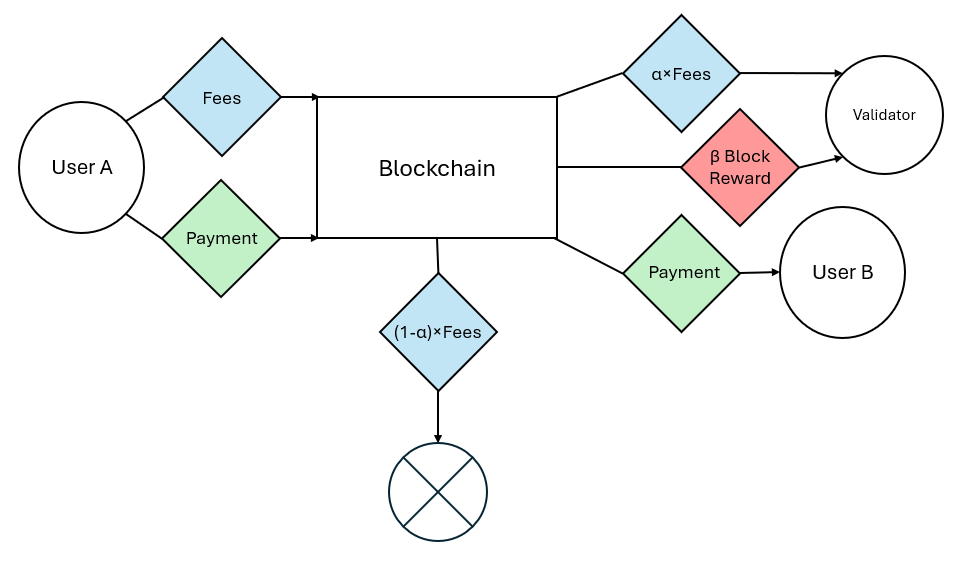

In Fig. 1, I present a simplified cryptocurrency staking example where there are two blockchain users and one validator. The example has three parts. First, represented in green, User A sends a payment to User B. Second, represented in blue, User A pays a transaction fee. Those fees are split into two parts. A percent (α) of the fees are paid directly to the validator and the remaining fees (1 – α) are “burned” or destroyed.[4] Third, represented in red, the blockchain protocol creates an amount of new cryptocurrency (β) which is also given to the validator as a block reward.

Figure 1.

A basic principle in taxation and accounting is that the treatment of any transaction should reflect its underlying economics. From an accounting standpoint, income is recorded when earned and expenses are recorded when incurred, with a focus on matching corresponding income to the expenses which generated the income. Deviations from these principles in taxation occur frequently due to a variety of factors, generally for a practical, policy, or political reason. In the next sections, I outline two related arguments in support of deferring the taxation of staking rewards.

Cryptocurrency as a self-created asset

One of the most common arguments against the immediate taxation of staking rewards is that block rewards are self-created assets. Often used analogies include farmers who grow crops but do not recognize income when crops are harvested,[5] or bakers who doesn’t recognize income when the cake comes out of the oven.[6] In Tootal Brahurst Lee Co. v. Commissioner 30 F .2d 239, 240-41 (2d Cir. 1929), the court noted that this deferral of income is necessary as there may be many intervening events, and without an external party, there is no way of determining what the actual income amount is until a sale. The court stated the value of a product “is dependent upon the rule of supply and demand, deterioration or destruction of the product, and although the product may be worth more as a manufactured article than as the raw material, there is no way of determining the profit until a sale is realized and the price becomes known.” These uncertainties support taxing the income come only when the farmer sells her crops, or the baker sells his cake.

The court’s reasoning in Tootal generally follows sound tax principles and serves the public interest. There are many cases where taxation is delayed due inability to calculate income or because the taxpayer may not have the immediate liquidity to pay the tax. However, it is worth considering how the factors in Tootal may apply to cryptocurrency. First, cryptocurrency is intrinsically a digital good. It is not physical property. It cannot rot, spoil, or deteriorate.[7] In the case of cryptocurrency, the argument for deferral is strongest for delaying recognition of income until the block rewards can be withdrawn and is no longer subject to the risk of forfeiture through slashing.[8] This would also mimic the taxation of items such as restricted stock compensation, which is generally not taxed until the stock is transferable or no longer subject to substantial risk of forfeiture unless a taxpayer elects otherwise.[9]

The court also cites the rule of supply and demand and the determination of profit as facts supporting deferral of income. This argument again makes sense in the case of physical goods, which can have significant time and uncertainty between value creation and eventual sale, and whose prices may not be readily knowable. One of the defining features of cryptocurrency is the ability to trade at any time near instantaneously. Most major cryptocurrencies are openly traded on several major markets, with billions of dollars of daily volume and significant market depth.[10] Taxpayers who have control of cryptocurrency can accurately determine its price at any time and, importantly, are able to sell it at the market price.[11] To the extent a cryptocurrency has price risk related to cryptocurrency holdings, it comes from the taxpayer’s choice to hold the cryptocurrency, not due to inherent limitations beyond the control of the taxpayer.

