When Wealth Taxes Rely on Financial Accounting Numbers

When people think about billionaire wealth, they picture mansions, yachts, and private jets. But those assets make up only a tiny fraction of billionaire wealth. According to Altrata’s Billionaire Census, about 66% of billionaire wealth is tied up in business equity, while only about 3% is in real estate and luxury assets. And nearly half of that business equity is in private companies, not publicly traded firms.[1]

Public companies have easily observable prices. Private companies do not and must instead be valued using estimates. Wealth taxes therefore run into a basic problem: much of the wealth they aim to tax does not have a price. It has an estimate.

Estimating the Value of Private Companies

This problem may sound academic, but it becomes very real when governments try to tax the value of private companies. California’s proposed billionaire tax, for example, estimates private company values using a formula based on financial accounting numbers.

California Taxable Value = Book Value + 7.5 × Average Earnings

This approach is not entirely unusual. Switzerland, for example, estimates private company value as a weighted average of book value and capitalized earnings:

Swiss Taxable Value = (2 × Earnings Value + Book Value) / 3

In the Swiss system, Earnings Value is earnings divided by a government-set capitalization rate, currently about 10 percent. California’s formula looks different, but the idea is similar. Both methods rely on the same underlying accounting numbers, book value and earnings, to estimate firm value.

As an accounting professor, I am always encouraged when financial accounting takes center stage in public policy debates. But this proposal should come with an accountant’s warning: accounting numbers were not designed to measure firm value.

1. The Financial Information Problem

Wealth tax proposals in the US are often discussed using European examples, but European private companies operate in a very different reporting environment. In much of Europe, private companies are required to prepare and publicly file financial statements each year. Many are also required to have those statements audited. The information needed to value private businesses therefore already exists and is often independently verified.[2]

The United States has a very different system. Private companies are not required to publicly disclose financial statements, and many do not prepare financial statements using generally accepted accounting principles (GAAP).[3] Furthermore, IRS data indicate that fewer than 40 percent of private companies with at least $10 million in assets receive an audit.[4] Audited GAAP financial statements are the exception rather than the rule, even among fairly large firms.

In Europe, the valuation problem is how to use accounting data. In the United States, the problem begins earlier: whether the data exist and whether they can be trusted.

2. The Book Value Problem

A firm’s book value reflects its assets minus liabilities. But book value was never meant to measure what a business is actually worth, and the two numbers often differ substantially for several reasons.

First, book value excludes many assets that drive value in modern businesses, including data, brands, customer relationships, and patents. Because accounting rules generally require internally created intangible assets to be immediately expensed, they never appear as an asset on the balance sheet.[5] As a result, much of modern firms’ value would not be taxed under a book-value system.

Second, accounting is generally conservative in practice, meaning losses are recognized more quickly than gains and asset values are written down more readily than written up.[6] This conservatism will compound the understatement of wealth under a book-value tax system.

Third, economic value depends on expected future cash flows of the business. Book value, however, depends partly on how the business is financed. Two companies with identical operations and economic value can report very different book values simply because they use different financing. Change the financing and the tax bill will change even if the business does not.

In short, book value reflects accounting rules, accounting conventions, and financing choices as much as it reflects economic performance. If the goal is to tax accounting outcomes, a book-value tax makes sense. If the goal is to tax economic wealth, it does not.

3. The Earnings Problem

These wealth tax formulas also rely on earnings. But earnings have their own limitations.

Companies that invest heavily in future growth often report negative earnings because accounting rules require many investments, such as research and development and marketing, to be expensed immediately. This is why the majority of companies going public report losses even though investors value them at billions of dollars. Earnings-based formulas would therefore undervalue many high-growth firms, including many of the California-based firms owned by billionaires that the proposed wealth tax is designed to target.

Another issue arises when these formulas convert earnings into values using a fixed earnings multiple. Price-earnings ratios range from less than 10 in some industries to over 100 in others. Applying the same multiple across all firms assumes the relationship between earnings and value is the same across industries, which it clearly is not. The result is that firms with similar economic value will face different taxes simply because they operate in different industries, violating horizontal equity.

Do These Formulas Approximate Market Value?

These issues raise an obvious question: how well do these formulas actually approximate market value? For private firms in the US, there is ultimately no way to know because reliable accounting data and market prices are not observable.