There are reasons that may favor a very limited deferral of the recognition of income until the taxpayer has control over the assets. As mentioned earlier, there are many situations where tax policy dictates deferral of income because the taxpayer may not have the requisite cash to pay the tax owed on a transaction. To the extent that validators are required to hold block rewards, or the block reward is at risk of loss due to slashing, there is a compelling reason to defer taxation. Just like in Tootal, there would be risk of intervening events (slashing) and a risk of loss. For most blockchains, this would only result in a very limited deferral, and current rules under Revenue Ruling 2024-14 already require that the taxpayer have “dominion and control” of the cryptocurrency before taxation. On net, requiring the recognition of income after the short period when a taxpayer does not have control of the block rewards would not place a significant burden on taxpayers.

Who pays block rewards

The valuation argument is also often framed from a legal perspective as a requirement that there must be a counterparty in order to have income. From a tax policy perspective, this has historically made sense. Wealth acquired without a direct counterparty would typically only include things such as natural resources or items produced by a taxpayer’s own labor. Once again, these items would be hard to value with a significant amount of uncertainty in the eventual valuation. When applied to cryptocurrency however, the view that there is no counterparty takes a very narrow view of blockchains.

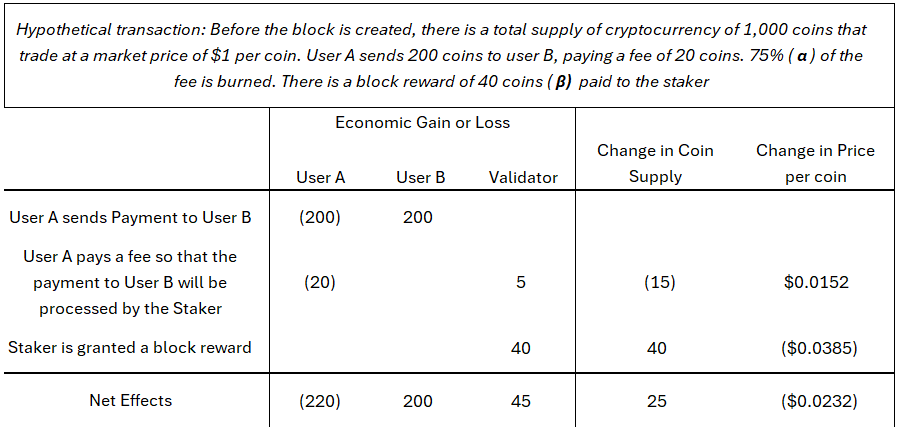

Table 1.

We can examine the economic effects on all parties using a simplified example. Table 1 details the direct and indirect economic effects of each part of a hypothetical transaction based on Fig. 1. When User A pays a fee for the transaction to be processed, User A has an economic loss of 20 coins. The fee is then split into two parts. One part of the fee is paid to the validator (5 coins). As noted above it is generally agreed that fees are income to the validator. The other portion of the fee is permanently removed from the supply of the cryptocurrency through the process of burning (15 coins). This has an indirect effect on all holders of the cryptocurrency, as it raises the value of the remaining cryptocurrency by $0.015 per coin.[12] Lastly, the blockchain creates new cryptocurrency (β) as a block reward and gives it to the validator (40 coins). In an efficient market, there is a deflationary effect from the burning of the transaction fees, but that is offset by the inflationary effect of the block rewards. In the case of the example, the net effect is inflationary and the price of the coin decreases by $0.023. If there is a net issuance of coins, there is a transfer of value from cryptocurrency holders to validators. If there is a net destruction of coins, then there is a transfer of value from the user paying the fees to cryptocurrency holders.[13]

Although there is no direct counterparty, blockchain protocols are public. Holders of a particular cryptocurrency have actively chosen to pay for payment processing through dilution.[14] Unlike a natural resource, the value which accrues to the validator as a block reward comes from other cryptocurrency holders. It is also clear that participants in blockchains chose the structure of the blockchain. Blockchain protocols are actively managed and updated through governance protocols. For example, participants on both the Bitcoin and Ethereum networks can coordinate and implement changes through Improvement Protocols.[15][16] Major changes have been made to the Ethereum blockchain, such as moving from Proof-of-Work to Proof-of-Stake. It is unclear why tax policy should favor a blockchain which chooses to pay for transaction processing through dilution of current owners compared to one which requires users sending transactions to pay for processing directly.

Potential taxpayer incentives with deferral

More generally, treating block rewards differently from fees violates the general tax policy goal of treating similar transactions similarly. Imagine two scenarios. In scenario A, the blockchain developer sets a fixed fee per block of 50 coins and pays 100% of the fee to the validators. In scenario B, the blockchain developer sets the same fixed fee of 50 coins, but codes the blockchain to burn 50 coins for each block and create 50 new coins as block rewards given to validators. In this stylized example, there is no clear economic difference between scenario A and B, yet under deferral for block rewards, Scenario A would generate $50 of immediate income while Scenario B would generate $0 of immediate income. Lawmakers should seek to tax two economically identical economic transactions the same. In an extreme case, a blockchain could be designed to create tax deductions via fees paid while deferring the recognition of any income from block rewards.

There is also another issue with deferral, the matching of expenses to revenues. Deferring only the income from block rewards creates a mismatch between the income recognized and the expenses related to that income. This is particularly true for cryptocurrency mining, which has greater upfront costs, but also applies to staking. Both staking and mining likely are activities engaged in for the pursuit of profit and may qualify as business activities with deductible expenses. If income from block rewards can be deferred until the sale of those rewards, it could allow taxpayers to recognize losses related to ongoing expenses while deferring income indefinitely. If lawmakers want to allow the deferral of income, they should also explicitly mandate capitalization and deferral of any expenses related to the deferred income.

Conclusion

The argument that cryptocurrency staking is like baking a cake, and therefore should not be taxed until the cryptocurrency is sold, is not persuasive when thinking about optimal tax policy. Cryptocurrency is not like physical property that is hard to value. Most cryptocurrency is easy to value, with market prices available 24/7. Cryptocurrency does not carry significant risk of loss or deterioration, unlike physical property. A key feature of cryptocurrency is its decentralized electronic ledger, which makes it extremely resilient to a variety of risks. Finally, treating block rewards differently than transaction fees would create the opportunity for blockchain participants and developers to adjust blockchain protocols to maximize tax savings without changing the economic substance of the transactions. Without a strong policy reason to incentivize validators to hold block rewards, policy makers should default to treating block rewards equally with other similar transactions and have them taxable once the rewards are fully under the control of validators.

[1] Revenue Ruling 2023-14, taxation occurs when the taxpayer has an “accession to wealth” and “gains dominion and control” of the cryptocurrency.

[2] See Marian, O. (2022). Law, Policy, and the Taxation of Block Rewards. Tax Notes. https://www.taxnotes.com/featured-analysis/law-policy-and-taxation-block-rewards/2022/06/03/7dhq5. Accessed March 20, 2026.

[3] See Schwartz, J. (2026). U.S. Federal Income Taxation of Staking Rewards. https://static.cahill.com/docs/Staking%20Tax%20Memo.pdf. Accessed March 20, 2026.

[4] For example, since August 2021, the Ethereum network permanently removes a portion of fees paid from the total supply of ETH (“burns”). This change was made under Ethereum Improvement Proposal (EIP-1559). (https://eips.ethereum.org/EIPS/eip-1559)

[5] For example, Making America the Crypto Capital of the World: Ensuring Digital Asset Policy Built for the 21st Century, 119th Cong. (2025) (testimony of Jason Somensatto) and Examining the Taxation of Digital Assets, 117th Cong. (2021) (testimony of Peter Van Valkenburgh).

[6] For example, Complaint, Jarrett, No. 3:21-cv-00419 (M.D. Tenn. May 26, 2021)

[7] A taxpayer could lose their cryptocurrency if they forget or lose access to their private key, which serves as a digital proof of ownership for cryptocurrency.

[8] Under Revenue Ruling 2023-14 taxpayers are currently only taxed once they have “dominion and control”, which is typically interpreted as the time when a taxpayer can withdraw and sell their cryptocurrency.

[9] 26 USC § 83(a)

[10] Coinmarketcap.com reports 24-hour bitcoin volume of $39 billion and 24-hour Ethereum volume of $18 billion. In total, 8 of the top 10 cryptocurrencies by market cap had over $1 billion in 24-hour volume. Accessed March 24, 2026.

[11] Although the most commonly used and held cryptocurrencies are large and liquid, there may be tax policy reasons to treat illiquid cryptocurrencies which are hard to value in a different manner.

[12] I assume that there is some intrinsic value to the blockchain itself that is unrelated to individual coins. For example, there may be value in a blockchain if remittances through cryptocurrency are cheaper than non-cryptocurrency alternatives. For example, Bitso, a Mexican cryptocurrency exchange, reports processing over $3 billion in remittances in 2022. Transaction costs for these remittances can be just 1 percent compared to up to 10% with competitors like Western Union or MoneyGram.

Schwartz, L. (2023). How crypto can reshape the $130 billion remittance market in Latin America. Fortune. https://fortune.com/crypto/2023/05/03/how-crypto-can-reshape-the-130-billion-remittance-market-in-latin-america/. Accessed 3 May 2023.

[13] To the extent that inflationary or deflationary pressure changes the valuation of block rewards, the change should occur at approximately the same time as the transaction and be incorporated into the price of the cryptocurrency. Since block generation happens continuously, expectations of inflation or deflation are likely already built into most cryptocurrency prices.

[14] For example, Bitcoin’s cap of 21 million coins has long been seen as a reason for price appreciation. Prior academic work has also found negative relations between supply of cryptocurrency and prices (see Peng, S., Prentice, C., Shams, S., & Sarker, T. (2024). A systematic literature review on the determinants of cryptocurrency pricing. China Accounting and Finance Review, 26(1), 1-30.)

[15] For a more detailed history of Bitcoin changes,, see: https://www.blog.bitfinity.network/bitcoin-fork-history-the-evolution-of-protocol-changes/

[16] See: https://eips.ethereum.org/EIPS/eip-1