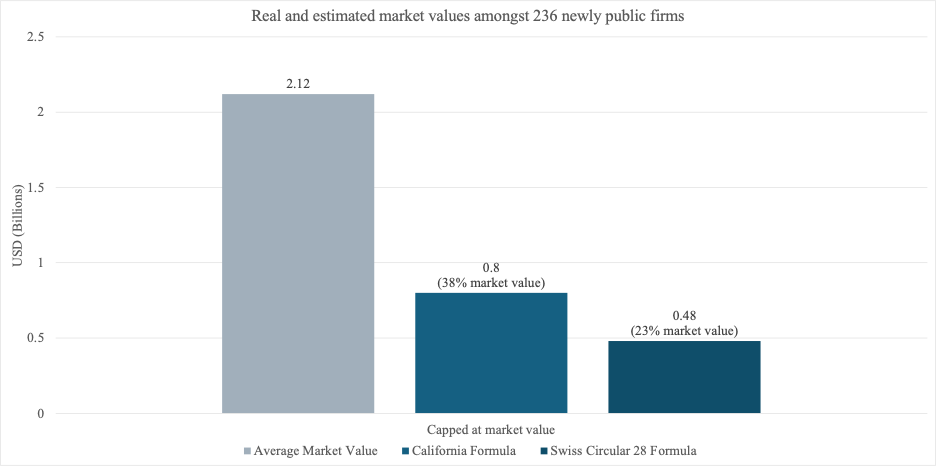

The closest observable test comes from newly public firms, where both accounting numbers and market values are available and firms were recently private. Using the CRSP/Compustat merged database, I identify U.S. firms that went public in 2024 and 2025 with available book value and earnings data. I then apply both the California and Swiss valuation formulas and compare those estimates to market values at the end of the firms’ first fiscal year after going public. Because the California proposal allows taxpayers to submit an appraisal if the formula substantially overstates value, the formula effectively acts as a ceiling for taxable value. To reflect this, I cap formula-based values at 100 percent of market value.

The sample includes 236 firms with an average market value of approximately $2.12 billion at year-end. The California formula produces an average value of approximately $0.80 billion and the Swiss formula about $0.48 billion. On average, the formulas thus produce values equal to roughly 38 percent and 23 percent of market value, respectively.

Public market valuations are typically higher than private market valuations, so the Federal Reserve applies about a 25 percent discount when estimating private business values from public multiples.[7] However, even after accounting for this discount, the differences observed here are far larger than illiquidity alone would explain. This gap does not bode well for how much revenue this type of tax would actually raise.

The Fundamental Private Company Valuation Problem

The California proposal allows both taxpayers and the tax board to submit certified appraisals if they suspect the accounting-based formulas misstate value. But appraisals are expensive, time-consuming, administratively difficult, and subjective, which is why the accounting-based formulas were likely chosen as the default method in the first place.

Concerns about the cost and subjectivity of appraisals are often dismissed by proponents, who argue that private businesses of billionaires have many investors and therefore a record of transactions that make valuation simple. But private market transactions do not produce a single company value. Each financing round involves different securities with varying rights and protections, so the latest round price applies only to that specific security, not to earlier investors who hold different shares. Research shows that using later round share prices to value earlier shares can overstate values by more than 50 percent.[8] Taxpayers would surely challenge these inaccurate valuations, turning what is presented as a simple system into an administratively burdensome one reliant on subjective appraisals and lengthy appeals.

All of these challenges stem from a simple fact: private businesses do not have observable prices. Thus, much of the wealth these taxes aim to tax must be estimated. Estimates are not prices, and formulas based on financial accounting information cannot change that.

My point in writing this is not to argue for or against taxing billionaire wealth, but to offer an accountant’s warning: measuring wealth without market prices is far more difficult than wealth tax proposals often assume.

References

[1] Altrata. (2025). Billionaire Census 2024. Altrata.

[2] Beuselinck, C., Elfers, F., Gassen, J., & Pierk, J. (2023). Private firm accounting: the European reporting environment, data and research perspectives. Accounting and Business Research, 53(1), 38-82.

[3] Call, A., Hendricks, B, Labro, E., & Sutherland, A. (2026), MIT Survey of Private Firm CFOs: Results Summary. https://ssrn.com/abstract=5291766

[4] Lisowsky, P., & Minnis, M. (2020). The silent majority: Private US firms and financial reporting choices. Journal of Accounting Research, 58(3), 547-588.

[5] Lev, B. (2018). The deteriorating usefulness of financial report information and how to reverse it. Accounting and Business Research, 48(5), 465-493.

[6] Watts, R. L. (2003). Conservatism in accounting part I: Explanations and implications. Accounting Horizons, 17(3), 207-221.

[7] Campbell, R. C., & Robbins, J. A. (2025). The value of private business in the United States. Journal of Public Economics, 249, 105466.

[8] Gornall, W., & Strebulaev, I. A. (2020). Squaring venture capital valuations with reality. Journal of Financial Economics, 135(1), 120-143.